Roth IRA vs Traditional IRA: Which One Wins in 2026?

Every year, millions of Americans open an IRA without knowing whether they chose the right type. The difference between choosing correctly and choosing incorrectly can be worth $50,000 to $150,000 over a 20-year retirement. And the right answer is different for almost every person.

The Roth vs. traditional IRA debate is one of the most argued topics in personal finance — and one of the most oversimplified. You’ve probably seen some version of “Roth always wins” or “take the deduction now.” Both camps have loud voices. Both miss something important.

This is not a debate with a single winner. It is a decision framework — one that produces different correct answers for different people depending on five specific dimensions: tax treatment, income limits, withdrawal rules, required minimum distributions (RMDs), and estate planning. By the end of this guide, you’ll know exactly which account wins for your specific situation, and you’ll have the tools to make the most of whichever path you choose.

If you’re just building your foundation, it helps to start by understanding the key retirement planning terms you’ll encounter throughout this decision — terms like MAGI, RMD, IRMAA, and the pro-rata rule will come up often here.

Let’s start with the foundational difference — because everything else flows from one core distinction between these two accounts.

The One Core Difference That Drives Everything

Before any comparison can be meaningful, you need to understand the tax treatment distinction with complete clarity. This is the bedrock of every analysis that follows.

The traditional IRA — pay taxes later.

Contributions may be tax-deductible in the year you make them, reducing your taxable income today. The money grows tax-deferred — no tax on dividends, interest, or capital gains while it sits inside the account. But every dollar you withdraw in retirement is taxed as ordinary income — both principal and growth. You’re essentially making a deal with the government: “I’ll pay taxes later, in retirement.”

The Roth IRA — pay taxes now.

Contributions are made with after-tax dollars — no deduction today. The money grows completely tax-free. Qualified withdrawals in retirement are completely tax-free — every dollar of principal and all growth, forever. You’re making the opposite deal: “I’ll pay taxes now and never again.”

The central question: pay taxes now or later?

- If your tax rate is higher now than it will be in retirement → traditional IRA wins

- If your tax rate is lower now than it will be in retirement → Roth IRA wins

- If your tax rate is the same now and in retirement → mathematically identical (assuming equal contribution amounts)

Here’s how that plays out in practice:

Suppose Michael contributes $7,000 to a traditional IRA at a 25% tax rate, and his twin brother David contributes $7,000 to a Roth IRA. David actually contributes $5,250 of after-tax money (75% of $7,000) and pays $1,750 in tax now. Both earn 7% annual returns for 20 years. Michael’s $7,000 grows to $27,137 — then he pays 25% tax on withdrawal = $20,353 net. David’s $7,000 grows to $27,137 — all tax-free. Their net outcomes are identical because the tax rates were equal. The Roth wins when tax rates rise; the traditional wins when tax rates fall.

Why doesn’t this equivalence hold in practice? Tax rates change — Congress has modified tax brackets multiple times in the past 30 years. People’s income changes dramatically across a career and into retirement. And the Roth IRA has structural advantages beyond pure tax math — no RMDs, flexible withdrawal rules, and estate planning benefits — that often tip the practical balance in real life.

Pro Tip: The cleanest way to evaluate Roth vs. traditional for your situation: compare your current marginal tax bracket to your projected retirement bracket. If retirement rates will be lower → lean traditional. If they’ll be higher or equal → lean Roth. If you genuinely cannot predict → split the difference and contribute to both.

The Five Decision Dimensions — How Each Account Really Performs

Rather than a dry feature-by-feature comparison, here’s what each dimension actually means for a real person making real retirement decisions.

Dimension 1 — Tax Treatment: Current vs. Future

Traditional IRA — the immediate benefit: At the 22% federal bracket, a $7,000 traditional IRA contribution saves $1,540 in federal income tax this year. At 24%, it saves $1,680. The saving is immediate, tangible, and certain — you see it in your tax refund or reduced payment this April.

Roth IRA — the long-game benefit: No deduction today. But qualified withdrawals in retirement (account open for at least 5 years AND age 59½+) are completely tax-free — including every dollar of compounding growth. The longer the money stays invested, the more powerful that tax-free treatment becomes. $100,000 of investment growth in a Roth costs you nothing when you withdraw it. In a traditional IRA, that same $100,000 of growth triggers ordinary income tax at whatever rate applies in retirement.

