10 Retirement Myths Debunked [What Most People Get Wrong]

Most people spend more time planning a two-week vacation than they spend planning the 30 years that come after their last paycheck.

It sounds harsh, but it is true — and a big reason why is that retirement is surrounded by myths. Some come from well-meaning family members who retired in a different era.

Others come from outdated financial “rules” that no longer apply to today’s economy. A few are just wishful thinking that hardened into conventional wisdom over time.

This guide is not a lecture. It is a practical myth-busting resource for anyone who wants to replace dangerous assumptions with actionable truths — whether you are 35, 55, or somewhere in between.

These retirement myths affect people at every income level. They are not just mistakes made by people who are “bad with money.” They catch smart, hardworking people off guard every single day.

By the time you finish reading, you will have swapped out 10 retirement misconceptions for 10 things that are actually true — and that could save you thousands of dollars and years of stress.

Let’s start with the one that surprises people the most.

Myth #1: “I Need $1 Million to Retire Comfortably”

The Myth

You need exactly $1 million saved before you can even think about retiring.

The Truth

The right retirement number is deeply personal. It depends on your lifestyle, your location, your health, and your income sources — not on a headline figure that sounds impressive at dinner parties.

Here is a simple way to think about it. Financial planners often use something called the 4% rule, which suggests you can withdraw 4% of your portfolio per year without running out of money over a 30-year retirement. That means:

- $500,000 in savings supports $20,000 per year in portfolio withdrawals

- $750,000 supports $30,000 per year

- $1,000,000 supports $40,000 per year

But here is what those numbers leave out: Social Security, pensions, rental income, and part-time work all count toward your retirement income too.

Many retirees live comfortably on $35,000 to $50,000 per year in total household income — especially when they own their home, have Medicare, and have eliminated commuting and childcare costs.

Take Robert, a retired school administrator from Indiana. He retired at 64 with $620,000 saved and $1,800 per month in Social Security. His actual monthly expenses? $3,400. He has been comfortable for six years — without ever hitting that mythical $1 million mark.

Pro Tip: Before you fixate on a number, calculate your actual retirement budget first. Most people find their retirement expenses are 20 to 30 percent lower than their working expenses — no more commuting costs, work wardrobe, or payroll taxes.

The bottom line: The magic number is your number — not someone else’s headline.

Myth #2: “Social Security Will Cover My Basic Needs”

The Myth

Social Security was designed to be a full retirement income, so it should be enough to live on.

The Truth

Social Security was designed to replace roughly 40% of pre-retirement income for average earners — not 100%. It was always meant to be one leg of a three-legged stool, alongside personal savings and a pension.

The average monthly Social Security benefit in 2026 is approximately $1,907, which works out to about $22,884 per year. That keeps you above the federal poverty line — but not comfortably above it, and certainly not with much room for healthcare costs, housing, or anything else that rises in price as you age.

There is also a long-term concern worth knowing about. The Social Security trust fund is projected to face shortfalls by around 2033 without legislative changes, according to the SSA Trustees Report.

That does not mean Social Security will disappear, but it does mean future benefits could look different than they do today.

How Your Claiming Age Affects Your Benefit

| Claiming Age | % of Full Benefit | Est. Monthly Benefit | Annual Income |

|---|---|---|---|

| 62 (early) | 70% | $1,335 | $16,020 |

| 67 (full retirement age) | 100% | $1,907 | $22,884 |

| 70 (delayed) | 124% | $2,365 | $28,380 |

Source: Social Security Administration, 2026 average benefit estimates. Individual benefits vary based on earnings history.

Common Mistake: Claiming Social Security at 62 just because you can is one of the costliest retirement decisions many people make. Waiting just three more years to your full retirement age can add over $6,000 per year to your lifetime benefit.

Social Security should be the floor of your retirement income — not the ceiling.

Myth #3: “I’ll Spend a Lot Less Money in Retirement”

The Myth

Once you stop working, your expenses drop dramatically and money becomes easy to manage.

The Truth

Early retirement — roughly ages 60 to 75 — is often called the “go-go years” by financial planners. This is when most retirees are healthy, energetic, and eager to travel, pursue hobbies, visit grandchildren, and eat out regularly. For many people, these years cost more than their working years did.

Healthcare is the real wildcard. Fidelity estimates that the average couple needs $315,000 saved just to cover healthcare expenses in retirement — and that figure does not include long-term care.

Retirement spending typically follows what researchers call a “smile” pattern. Expenses are high in the early, active years. They dip somewhat in the quieter middle years. Then they climb sharply again late in retirement, driven by healthcare needs, prescription costs, home modifications, and sometimes assisted living.

