How to Set Your Retirement Number (Step-by-Step Guide 2026)

Most people have no idea what their retirement number is. They have a vague sense that it should be “a lot.” That vagueness is expensive.

Here is the thing — knowing how to set your retirement number sounds like something only a financial advisor can do. A complex formula. A proprietary calculation. A number that lives inside an expensive spreadsheet you never see.

It is not. Your retirement number is simply the amount of savings needed to generate the income you want, for as long as you need it. That is a math problem — and math problems have answers.

By the time you finish this post, you will have three things: a clear method for calculating your number, a reality-check framework for what to do if it feels out of reach, and a concrete first action step you can take this week.

An imperfect number you actually use beats a perfect number you never calculate. Let’s start with the method that changed how millions of people think about retirement — and it involves one elegant rule.

Start Here — The 4% Rule and What It Actually Means

The 4% rule is the most widely cited retirement planning guideline in existence. Most people have heard of it. Very few understand it well enough to actually use it.

The rule comes from the 1994 “Trinity Study” — research by three finance professors at Trinity University who analyzed decades of historical market data. Their conclusion: a retiree who withdraws 4% of their portfolio in year one, then adjusts that amount for inflation each subsequent year, has a very high probability of not outliving their money over a 30-year retirement.

The formula is simple:

Annual expenses ÷ 0.04 = Retirement number

Take Linda, a 56-year-old marketing manager from Colorado. She estimates her retirement will cost $52,000 per year. Using the 4% rule: $52,000 ÷ 0.04 = $1,300,000. That is Linda’s starting retirement number.

But here is where most people stop — and they should not. What if you have other income sources coming in?

The modified formula accounts for that:

(Annual expenses − Annual guaranteed income) ÷ 0.04 = Portfolio needed

Linda expects $18,000 per year in Social Security. So her portfolio only needs to cover $34,000 per year: $34,000 ÷ 0.04 = $850,000. That is a very different — and far more achievable — number.

Pro Tip: Always calculate your retirement number twice — once without Social Security (your worst-case target) and once with it (your realistic target). The gap between these two numbers is your “Social Security cushion” — and it is often larger than people expect.

The 4% rule gives you a starting number — not a final verdict. Your real number requires a few more layers of personalization. That is exactly what the next section covers.

The Five Inputs That Determine YOUR Number

No formula works without accurate inputs. These five variables are what make a retirement number personal — and estimating each one honestly is what separates a useful number from a meaningless one.

Input 1 — Your Retirement Age

Earlier retirement means longer the money must last — which means a larger portfolio is required. But the effect compounds in two directions simultaneously: every year earlier you retire both adds a year of withdrawals and removes a year of contributions and growth.

The 4% rule was designed for 30-year retirements. If you plan to retire before 60, many financial planners now recommend using a 3.5% withdrawal rate — or even 3% — to account for the longer time horizon. The table below shows the difference this makes.

| Retirement Age | Est. Years in Retirement | Required Portfolio (4% Rule) | Required Portfolio (3.5% Rule) |

|---|---|---|---|

| 55 | ~35 years | $1,250,000 | $1,428,000 |

| 60 | ~30 years | $1,250,000 | $1,428,000 |

| 65 | ~25 years | $1,250,000 | $1,428,000 |

| 70 | ~20 years | $1,000,000* | $1,100,000* |

*Based on $50,000/year lifestyle need. Source: Bengen (1994) and updated research. For illustrative purposes only. The 4% rule is a guideline, not a guarantee.

Rule of thumb: If you plan to retire before 62, use the 3.5% withdrawal rate as your baseline to build in a safety margin.

Input 2 — Your Estimated Annual Retirement Expenses

This is the single most important input — and the most commonly misjudged. Conventional wisdom says you will need 70–80% of your pre-retirement income. Modern research suggests 90–100% is safer, especially in the active early years of retirement when people tend to spend the most.

Here is a practical framework for estimating your number honestly.