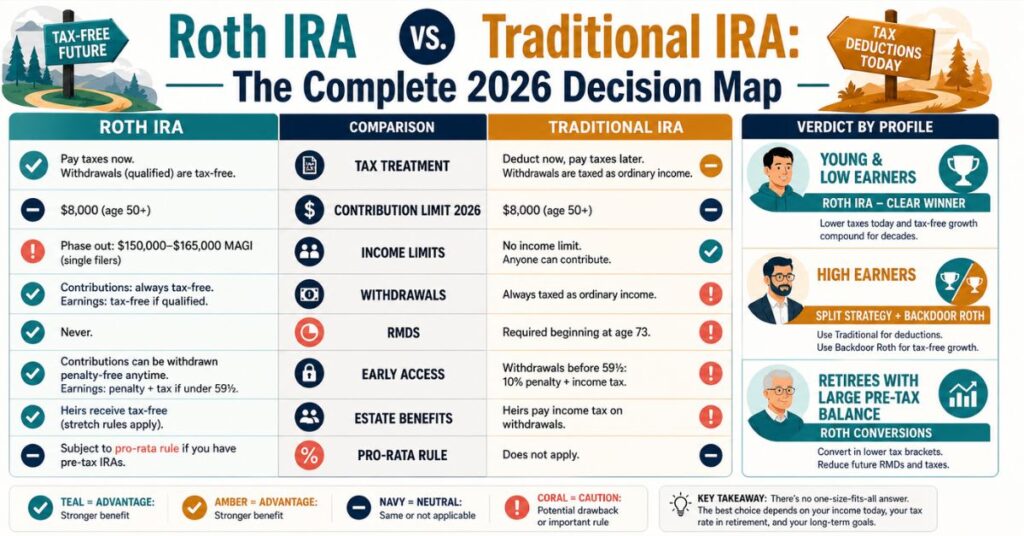

| Account Type | Annual Contribution | Growth (25 yrs, 7%) | Tax on Withdrawal | After-Tax Value |

|---|---|---|---|---|

| Roth IRA | $7,000 (after-tax) | $454,513 | $0 | $454,513 |

| Traditional IRA | $7,000 (pre-tax) | $454,513 | 22% = ~$100,000 | $354,513 |

| Traditional IRA + investing the tax savings separately | ~$5,460 net | Complex | Varies | ~$400,000–$430,000* |

Illustrative calculations. The comparison narrows when you invest the traditional IRA’s annual tax savings separately. This is precisely why equal tax rates produce equal outcomes. For educational purposes only.

Dimension 2 — Income Limits: Who Can Contribute?

Traditional IRA: Anyone with earned income can contribute — no income limit on the contribution itself. The tax deductibility phases out at higher incomes if you (or your spouse) have a workplace retirement plan:

- 2026 phase-out (single filer with workplace plan): $77,000–$87,000 MAGI

- 2026 phase-out (married filing jointly, you have workplace plan): $123,000–$143,000 MAGI

Above these limits, you can still contribute — but it’s non-deductible (after-tax basis).

Roth IRA: Direct contributions are restricted for higher earners.

- 2026 phase-out (single filers): $150,000–$165,000 MAGI

- 2026 phase-out (married filing jointly): $236,000–$246,000 MAGI

- Above these limits: cannot contribute directly to a Roth IRA — but the backdoor Roth strategy (covered below) solves this.

| Filing Status | Roth Contribution Limit | Roth Phase-Out | Traditional Deductibility Phase-Out (with workplace plan) |

|---|---|---|---|

| Single | $7,000 ($8,000 age 50+) | $150,000–$165,000 | $77,000–$87,000 |

| Married Filing Jointly | $7,000 per person | $236,000–$246,000 | $123,000–$143,000 |

| Married — only one spouse has workplace plan | $7,000 per person | $236,000–$246,000 | $230,000–$240,000 (non-covered spouse) |

Source: IRS Publication 590-A, 2026. MAGI thresholds adjusted annually.