Yes, some expenses disappear when you retire — your mortgage (if it is paid off), commuting costs, work clothes, and payroll taxes. But new ones take their place. Planning as if your expenses will simply shrink is one of the most common and painful retirement budget mistakes.

Pro Tip: Build a retirement budget before you retire, not after. Track your current spending for 90 days, remove work-related costs, and add estimated healthcare and leisure spending. This single exercise prevents the most common retirement budget shock.

Myth #4: “My Home Equity Is My Retirement Plan”

The Myth

“My house is worth $400,000 — that’s my retirement fund right there.”

The Truth

Home equity is illiquid. You cannot pay a grocery bill with square footage. And tapping into that equity is rarely as simple or profitable as it sounds.

Selling your home means you need somewhere else to live — which costs money. Downsizing works, but after buying or renting a smaller place, moving costs, and taxes, the net proceeds are often significantly less than expected. In high-cost areas, that gap can be surprisingly large.

Reverse mortgages are another option, but they come with substantial fees, interest that accrues over time, and real risks for heirs. They can be a useful tool in specific situations, but they are not a retirement strategy.

It is also worth remembering that real estate values are not guaranteed. The 2008 housing crash wiped out retirement plans for millions of people who had relied entirely on home equity as their financial safety net.

Your home is a valuable asset and a meaningful supplement to a retirement plan. It is not a substitute for one.

The bottom line: Your house is an asset, not a paycheck — and retirement requires a paycheck.

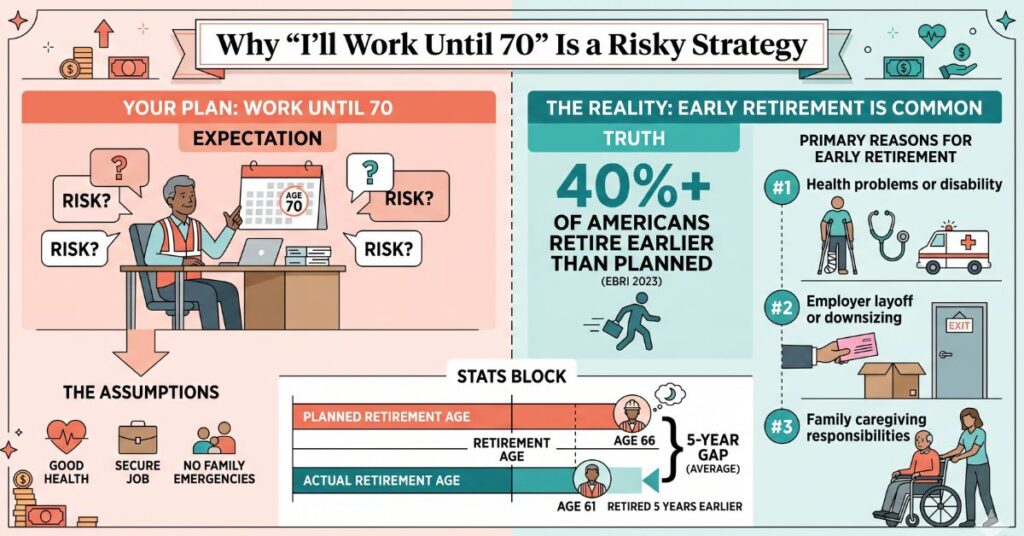

Myth #5: “I’ll Work Until I’m 70, So I Have Plenty of Time”

The Myth

Planning to work well into your late 60s gives you plenty of runway to save more money later.

The Truth

According to the Employee Benefit Research Institute, more than 40% of retirees leave the workforce earlier than they planned. The reasons are not laziness or poor planning. They are health problems, employer layoffs, and family caregiving responsibilities — things no one can fully anticipate or plan around.

Here is what the data actually shows:

- Over 40% of Americans retire earlier than planned (EBRI, 2023)

- The number one reason for unplanned early retirement: health problems or disability

- The number two reason: employer layoffs or downsizing

- The number three reason: family caregiving responsibilities

- The average actual retirement age in the U.S. is 61 — versus a planned retirement age of 66

- That is a five-year gap between intention and reality

Every year of planned “later saving” that does not happen is compound growth you will never recover. Being forced to retire at 58 instead of 70 with inadequate savings is not a hypothetical risk. It happens to real people every year.

Planning to work longer is a hope, not a strategy. Build a plan that works even if you have to stop at 60.

Myth #6: “A 401(k) and a Savings Account Are the Same Thing”

The Myth

Money is money — whether it is sitting in a savings account or a 401(k), it grows the same way.

The Truth

These two accounts are not remotely the same, and treating them as equivalent is one of the most expensive financial mistakes a working person can make.

A savings account earns interest — currently around 4 to 5% APY in 2026, though historically much lower. A 401(k) invests in the market and has historically returned 7 to 10% annually over long periods. But the gap goes beyond interest rates.

