How Working in Retirement Affects Your Social Security Benefits

What if you want to retire from your main career but still work part-time? Will Social Security penalize you? The answer is: it depends — and the difference between getting it right and getting it wrong can be thousands of dollars per year.

The line between “working” and “retired” has never been blurrier. Today, millions of Americans pursue consulting work, part-time jobs, freelance gigs, and encore careers right alongside their Social Security benefits.

And while that’s a beautiful thing, it comes with one important rule you need to understand: claiming Social Security while working before your Full Retirement Age (FRA) triggers something called the earnings test — a provision that can reduce your monthly benefits when your income exceeds a certain threshold.

Here’s the single most important thing to understand before we go any further: the money withheld by the earnings test is not lost. It comes back to you. That one fact — widely misunderstood — changes everything about how you should think about how work in retirement affects SS benefits.

This guide covers all three phases of the earnings test — before FRA, the year of FRA, and after FRA — with exact 2026 thresholds, named examples, and a clear decision framework so you know exactly where you stand.

Let’s start by understanding the three distinct phases of Social Security and work — because the rules are completely different depending on which phase you’re in.

The Three Phases of Working While Collecting Social Security

Before diving into any numbers, you need a mental map. The Social Security Administration doesn’t apply one uniform rule to working retirees — it applies three very different sets of rules depending on your age relative to your Full Retirement Age. Miss this framework and the details that follow will feel scattered. Understand it and everything else clicks into place.

The rules shift at two specific moments: the calendar year before you reach FRA, and the actual month your FRA birthday arrives. Your situation is determined entirely by where you fall relative to those two milestones.

Phase 1 — Before the Year You Reach FRA The strictest rules apply here. The earnings test uses the lowest threshold and the highest withholding rate. This phase governs every month you are both under FRA and receiving benefits.

Phase 2 — The Calendar Year You Reach FRA A transitional period with its own distinct rules. The earnings threshold increases significantly, the withholding rate drops, and the phase ends the moment your FRA birthday arrives.

Phase 3 — The Month You Reach FRA and Beyond The earnings test disappears entirely — for the rest of your life. You can earn any amount from any type of work without any reduction in your Social Security benefit.

Quick Reference:

- Phase 1 (below FRA): $22,320 threshold — $1 withheld per $2 over the limit

- Phase 2 (year of FRA): $59,520 threshold — $1 withheld per $3 over the limit

- Phase 3 (FRA and beyond): No earnings test — earn any amount, keep your full benefit

The earnings test is not a permanent tax on working retirees. It is a temporary adjustment that expires the moment you reach your Full Retirement Age. Everything changes at that birthday.

Phase 1 — The Earnings Test Before Your Full Retirement Age

This is the phase that creates the most confusion and the most costly financial mistakes. The rules are strict, the numbers matter, and there is one pervasive myth that causes real damage — which we’ll correct head-on. Let’s start with the mechanics.

The 2026 Earnings Test Threshold and Withholding Formula

In 2026, the annual earnings test exempt amount for those below FRA is $22,320 — or approximately $1,860 per month. This figure is adjusted annually for wage inflation and has grown steadily from $19,560 in 2023.

For every $2 you earn above that $22,320 threshold, $1 in Social Security benefits is withheld. But here is where most explanations stop short: the SSA does not trim a little from each monthly check. Instead, it withholds complete monthly benefit payments until the total calculated withholding amount is satisfied. That distinction matters in how you experience the earnings test.

Here’s how it plays out in practice:

Sandra, 63, claimed Social Security at 62 and receives $1,400/month ($16,800/year). She works part-time and earns $34,320 in 2026 — exactly $12,000 above the $22,320 threshold. The SSA withholds $1 for every $2 over the limit: $12,000 ÷ 2 = $6,000 to be withheld. Since her monthly benefit is $1,400, the SSA withholds approximately 4–5 complete monthly payments early in the year. Sandra receives no Social Security checks from January through April or May — then receives her full $1,400 every month for the rest of the year.

The calendar-year experience can feel jarring — no checks for several months, then full checks for the rest. That’s by design, not by error.

What Counts as “Earnings” for the Earnings Test

This is where many retirees are caught off guard. “Earnings” for the earnings test has a very specific legal definition — and it is much narrower than total income.