Dimension 3 — Withdrawal Rules: Flexibility and Penalties

Traditional IRA: Withdrawals before age 59½ trigger a 10% early withdrawal penalty plus ordinary income tax. After 59½, withdrawals are penalty-free but still fully taxed as ordinary income. No flexibility to access contributions early without penalty.

Roth IRA — the structural flexibility advantage: Contributions (not earnings) can be withdrawn at any time, at any age, penalty-free and tax-free — because they were already taxed. Earnings before age 59½ and before the 5-year rule is met are subject to penalty and tax. After age 59½ AND after the Roth IRA has been open for at least 5 tax years, all withdrawals are completely tax-free.

Here’s what that flexibility means in practice:

Sandra, 54, contributes $8,000/year to her Roth IRA. After 8 years, her account holds $64,000 in contributions and $47,000 in earnings. She faces an unexpected medical bill of $30,000. Sandra withdraws $30,000 from her Roth IRA — all from contributions, not earnings — with zero tax and zero penalty. The same $30,000 withdrawal from a traditional IRA would trigger $6,600 in income tax (at 22%) plus a $3,000 early withdrawal penalty — $9,600 in total costs. The Roth’s flexibility saves Sandra $9,600 in a genuine emergency.

Dimension 4 — Required Minimum Distributions: The Retirement Tax Trap

Traditional IRA: Starting at age 73, the IRS requires minimum annual withdrawals based on your account balance and a life expectancy factor. RMDs are taxed as ordinary income whether you need the money or not. Missing an RMD triggers a 25% penalty on the amount that should have been withdrawn.

The real danger: many retirees build large traditional IRA balances during their working years without thinking through the implications. A $1.5M traditional IRA generates approximately $58,000 in year-one RMDs. Added to Social Security income and any pension, this can easily push total taxable income well above $100,000 — triggering higher Medicare IRMAA surcharges, increased Social Security taxation, and a higher marginal bracket than the retiree ever saw during their working years.

To understand exactly how your Social Security income is calculated and how it interacts with these taxable withdrawals, read our complete guide on how Social Security is calculated.

Roth IRA: No RMDs during the original owner’s lifetime — ever. The money can sit and grow completely tax-free to age 90 or beyond. This also makes the Roth IRA a powerful estate planning tool — assets pass to heirs with tax-free treatment for up to 10 years under SECURE 2.0 rules.

Common Mistake: Building a retirement portfolio entirely in traditional pre-tax accounts and never thinking about RMDs. The person who accumulates $2M in a traditional IRA, retires at 65, and does no Roth conversion planning will face mandatory taxable withdrawals of $75,000+ starting at age 73 — potentially landing in a higher tax bracket than they were in during peak earning years. Start thinking about RMD management in your 50s, not your 70s.

Dimension 5 — Estate Planning and Legacy: Passing Wealth to Heirs

Traditional IRA: Under SECURE 2.0, non-spouse beneficiaries must withdraw all inherited traditional IRA funds within 10 years — and every dollar is taxed at their ordinary income rate. If your children are in their peak earning years (40s–50s) when they inherit, those withdrawals may be taxed at 22%, 24%, or even 32%.

Roth IRA: Inherited Roth IRAs also require withdrawal within 10 years — but all distributions are completely tax-free.

James and William are brothers who each inherit $400,000 from their parents. James inherits a traditional IRA; William inherits a Roth IRA. Both are 48 years old and in the 24% federal tax bracket. Both withdraw $40,000/year for 10 years. James pays 24% income tax on each withdrawal: $9,600/year × 10 years = $96,000 in total federal income tax. After-tax inheritance: $304,000. William pays zero. After-tax inheritance: $400,000. The Roth IRA delivers $96,000 more after-tax value — from the exact same inherited balance — simply due to account type.

The Tax Bracket Prediction Problem — Why This Decision Is Hard

The theoretically correct answer requires predicting your future tax rate — which is genuinely uncertain. Here’s how to think through it honestly.

The case for expecting higher retirement tax rates: Current federal debt levels create pressure for future tax increases — many tax experts believe rates will be higher in 10–20 years. Large pre-tax 401k/IRA balances generate substantial RMDs that may push retirement income higher than anticipated. Social Security income can become up to 85% taxable, creating an effective marginal rate “bump” that catches many retirees off guard. Medicare IRMAA surcharges function as a de facto high-income tax on retirees.