401(k) contributions are made pre-tax, which lowers your taxable income right now. If your employer offers a match — and the average employer match is around 4.7% of salary — that is essentially free money you leave on the table by keeping funds in a savings account instead.

Roth 401(k)s and Roth IRAs add another layer: that money grows completely tax-free. Every dollar you contribute grows without the government taking a cut when you withdraw it in retirement.

The Real Difference Over 20 Years

Consider this example. You invest $500 per month for 20 years.

- In a savings account at 4.5% interest: approximately $193,000

- In a 401(k) at a 7% average return, with an employer match: over $340,000

That is more than $147,000 in additional wealth from the exact same monthly contribution — simply by using the right account.

Leaving money in a savings account instead of a 401(k) is mathematically one of the most expensive “safe” decisions a person can make.

Myth #7: “I Should Move All My Money to ‘Safe’ Investments Before I Retire”

The Myth

The moment you retire, you should shift everything into bonds and cash so you do not risk losing money.

The Truth

A 65-year-old today has a statistically strong chance of living into their mid-to-late 80s. That is a 20 to 25-year investment horizon — longer than many people’s entire working careers. Managing your money as if you need it all tomorrow ignores that reality.

Inflation is the hidden danger here. Even at a modest 3% annual inflation rate, purchasing power is cut roughly in half over 24 years. A portfolio that earns 2% while inflation runs at 3.5% is losing real value every single year, even if the account balance looks stable on paper.

Common Mistake: Moving entirely to cash or bonds at retirement is sometimes called “reverse risk” — the risk of being too safe. If your portfolio earns 2% but inflation runs at 3.5%, you are quietly losing purchasing power every year.

The modern approach that most financial planners now recommend is a “bucket strategy”:

- Bucket 1 (Short-term): One to two years of living expenses in cash or very stable assets

- Bucket 2 (Medium-term): Income-generating investments designed to fund years three through ten

- Bucket 3 (Long-term): Growth-focused investments for year ten and beyond

Maintaining some equity exposure — typically 30 to 50% — through retirement is now standard guidance, not risky behavior.

Myth #8: “Medicare Will Cover All My Healthcare Costs”

The Myth

Once you hit 65, Medicare takes care of everything medical and you have no more healthcare worries.

The Truth

Medicare is valuable, but it has significant gaps that catch many retirees off guard — often at the worst possible moment.

Here is a clear breakdown of what Medicare actually covers:

| Coverage Area | Medicare Covers | Out-of-Pocket Reality |

|---|---|---|

| Hospital stays | Yes (Part A, after deductible) | $1,632 deductible per benefit period (2026) |

| Doctor visits | Yes (Part B, 80%) | You pay 20% with no cap |

| Prescription drugs | Partial (Part D) | Varies by plan and drug |

| Dental | No | 100% out-of-pocket |

| Vision | No | 100% out-of-pocket |

| Hearing aids | No | 100% out-of-pocket |

| Long-term care | No | Average $108,000/year |

Source: Medicare.gov and Genworth Cost of Care Survey, 2026.

The average Medicare beneficiary still pays $3,000 to $5,000 per year out of pocket even with coverage. And the largest uncovered expense — long-term care — is something most people never budget for. The average cost of a nursing home in 2026 runs approximately $108,000 per year. Medicare does not cover it.

Medigap (supplemental insurance) and Medicare Advantage plans exist to fill some of these gaps. Understanding your options before you turn 65 — not after — is essential.

Myth #9: “I Can Figure Out Taxes in Retirement Later”

The Myth

Taxes are simpler in retirement. You earn less, so there is less to worry about.

The Truth

Taxes in retirement can be surprisingly complicated — and surprisingly expensive — if you have not planned for them in advance.

Here is what many retirees do not realize until it is too late:

Traditional 401(k) and IRA withdrawals are taxed as ordinary income. Every dollar you pull out is a taxable event. If you have saved $800,000 in a traditional 401(k), you have $800,000 of pre-tax money sitting in an account — and the IRS will want its share every time you make a withdrawal.

Social Security benefits can be taxed. If your “combined income” exceeds certain thresholds, up to 85% of your Social Security benefit becomes taxable.

Required Minimum Distributions (RMDs) start at age 73. The IRS requires you to begin withdrawing from traditional retirement accounts whether you need the money or not. Large RMDs can push retirees into higher tax brackets and trigger Medicare IRMAA surcharges — extra premium costs that add hundreds of dollars per month.

The solution is tax diversification — having a mix of Roth accounts (tax-free withdrawals), traditional accounts (taxable withdrawals), and regular taxable accounts. This gives you flexibility to manage your tax bill in retirement.