Counts as earnings:

- Wages from a W-2 job — salary, hourly pay, bonuses, commissions, and vacation pay

- Net profit from self-employment (Schedule C income after business expenses)

- Freelance and contractual income paid as wages or self-employment income

- Contributions to certain deferred compensation plans in the year they are deferred

Does NOT count as earnings:

- Investment income — dividends, capital gains, interest

- Rental income (unless you operate a formal business with active management)

- Pension payments and annuity income

- IRA and 401(k) withdrawals

- Social Security benefits themselves

- Unemployment compensation

- Workers’ compensation

The practical implication of this is enormous. A retiree living on $80,000 per year from IRA withdrawals, dividends, and rental income faces zero earnings test — because none of that qualifies as “earnings” under SSA rules. The earnings test applies exclusively to wages and self-employment profit.

This is especially important to understand if you’re exploring retirement planning strategies for building multiple income streams — the source of your income determines your earnings test exposure far more than its total amount.

How the SSA Actually Implements Withholding

At the start of each year, the SSA asks beneficiaries to estimate their expected annual earnings. Based on that estimate, the SSA calculates how many monthly benefit payments to withhold — and begins the withholding immediately in January.

If actual earnings come in lower than projected, the SSA reconciles the difference and returns any over-withheld amounts. If actual earnings exceed the estimate, additional benefit months may be withheld retroactively. The takeaway: notify the SSA promptly if your expected earnings change significantly during the year. This prevents both unwanted payment gaps and end-of-year repayment surprises.

Earnings Test Withholding Examples — 2026, Phase 1 (Monthly Benefit: $1,400)

| Annual Earnings | Amount Over Threshold | Benefits Withheld | Months of Full Checks |

|---|---|---|---|

| $22,320 or less | $0 | $0 | 12 months |

| $27,320 | $5,000 | $2,500 | ~10 months |

| $34,320 | $12,000 | $6,000 | ~8 months |

| $42,320 | $20,000 | $10,000 | ~5 months |

| $50,320 | $28,000 | $14,000 | ~2 months |

| $60,920 | $38,600 | $19,300 | $0 — all withheld |

Illustrative calculations using 2026 SSA earnings test threshold of $22,320 and $2-for-$1 withholding formula. For educational purposes only.

The Myth That Costs Retirees Thousands — “Withheld Benefits Are Lost Forever”

This is the most important section in this entire post. Read it twice.

The Myth: “If the SSA withholds my Social Security benefits because I’m working, that money is gone forever.”

The Reality: Withheld benefits are not lost. Not a single dollar. They are credited back to you at your Full Retirement Age through a permanent upward adjustment to your monthly benefit — for the rest of your life.

Here is exactly how the credit-back mechanism works. When you reach FRA, the SSA recalculates your monthly benefit to account for every month that was withheld due to the earnings test. For each complete month withheld, the SSA treats it as if you had claimed one month later — applying the same actuarial adjustment that would have applied had you actually delayed your claim. Your monthly benefit is permanently increased, starting the month you reach FRA.

Let’s follow Sandra from the earlier example through to her FRA:

Sandra claimed at 62 and received a 30% permanent reduction — her Primary Insurance Amount (PIA) of $2,000 was reduced to $1,400/month. During her pre-FRA years, the SSA withheld a total of 14 monthly payments due to the earnings test. At Sandra’s FRA of 67, the SSA recalculates. Those 14 withheld months are credited back. The SSA treats Sandra as if she claimed 14 months later than she actually did, reducing her early-claiming penalty proportionally. Her benefit increases from $1,400/month to approximately $1,527/month — a permanent increase that begins the month she reaches FRA.

Sandra does not receive a lump-sum repayment. But her higher monthly benefit will, over time, return every dollar that was withheld — typically within 2–3 years of reaching FRA. After that break-even point, she receives more per month for the rest of her life than she would have without the earnings test withholding.

Think of it this way: the earnings test is effectively an enforced delayed-claiming mechanism. It is not a penalty for working. It is an adjustment to reflect when you effectively started receiving benefits.

Tell every retired friend who fears the earnings test this one fact: the money withheld is not taken from you — it comes back as a higher monthly benefit starting at FRA. Understanding this transforms the earnings test from a financial threat into a largely neutral event for most working retirees.

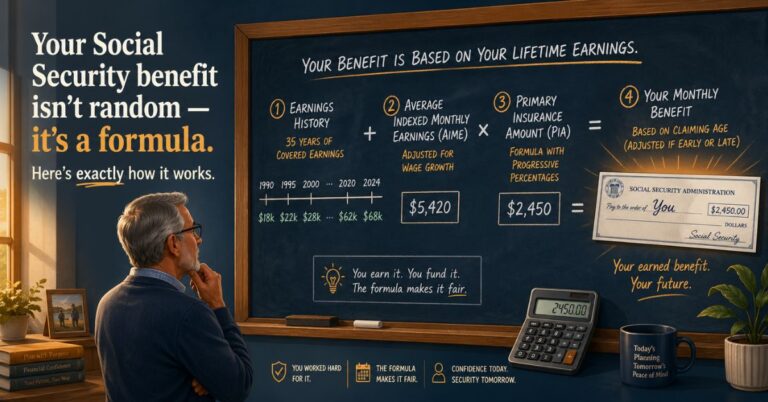

To fully understand why this recalculation works the way it does, it helps to understand how Social Security benefits are calculated — specifically how your PIA and AIME interact with your claiming age to determine your monthly payment.