The case for expecting lower retirement tax rates: Retirement income is often lower than peak working income. No more payroll taxes (FICA) in retirement — a significant reduction in effective burden. Standard deductions, medical expense deductions, and careful withdrawal sequencing may reduce taxable income into the 12% bracket for some retirees.

The practical resolution — tax diversification: Given genuine uncertainty, maintaining accounts in all three tax buckets provides maximum flexibility:

- Pre-tax bucket (traditional IRA, 401k): taxed on withdrawal — good if rates fall

- After-tax bucket (Roth IRA, Roth 401k): never taxed again — good if rates rise

- Taxable bucket (brokerage): taxed on dividends and capital gains — flexible in any scenario

Tax diversification isn’t about predicting the future — it’s about removing the need to predict correctly.

Pro Tip: If you genuinely cannot determine which account wins for you, open both. Contribute to your traditional 401k for the employer match and current deduction, then open a Roth IRA and contribute $7,000–$8,000/year. This simple split provides tax diversification without requiring a definitive forecast. Many financial planners consider this the default recommendation for anyone in the 22–24% bracket who is uncertain.

The Verdict — Which IRA Wins for Your Specific Situation

Here’s the honest, profile-by-profile verdict. Find yours and read carefully.

Profile 1 — Young, Early-Career Worker (20s–30s, income below $60,000) Winner: Roth IRA — unambiguous.

You’re in the lowest tax brackets of your career (10–12% today). You have decades of tax-free compounding ahead. There’s a high probability that tax rates will be higher in your peak earning years and again in retirement. Pay 10–12% tax now to avoid paying 22–32% tax later. If there were one piece of advice to lock in early, it’s this: start a Roth IRA now. Understand why in our guide on why retirement wealth planning starts now.

Profile 2 — Mid-Career Worker (40s, income $60,000–$150,000) Winner: Roth IRA, with traditional for employer match.

Still below peak earnings — tax rates are likely to rise in your highest-income years. Capture the full employer 401k match (traditional) for the free money, then direct your IRA contributions to Roth. The long time horizon amplifies Roth’s compounding advantage.

Profile 3 — Peak Earner in 50s (income $150,000–$250,000+) Winner: Split — traditional 401k + Roth IRA (via backdoor) + evaluate Roth 401k.

At the 24–32% bracket, the current tax deduction has real value. But your large pre-tax balances are creating growing RMD risk. Traditional 401k contributions reduce current taxes. A backdoor Roth IRA simultaneously builds the tax-free bucket for future RMD management. The split strategy maximizes both current deduction and future flexibility.

Profile 4 — Near-Retirement (60s, within 5 years of retirement) Winner: Situational — evaluate your pre-tax balance vs. projected retirement income.

Calculate your expected retirement income: Social Security + pension + RMDs from existing pre-tax accounts. The timing of your Social Security claim has a major effect on this calculation — see our full guide on the best age to claim Social Security benefits before building your income projection. If projected income is high (above $80,000 single / $130,000 married), there’s a strong case for Roth contributions and Roth conversions now. This profile benefits most from a specific projection modeled with a fee-only financial advisor.

Profile 5 — Retiree (65+) With Large Pre-Tax Balances Winner: Roth conversion strategy — convert traditional funds to Roth.

No longer making new contributions in most cases. Focus shifts to Roth conversions in the pre-RMD window: converting $30,000–$50,000/year while keeping taxable income in the 12–22% bracket reduces the future RMD burden, reduces Social Security taxation, and reduces IRMAA premiums. (More detail on this below.)

Profile 6 — Estate-Focused Retiree (65+ With Children or Heirs) Winner: Roth IRA — not even close.