Expenses that typically decrease in retirement:

- Mortgage payments (if your home is paid off before you retire)

- Commuting and work-related costs

- Payroll taxes — you stop paying FICA when you stop working

- Retirement account contributions — you are withdrawing, not contributing

- Life insurance — if children are grown and the mortgage is gone

Expenses that typically increase in retirement:

- Healthcare and prescription costs — often significantly

- Travel and leisure, especially in ages 60–75

- Home maintenance and aging-in-place modifications

- Gifts and financial support to adult children or grandchildren

- Long-term care costs, especially after age 75

The smartest approach is to think about retirement spending in three phases: the go-go years (ages 60–75, highest spending), the slow-go years (ages 75–85, somewhat lower), and the no-go years (ages 85+, lower activity but higher healthcare costs). Build a rough budget for each phase rather than assuming a flat annual number throughout.

Input 3 — Your Expected Income Sources

Every dollar of guaranteed income you have coming in is a dollar your portfolio does not need to generate. This one input shifts retirement math more dramatically than almost anything else.

Common retirement income sources to account for:

- Social Security — use your actual SSA.gov estimate, not a generic figure

- Pension — increasingly rare in the private sector, but significant if you have one

- Rental income from investment real estate

- Part-time work or consulting income, especially in the first 5–10 years of retirement

- Annuity payments if you own one

- Royalties or business income if applicable

Here is a figure worth memorizing: every $1,000 per month in guaranteed income reduces your required portfolio by $300,000 using the 4% rule. If you have a pension and Social Security together producing $3,000 per month, your required portfolio drops by $900,000 compared to someone with no guaranteed income at all.

Input 4 — Your Life Expectancy

This is the uncomfortable variable most people prefer to skip. Do not skip it.

A 65-year-old American man has a 50% chance of living to 85. A woman has a 50% chance of living to 88. A married couple at 65 has a 50% chance that at least one spouse lives to 92. The real retirement risk is not dying — it is outliving your money.

Use age 90 as your planning baseline. If you are in excellent health or have a family history of longevity, plan to 95. Every additional year of life expectancy adds roughly 2–3% to the portfolio needed — which is why this input is worth thinking through honestly rather than optimistically.

You can get a personalized estimate using the SSA’s life expectancy calculator at ssa.gov/planners/lifeexpectancy.

Input 5 — Your Inflation Assumption

Money loses purchasing power over time. $52,000 today will need to be roughly $94,000 in 30 years just to buy the same things, assuming 2% average annual inflation. That is not a worst case — that is a modest baseline.

“Retirement inflation” can actually run higher than general inflation because healthcare costs historically rise faster than the Consumer Price Index. Use 2.5–3% as your planning assumption for general expenses and 5–6% for healthcare-specific costs.

The good news: the 4% rule already accounts for historical average inflation in its original design — so if you are using the formula correctly, inflation is partially built in. For healthcare costs, add the buffer separately.

Three Ways to Calculate Your Number — Choose Your Style

Different people have different comfort levels with financial math. Here are three approaches — quick, standard, and comprehensive — so you leave with a method you will actually use.

Method 1 — The Quick Formula (5 Minutes)

For anyone who wants a ballpark number today.

Step 1: Estimate your annual retirement spending. If you are not sure, use 90% of your current gross income as a starting estimate.

Step 2: Subtract your expected annual Social Security income. Check SSA.gov for your personalized estimate.

Step 3: Divide the remaining gap by 0.04.

Example: $60,000 estimated spending − $20,000 Social Security = $40,000 portfolio gap. $40,000 ÷ 0.04 = $1,000,000 target portfolio.

Time required: 5 minutes, one piece of paper, a phone calculator. This is your starting point — not your final answer.

Method 2 — The Income Replacement Method (20 Minutes)

For a more refined estimate that accounts for your income and healthcare costs.

Step 1: Calculate your current gross annual income.

Step 2: Multiply by your replacement rate. Use 85% as a default; adjust up if you plan to travel heavily, down if you plan to live simply.

Step 3: Subtract all confirmed annual guaranteed income — Social Security, pension, rental income, any annuity payments.

Step 4: Divide by your withdrawal rate. Use 4% for a 30-year retirement; 3.5% for 35+ years.

Step 5: Add a healthcare buffer: $200,000 for singles; $350,000 for couples (based on Fidelity 2024 healthcare cost estimates).

Example: $85,000 income × 85% = $72,250 needed annually. Minus $22,000 Social Security = $50,250 portfolio gap. $50,250 ÷ 0.04 = $1,256,250. Plus $350,000 healthcare buffer = $1,606,250 comprehensive target.