Pro Tip: The years between retirement and age 73 — when RMDs begin — are often the lowest-tax years of a retiree’s life. This window is your opportunity to do strategic Roth conversions, harvest capital gains at the 0% rate, and restructure your income to minimize taxes for decades to come. Waiting until 73 to think about this is an expensive mistake.

Myth #10: “Retirement Planning Is Only for Rich People”

The Myth

Retirement planning is something wealthy people do with expensive financial advisors. Regular people just save what they can and hope for the best.

The Truth

This is perhaps the most damaging myth on this entire list — and it disproportionately hurts middle-income earners who would benefit most from a solid plan.

The truth is that a simple, powerful retirement strategy is available to anyone with a job:

- Build a small emergency fund so you are never forced to tap retirement accounts early

- Contribute enough to your employer’s 401(k) to capture the full match — that is an immediate 100% return on that portion of your money

- Open a Roth IRA — there is no minimum balance requirement to start, and the tax-free growth is one of the best deals in personal finance

That is it. No financial advisor required to get started.

Free tools from SSA.gov, IRS.gov, and investor.gov provide everything a beginner needs to calculate projected benefits, understand contribution limits, and model different retirement scenarios.

When you are ready for more personalized guidance, fee-only financial advisors — who charge by the hour rather than earn commissions on products they sell you — are accessible at virtually any income level. The National Association of Personal Financial Advisors (NAPFA) directory at napfa.org lists vetted fee-only advisors nationwide.

The difference between a good retirement and a financially stressful one is almost never income level. It is almost always whether someone had a plan.

The bottom line: Retirement planning is not a luxury for the wealthy — it is the tool that prevents the middle class from becoming the impoverished elderly.

FAQs About 10 Retirement Myths Debunked

What is the biggest retirement myth that costs people the most money?

Believing that Social Security will cover your needs is probably the single most expensive myth. The average benefit of around $1,907 per month is a supplement, not a salary. People who plan their retirement entirely around Social Security often face severe financial stress in their 70s and 80s when healthcare costs rise and savings run thin.

Is $500,000 enough to retire on?

It can be, depending on your lifestyle and other income sources. Using the 4% rule, $500,000 supports about $20,000 per year in portfolio withdrawals. Combined with even a modest Social Security benefit of $1,500 per month — which equals $18,000 per year — that is $38,000 annually. That is enough for a modest but comfortable retirement in many parts of the country, especially if your mortgage is paid off.

Do I really need a financial advisor to retire well?

Not necessarily, especially in the early stages. The fundamentals — maximize your employer match, open a Roth IRA, avoid withdrawing early, and stay invested — do not require professional advice. As you get closer to retirement, however, a fee-only advisor can add significant value on Social Security timing, tax strategy, and withdrawal sequencing.

Is it true that retirees spend less than they did while working?

Early in retirement, many retirees actually spend more. The “go-go years” often include travel, dining out, and active lifestyle expenses. Spending typically dips in the quieter middle years, then rises sharply again later due to healthcare. Planning for a retirement budget that is roughly equal to your pre-retirement budget is generally safer than assuming your expenses will shrink on their own.

Does working in retirement affect your Social Security benefit?

If you claim Social Security before your full retirement age and continue working, your benefits can be temporarily reduced if you earn above a certain threshold ($22,320 in 2026). However, those withheld benefits are not lost — they are added back to your monthly payment once you reach full retirement age. After full retirement age, you can earn any amount without any reduction in your benefit.

The Bottom Line

You came into this post carrying at least a few of these myths. Most people do. The retirement landscape is cluttered with outdated advice, oversimplified rules, and assumptions that feel safe but are actually costing people thousands of dollars and years of financial security.

Here are the three truths worth carrying with you:

Your retirement number is personal. Stop comparing yourself to arbitrary benchmarks. Calculate your actual expected expenses, factor in all your income sources, and build toward a number that reflects your real life.

Social Security is a floor, not a ceiling. It is a meaningful piece of your retirement income — but it was never designed to be the whole picture. Build above it.

“Later” is the most expensive word in retirement planning. Compounding rewards people who start. Every year of delay costs more than the year before it.

Now that you know what is myth and what is reality, the next step is building your personal plan. Start with our guide on how to set your retirement number, or take our Retirement Readiness Quiz to see exactly where you stand today.

The retirees who thrive are not the ones who got lucky. They are the ones who stopped believing the myths.

Disclaimer: The content on RetireWealthPath.com is for informational and educational purposes only and does not constitute financial, tax, or legal advice. We are not licensed financial advisors. The information provided may not apply to your specific situation. Always consult a qualified financial professional, tax advisor, or attorney before making any financial decisions. Retirement planning involves risk and individual results will vary.