Every dollar converted to Roth before death is a dollar saved from ordinary income tax for your heirs. The Roth IRA is the single most efficient wealth transfer vehicle for middle-income families with meaningful retirement assets. Not sure where you stand on overall retirement readiness? Take our retirement readiness quiz to identify your gaps before building your estate strategy.

| Reader Profile | Recommended Primary Account | Primary Reason |

|---|---|---|

| Young, low income (20s–30s) | Roth IRA | Pay low rates now; decades of tax-free growth |

| Mid-career, moderate income | Roth IRA + traditional 401k match | Rising rates ahead; RMD avoidance |

| Peak earner, high income | Traditional 401k + Backdoor Roth IRA | Current deduction + tax diversification |

| Near-retirement, large pre-tax balance | Backdoor Roth + begin conversions | RMD risk management |

| Retired, large pre-tax balances | Roth conversion strategy | Pre-RMD window optimization |

| Estate-focused retiree | Roth conversion to pass tax-free wealth | Heir inheritance tax advantage |

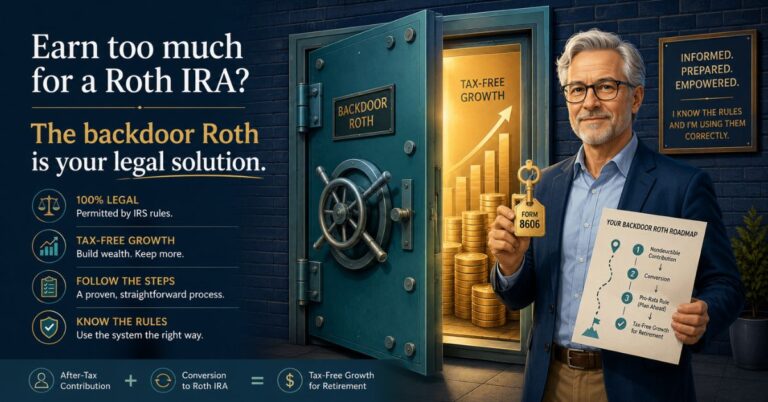

The Backdoor Roth IRA — The High Earner’s Solution

For the growing segment of readers who earn above the Roth contribution limits, the backdoor Roth is the most important strategy in this entire post. Here’s exactly how it works.

What is it?

A legal two-step process allowing high earners above the Roth income limits to access the Roth IRA’s tax-free benefits. It’s not a loophole — it was explicitly approved by the IRS and confirmed in Congressional reports.

Step 1: Contribute to a non-deductible traditional IRA.

Anyone with earned income can contribute to a traditional IRA regardless of income — there is no income limit on the contribution itself, only on the deductibility. For a high earner above the Roth limits, this contribution is non-deductible (after-tax basis). Contribute $8,000 (age 50+) or $7,000 (under 50). File IRS Form 8606 to establish the after-tax basis — this is critical to avoid double taxation later.

Step 2: Convert the traditional IRA to a Roth IRA.

After contributing, immediately convert the account to a Roth IRA. Because the contribution was non-deductible (already taxed), the conversion triggers no income tax. The “immediately” timing matters: the longer you wait, the more any earnings inside the account accumulate — and those earnings are taxable on conversion.

The pro-rata rule — the critical complication.

If you have other pre-tax traditional IRA balances (a rollover IRA or prior deductible contributions), the IRS applies the pro-rata rule, treating all your IRA accounts as one pool. If you have $90,000 in a pre-tax rollover IRA and add $10,000 in non-deductible contributions, then convert the $10,000 — only 10% of the conversion is treated as after-tax. The other 90% is taxable. The solution: roll your pre-tax IRA balances into your employer’s 401k before executing the backdoor Roth — most 401k plans accept incoming rollovers from traditional IRAs.

Jennifer, 54, earns $190,000 as a physician assistant — above the $165,000 Roth income limit. She has no existing traditional IRA balances. Jennifer contributes $8,000 to a traditional IRA (non-deductible), waits 2 weeks, then converts the $8,000 to her Roth IRA. She pays zero income tax on the conversion and files Form 8606. Repeated annually, Jennifer adds $8,000/year in completely tax-free Roth savings. Over 11 years to age 65 at 7% return, that becomes approximately $125,000 in tax-free retirement wealth — available without RMDs for life.

Roth Conversions — Transforming Traditional IRA Money Into Tax-Free Wealth

Roth conversions are the most powerful tax optimization tool available to retirees with large pre-tax accounts — and the most neglected. Here’s the essential framework.

What is a Roth conversion?