Method 3 — The Expense-Based Method (1–2 Hours)

For the most accurate, personalized number you can get without a financial advisor.

Step 1: Build a detailed retirement budget. List every expected expense category with a monthly dollar amount.

Step 2: Multiply total monthly expenses by 12 for your annual retirement income need.

Step 3: Subtract all guaranteed income sources.

Step 4: Divide by your appropriate withdrawal rate.

Step 5: Add buffers for healthcare ($200,000–$350,000), long-term care ($200,000–$400,000 depending on your situation), and a 10–15% unexpected expenses cushion.

This method requires the most work — but it produces the most reliable, personalized number you can build on your own. Consider pairing it with a fee-only financial advisor for validation before you retire.

Common Mistake: Calculating your retirement number once and never revisiting it. Life changes — divorce, inheritance, health diagnoses, career shifts, housing decisions — all meaningfully shift your number. Recalculate every 3–5 years during your saving years, and again after every major life event.

Reality Check — What to Do When the Number Feels Impossible

Many readers will calculate their number and feel a wave of panic. That is a completely normal reaction — and it does not mean you are out of options.

Surveys consistently show that most Americans feel behind on retirement savings. Feeling behind is not the same as being stuck. You have more levers available than you probably realize — and most of them can be combined.

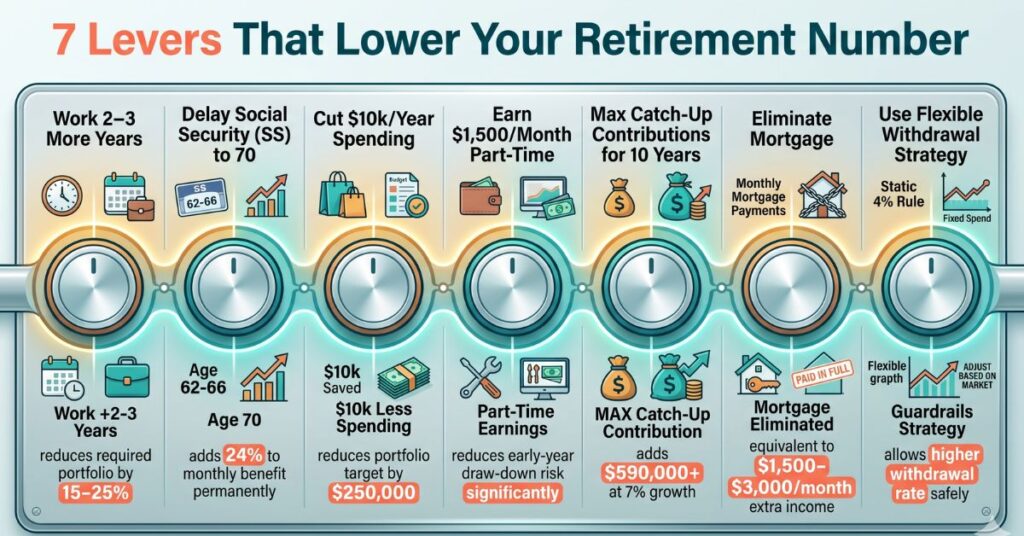

Here are seven genuine levers that can lower your required number or close the gap between where you are and where you need to be.

Lever 1 — Work 2–3 More Years Than Planned

Working until 65 instead of 62 does three things at once: it adds more contributions to your portfolio, avoids withdrawals for longer, and significantly increases your Social Security benefit. The combined effect on portfolio sustainability is dramatic — often more impactful than any single savings decision.

Lever 2 — Delay Social Security Claiming

Every year you delay past your Full Retirement Age (67 for most people) adds 8% to your monthly benefit permanently. Delaying from 67 to 70 adds 24% — which reduces the portfolio burden by hundreds of thousands of dollars over a long retirement. This one decision is often worth more than years of additional contributions.

Lever 3 — Reduce Planned Retirement Spending

Cutting $10,000 per year from your planned retirement budget reduces your required portfolio by $250,000 using the 4% rule. Geographic arbitrage — retiring in a lower cost-of-living area or state — is the single most powerful lifestyle lever available to most retirees.