Phase 2 — The Special Rules in the Year You Reach FRA

Most people know Phase 1 and Phase 3. Phase 2 — the transitional calendar year in which you reach FRA — is where significant money is left on the table due to a simple lack of awareness.

The Higher Threshold

In the calendar year you reach FRA, the earnings test threshold jumps dramatically to $59,520 in 2026 — approximately $4,960 per month. This threshold applies only to earnings accumulated in the months before your FRA birthday in that calendar year.

The Lower Withholding Rate

In the year of FRA, only $1 is withheld for every $3 earned above the threshold — compared to $1 per $2 in Phase 1. That reduction in the withholding rate, combined with the much higher threshold, dramatically reduces the financial impact of working in your FRA year.

The Monthly Rule Option

In the first year of retirement, the SSA offers a special “monthly earnings test” as an alternative to the annual test. Under this monthly rule, your benefit is only withheld in months where your earnings exceed one-twelfth of the annual threshold. This is particularly valuable for people who retire mid-year — they can receive full Social Security benefits for the months after retirement even if their total annual earnings (from the job they just left) exceed the annual threshold.

Here is what Phase 2 looks like in practice:

Thomas turns 67 — his FRA — in October 2026. He has been working full-time and earning $90,000 per year. He retires in October. His earnings through September total $75,000 — above the $59,520 Phase 2 threshold by $15,480. Withholding: $15,480 ÷ 3 = $5,160 in benefits withheld. Since Thomas’s monthly benefit is $2,200, approximately 2–3 monthly payments are withheld before his October birthday. Starting in October — the month Thomas reaches FRA — the earnings test disappears entirely. Thomas receives his full Social Security benefit every month from October through December with zero reduction, regardless of what he earns.

The critical planning insight here: if you are approaching FRA and your pre-FRA earnings in that calendar year will fall below $59,520, you may be able to claim Social Security with minimal or zero earnings test withholding. Many people who unnecessarily delay claiming because they fear the earnings test in their FRA year are leaving months of Social Security income uncollected for no reason.

Phase Comparison — 2026 Earnings Test Rules

| Feature | Phase 1 (Before FRA Year) | Phase 2 (Year of FRA) | Phase 3 (After FRA) |

|---|---|---|---|

| Annual threshold | $22,320 | $59,520 | No limit |

| Monthly threshold | $1,860 | $4,960 | No limit |

| Withholding rate | $1 per $2 over limit | $1 per $3 over limit | None |

| Applies to months | All months below FRA | Months before FRA birthday | Not applicable |

| Withheld amounts recovered? | Yes — at FRA | Yes — at FRA | N/A |

Source: Social Security Administration earnings test rules, 2026. Thresholds adjusted annually for wage inflation.

Phase 3 — After FRA, Work as Much as You Want

After FRA, the rules are beautifully simple: there are none.

The moment you reach your Full Retirement Age, the earnings test disappears permanently. You can earn $50,000, $150,000, or $500,000 from work — and receive every dollar of your Social Security benefit without any reduction. There is no form to file, no threshold to track, and no annual earnings reporting requirement.

The Bonus Benefit of Working After FRA

Here is something most retirees don’t expect: working after FRA can actually increase your Social Security benefit. If your current-year earnings are higher than one of the 35 years currently factored into your benefit calculation, the SSA automatically replaces the lower year with the higher one — and recalculates your monthly benefit upward. This recalculation happens each January, automatically, without any action on your part.

William claimed Social Security at 67 (FRA) and receives $2,300/month. He continues working as a consultant earning $95,000/year. His 35-year earnings average includes some early-career years where he earned approximately $25,000 (indexed). Each additional year of $95,000 in earnings replaces one of those $25,000 years in his calculation. After two years of post-FRA work, William’s monthly benefit increases to $2,380/month — a permanent $80/month increase from the improved earnings average. This recalculation happened automatically without William filing a single form.