Moving money from a traditional IRA (or pre-tax 401k) to a Roth IRA by paying income tax on the converted amount in the year of conversion. Unlike the backdoor Roth — which converts non-deductible after-tax contributions — a Roth conversion involves pre-tax money and triggers income tax on every dollar converted. There is no income limit on conversions — anyone can convert any amount at any time.

When does a Roth conversion make strategic sense?

The years between retirement and age 73 (when RMDs begin) often represent the lowest-income period of a retiree’s life. Without employment income and without RMDs, taxable income may drop to $30,000–$60,000/year. Converting $20,000–$50,000/year from traditional to Roth during this window often stays in the 12–22% bracket — while every dollar converted now potentially avoids forced withdrawal at 24–32% when RMDs arrive at 73.

The IRMAA guardrail: Medicare IRMAA surcharges begin at $106,000 of income for single filers and $212,000 for married filers in 2026. Roth conversions add to MAGI — and a large conversion can trigger IRMAA two years later (IRMAA uses income from 2 years prior). Optimal conversion amounts stay below these thresholds.

Thomas, 66, retired with $1.1M in a traditional IRA and $180,000 in a Roth IRA. He receives $28,000/year in Social Security and his expenses are $65,000/year. His taxable income without conversion is approximately $50,000 — solidly in the 12–22% range. Thomas converts $45,000/year from traditional to Roth from ages 66–72 (7 years). Total converted: $315,000, taxed at an average 20% = $63,000 in conversion taxes paid over 7 years. At 73, his traditional IRA balance is significantly lower — reducing his year-one RMD from roughly $42,000 to $28,000. That’s $14,000 less in forced taxable income annually. Over a 15-year retirement, the tax savings from reduced RMDs and IRMAA avoidance are estimated to exceed the $63,000 paid in conversion taxes — and Thomas has built $315,000+ in additional Roth assets that pass tax-free to his heirs.

Pro Tip: The single best time to evaluate a Roth conversion is December of each year — when you know your full annual income and can calculate exactly how much you can convert while staying in your target bracket. Converting “up to the bracket ceiling” rather than a fixed arbitrary amount maximizes the tax efficiency of each conversion.

The Seven Practical Factors — Your Final Decision Checklist

Apply these to your own situation:

Factor 1 — Your Current Tax Bracket

- 10–12%: Roth IRA almost always wins — pay the lowest rates of your career now

- 22%: Roth IRA usually wins — still relatively low; future rates likely higher or equal

- 24%: Lean toward split — meaningful current deduction; evaluate pre-tax balance carefully

- 32%+: Traditional often wins for current contributions; focus Roth strategy on conversions in future lower-income years

Factor 2 — Your Expected Retirement Tax Bracket

Expect lower rates → traditional preferred. Expect higher or same rates → Roth preferred. Genuinely uncertain → split contributions and eliminate the need to predict.

Factor 3 — Your Existing Pre-Tax Balance

Under $300,000 → flexibility to use either. $500,000+ → Roth increasingly valuable to avoid future RMD tax bombs. $1M+ → Roth conversions should begin immediately upon retirement.

Factor 4 — Your Time Horizon

15+ years to retirement → Roth is more valuable; more time for tax-free compounding. 5–10 years → evaluate more carefully; traditional deduction has more relative value. At or in retirement → focus on Roth conversions rather than contributions.

Factor 5 — Your Estate Planning Goals

Want to leave the most after-tax wealth to heirs → Roth IRA is significantly superior. No estate planning concern → pure personal tax math drives the decision.

Factor 6 — Your Income vs. Roth Limits

Below $150,000 single / $236,000 married → direct Roth contributions available. Above limits → backdoor Roth. Well above limits with large 401k balance → Mega Backdoor Roth via after-tax 401k contributions.

Factor 7 — Your Flexibility Need

Need the option to access money before 59½ without penalty → Roth IRA is dramatically superior — contributions are accessible anytime. No anticipated early access need → both accounts work equally on this dimension.

Understanding all of these terms in one place is easier with a dedicated reference. Our retirement planning vocabulary guide defines all 60 key terms — including MAGI, RMD, IRMAA, pro-rata rule, and the 5-year rule — in plain English.

Frequently Asked Questions

Q: I’m 55 with a large 401k balance and no Roth account at all. Is it too late to start a Roth IRA?