Lever 4 — Add Part-Time Income in Early Retirement

Even $1,500 per month ($18,000 per year) in part-time consulting or work reduces your portfolio draw-down dramatically during the critical early years when sequence-of-returns risk is highest. You do not need to fully replace your income — even partial income has an outsized effect on portfolio longevity.

Lever 5 — Maximize Contributions Aggressively Now

If you are 50 or older, catch-up contributions allow $31,000 per year in a 401(k) and $8,000 in an IRA. Maxing both for 10 years at 7% average annual growth adds over $590,000 to your portfolio. That is a number worth printing out and taping to your bathroom mirror.

Lever 6 — Eliminate Your Mortgage Before Retirement

Entering retirement with a paid-off home is the equivalent of generating an extra $1,500 to $3,000 per month — without needing a single additional dollar in savings. Paying off your mortgage aggressively in your final working years is one of the highest-return, zero-risk moves in retirement planning.

Lever 7 — Use a Flexible Withdrawal Strategy

A “guardrails” approach — spending somewhat less in down market years and somewhat more in strong years — can allow a higher starting withdrawal rate with a lower risk of running dry. This flexibility reduces the required starting portfolio compared to a fixed-withdrawal approach and is increasingly the recommendation of modern financial planners over the rigid 4% rule.

| Lever | The Action | The Impact |

|---|---|---|

| 1. Work longer | Retire at 65 instead of 62 | Reduces required portfolio by 15–25% |

| 2. Delay Social Security | Claim at 70 instead of 67 | Adds 24% to monthly benefit permanently |

| 3. Reduce spending | Cut $10,000/year from budget | Reduces portfolio target by $250,000 |

| 4. Earn part-time income | Earn $1,500/month in early retirement | Significantly reduces early-year draw-down |

| 5. Max catch-up contributions | Max 401(k) + IRA for 10 years | Adds $590,000+ at 7% average growth |

| 6. Pay off mortgage | Enter retirement debt-free | Equivalent to $1,500–$3,000/month extra |

| 7. Use flexible withdrawals | Adopt guardrails strategy | Allows higher withdrawal rate safely |

You have more control over your retirement number than you think. Each lever can be adjusted — and most can be combined for compounding effect.

From Number to Plan — Your Next Three Steps

Information without action is just entertainment. Here is a clear, low-friction path from “I now know my number” to “I am actually doing something about it.”

Step 1 — Write Your Number Down Today

Not in a spreadsheet you will never open. On a sticky note on your monitor. A note in your phone. The back of an envelope. The physical act of writing a specific number makes it real and creates the psychological commitment that keeps you moving toward it.

Your number: $_______________

Step 2 — Calculate Your Current Gap

Total retirement target − Current retirement savings = Your gap.

Then divide the gap by the number of months until your target retirement date. That monthly figure is roughly what you need in new contributions to close the gap — assuming 7% average annual returns.

Example: $900,000 target − $280,000 currently saved = $620,000 gap. 180 months until retirement (15 years). With 7% average annual growth, you need approximately $1,400 per month in new contributions to close that gap. Without investment growth, the number would be $3,444/month — so compounding is doing a significant portion of the work.

Step 3 — Take One Account Action This Week

Not a meeting with an advisor. Not a full financial overhaul. One action this week:

- If you are not capturing your full employer match → increase your 401(k) contribution by 2% this week

- If you do not have a Roth IRA → open one at Fidelity, Vanguard, or Schwab this week — it takes about 15 minutes online

- If you have accounts but have not reviewed them in over a year → log in and check your investment allocation this week

Pro Tip: Use the “my Social Security” account at SSA.gov to pull your actual projected benefit before finalizing your retirement number. It takes 10 minutes and gives you a personalized figure based on your real earnings history — far more accurate than any generic estimate or calculator guess.

When to Use a Financial Advisor to Validate Your Number

Self-calculated numbers are excellent starting points. But they can miss complexity that costs money over time: tax sequencing, Social Security optimization strategies, pension coordination, estate planning considerations, and investment allocation fine-tuning.