Not at all — and starting now may be exactly right. A Roth IRA opened at 55 gives you 10+ years of tax-free growth before the typical retirement date, plus tax-free withdrawals from 59½ onward. Starting the Roth clock now begins the 5-year rule period, ensuring qualified tax-free distributions when you need them. Your large pre-tax 401k balance also makes the Roth IRA’s RMD avoidance increasingly valuable — you want to balance pre-tax accumulation with tax-free accumulation going forward.

Q: My financial advisor told me traditional IRA is always better because of the tax deduction. Is that right?

Not universally — and that blanket statement suggests your full situation may not have been modeled. The traditional IRA’s deduction is genuinely valuable when your current rate is significantly higher than your expected retirement rate. But for someone building large pre-tax balances who will face substantial RMDs, the Roth often wins on a lifetime after-tax basis even when the current deduction appears more valuable in isolation. Ask your advisor to model the full after-tax, after-RMD comparison over your full retirement horizon. The answer may surprise you.

Q: Can I have both a Roth IRA and a traditional IRA at the same time?

Yes — you can hold both simultaneously. The $8,000 annual limit (age 50+) applies to the combined total across all your IRAs, not per account. So you can contribute $4,000 to a traditional IRA and $4,000 to a Roth IRA in the same year, or any other split totaling $8,000. Many people use this split intentionally for tax diversification — taking some current deduction while building tax-free wealth.

Q: If the Roth is so good, why does anyone use a traditional IRA?

The traditional IRA wins in legitimate situations: when your current tax rate is genuinely high (32%+) and retirement rates are likely lower; when you need the current deduction to reduce taxable income below a specific threshold (IRMAA, Social Security taxation, credit phase-outs); and when you cannot afford to pay the full tax on Roth contributions now. It’s not obsolete — it’s simply the right tool for different circumstances.

Q: What is the 5-year rule for Roth IRAs and why does it matter?

The 5-year rule requires that a Roth IRA be open for at least 5 tax years before earnings can be withdrawn tax-free — even after age 59½. The clock starts January 1st of the tax year for which you made your first Roth IRA contribution. Open a Roth in 2026 (for the 2026 tax year) and the window closes January 1, 2031. After that date AND after reaching 59½, all Roth withdrawals are completely tax-free. Crucially, the 5-year rule only affects earnings — contributions can always be withdrawn penalty-free at any time.

The Bottom Line

The Roth vs. traditional IRA debate comes down to one core question — and five structural advantages that often settle it before you even get to the math.

The traditional IRA wins when your current tax rates genuinely exceed your expected retirement rates. The Roth IRA wins when retirement rates equal or exceed today’s — and it holds an additional edge through no RMDs, flexible withdrawal rules, and dramatically superior estate planning benefits that compound in value for anyone building meaningful retirement wealth.

For most middle-income Americans in the 22–24% bracket, the honest answer points toward Roth — especially for anyone who hasn’t yet started, anyone with a growing pre-tax balance, and anyone who wants to leave tax-free wealth to heirs.

For high earners, the split strategy (traditional 401k + backdoor Roth) captures both the current deduction and the tax-free bucket. For retirees with large pre-tax balances, the Roth conversion in the pre-RMD window is the most valuable tax strategy most people have never used.

The final step is knowing your full retirement picture — how much you need, what your income sources look like, and whether your current savings rate is on track. Our guide on how to set your retirement number is the logical next step once your IRA strategy is clear.

The Roth vs. traditional debate has no universal winner — but it has a personal winner for you. You now have everything you need to find it.

Disclaimer:The content on RetireWealthPath.com is for informational and educational purposes only and does not constitute financial, tax, or legal advice. IRA contribution limits, income phase-out thresholds, Roth conversion rules, RMD requirements, IRMAA thresholds, and all other figures referenced in this article reflect 2026 IRS guidelines and are subject to change. Tax brackets and rates referenced are federal only — state income taxes vary and may significantly affect the analysis. All calculations, named examples, and strategic recommendations are for illustrative and educational purposes only and do not represent guaranteed outcomes. Always consult a qualified financial professional, CPA, or tax advisor before making IRA contribution, conversion, or withdrawal decisions.