Consider consulting a fee-only financial advisor to validate your number if any of these apply to you:

- Your household has multiple retirement account types — traditional, Roth, taxable brokerage, HSA, and pension

- You are within 5 years of your target retirement date

- You or your spouse has a significant health condition that affects life expectancy planning

- You have a complicated family situation — blended family, dependent adult children, or aging parents who may need financial support

- Your number feels genuinely unachievable and you want a professional second opinion on what levers are actually available to you

To find one, look at NAPFA.org (fee-only advisors), the Garrett Planning Network (hourly advisors), or SmartAsset’s advisor matching tool. A one-time retirement planning session typically costs $250–$500 per hour, or $1,500–$3,000 for a comprehensive plan. That is a fraction of what poor planning can cost over a 30-year retirement.

A financial advisor does not tell you what your number is — they help you stress-test the number you have already calculated and build a strategy around it. The work you have done in this post puts you in an excellent position to make that conversation genuinely useful.

FAQs About How to Set Your Retirement Number

What is a good retirement number for a 55-year-old with $200,000 saved?

It depends heavily on your lifestyle and income sources — but as a starting point: if you plan to retire at 65 on $50,000 per year and expect $18,000 per year in Social Security, your portfolio target is around $800,000. With $200,000 already saved, you have a $600,000 gap and 10 years — requiring roughly $3,500 per month in new contributions at 7% average growth. Aggressive, but not impossible, especially if you use catch-up contributions available at age 50.

Does the 4% rule still work in 2026?

It remains a useful starting framework, but many financial planners now suggest 3.5% for retirements longer than 30 years due to lower expected bond returns and longevity trends. The rule also assumes a diversified stock and bond portfolio — not all cash or all stocks. Use 4% as your initial estimate, then stress-test with a 3.5% scenario to see how much your target shifts.

Should I include my home equity in my retirement number calculation?

Generally no — unless you have a concrete plan to access it, such as downsizing to a less expensive home. Home equity is illiquid and does not generate income unless converted. If you plan to downsize and net $200,000 in proceeds, you can factor that in as a one-time addition to your portfolio. But do not count on a number you cannot easily spend when you need it.

How often should I recalculate my retirement number?

Recalculate every 3–5 years during your accumulation phase, and again after every major life event — marriage, divorce, inheritance, job change, significant health diagnosis, or housing decision. In the final 5 years before retirement, recalculate annually and begin stress-testing with a fee-only financial advisor at least once.

What if my retirement number is $2 million but I’ll only save $800,000?

First, check whether you have subtracted your guaranteed income sources — Social Security, pension, rental income — from your spending need. Many people have not, and this single adjustment often reduces the target dramatically. Second, run through the seven levers above: working a few extra years, delaying Social Security, trimming planned expenses, or adding part-time income can each shift the math more than you expect. Third, a fee-only advisor can often identify tax strategies and withdrawal sequencing approaches that extend a smaller portfolio further than a simple calculation suggests.

The Bottom Line

You came into this post with a vague sense that retirement requires “a lot.” You are leaving with a specific number — or at least a clear method for calculating one today.

Three things worth carrying with you:

- Your retirement number is a math problem, not a mystery — and you now have the formula to solve it.

- Guaranteed income sources dramatically reduce the portfolio you need to build. Social Security alone can shift your target by hundreds of thousands of dollars. Use your actual SSA.gov estimate, not a guess.

- If your number feels out of reach, you have more levers than you think — and most of them can be combined. Working two more years, delaying Social Security, and cutting $10,000 from your annual budget together can close a gap that feels impossible when viewed as a single mountain to climb.

Now that you have your number, the next step is understanding the accounts that will help you reach it. Start with Why Retire Wealth Planning Starts Now, or explore our Retirement Planning Vocabulary Guide if you want to make sure you are fluent in the terms that matter most on this journey.

The most expensive retirement number is not the one that feels too big — it is the one you never calculated.

Disclaimer: The content on RetireWealthPath.com is for informational and educational purposes only and does not constitute financial, tax, or legal advice. We are not licensed financial advisors. Calculations and examples in this post are for illustrative purposes only and do not represent guaranteed outcomes. The 4% rule is a guideline, not a guarantee — actual results depend on market performance, inflation, individual spending, and other factors. Always consult a qualified financial professional before making retirement planning decisions. Retirement planning involves risk and individual results will vary.