This benefit matters most for people who claimed at or near FRA but continued working at a meaningful income level, and for anyone whose early career included significant low-earning years. This is also a valuable consideration if you’re assessing the best age to claim Social Security — because working past FRA isn’t just neutral, it can actively improve your lifetime benefit.

Common Mistake: Assuming that once you claim Social Security, your benefit is completely fixed. It is not. If you work after FRA at above-average earnings, check each January to see if your benefit has increased. The SSA processes the recalculation automatically, but verifying the update is your responsibility.

Self-Employment and the Earnings Test — Special Rules That Catch People Off Guard

If you’ve transitioned from traditional employment into consulting, freelancing, or running your own business, the earnings test has a few unique wrinkles that can catch you completely off guard.

How Self-Employment Income Is Counted

The earnings test counts net profit from self-employment — meaning revenue after legitimate business expenses are deducted. Net profit is reported on Schedule C and subject to self-employment tax. The SSA specifically uses your Net Earnings from Self-Employment (NESE), which is net profit × 0.9235 — the same figure used to calculate self-employment tax.

The Substantial Services Test

For self-employed retirees, the SSA applies an additional layer: the “substantial services” test. If you own a business but delegate all operations and personally provide fewer than 45 hours per month of service, the SSA may not count the business income as earned income for earnings test purposes — even if the business is profitable. This creates a meaningful planning opportunity for business owners who want to maintain ownership while reducing active involvement.

The Timing Trap

Self-employment income is reported annually on tax returns — not monthly like W-2 wages. A self-employed retiree who has a profitable year may receive a large benefits withholding notification from the SSA retroactively, after the year is already over. This can produce unexpected repayment demands or sudden benefit suspensions. Tracking net income monthly — not just at tax time — is essential.

Here is what this looks like:

Barbara, 64, retired from corporate life and started consulting part-time. She claimed Social Security at 63 and receives $1,600/month. In 2026, her consulting generates $48,000 in revenue. After deducting $12,000 in legitimate business expenses, her net profit is $36,000. Amount over the $22,320 threshold: $13,680. Withholding: $13,680 ÷ 2 = $6,840. The SSA withholds approximately 4 complete monthly benefit payments early in the year, with the remainder reconciled at year-end.

Planning strategies for self-employed retirees under FRA:

- Maximize legitimate business deductions to reduce net profit closer to or below the earnings test threshold

- Time large client payments to years when you will be past FRA — eliminating the earnings test entirely

- Consider restructuring business ownership to reduce “substantial services” if appropriate and legitimate

- Consult a CPA who understands the specific interaction between Schedule C income and SSA earnings test rules

Pro Tip: If you are a self-employed retiree under FRA, track your net self-employment income monthly. At the start of each year, the SSA bases withholding on the estimated annual earnings you report. If your business income runs ahead of that estimate, contact the SSA mid-year to update your projection — and avoid a large, unexpected year-end reconciliation.

The Strategic Decision — Should You Claim Early If You’re Still Working?

Everything in this post has been building toward this question — the one most working retirees are actually asking when they search for information on the earnings test.

When Claiming Early While Working Almost Never Makes Sense

If you are working full-time and earning significantly above the $22,320 threshold, most or all of your early Social Security benefit will be withheld. In that scenario, you accept a permanent early claiming reduction without the benefit of actually receiving the early income. That is the worst possible outcome — a lasting penalty without the cash flow upside that motivated the early claim in the first place.

If your earnings are high enough that all SS benefits would be withheld anyway, you are effectively just delaying your benefit with extra administrative complexity attached.

Simple rule: If your annual work earnings will consistently exceed $22,320 before FRA, think carefully before claiming Social Security early. The earnings test will withhold most or all of your benefit — and while that money comes back at FRA, you’ve locked in a permanent early-claiming reduction without the cash flow benefit that was the whole point.

When Claiming Early While Working Can Still Make Sense

Earnings just below the threshold: If your part-time work generates $18,000–$22,000 per year — at or below the $22,320 limit — you can collect your full (if reduced) early benefit with zero withholding while maintaining meaningful work income.

Mixed income types: If most of your income comes from investments, rental properties, pensions, or IRA withdrawals — none of which count toward the earnings test — you can claim early and receive full benefits regardless of total income level.

Health concerns: If you have legitimate health concerns that reduce your life expectancy, the early benefit may be worth claiming even with some earnings test withholding. The break-even math shifts significantly when longevity is uncertain. Our guide on the best age to claim Social Security walks through the break-even calculation in detail.

The year of FRA with moderate earnings: In the year you reach FRA, the threshold jumps to $59,520. If your pre-FRA earnings in that year will fall below that amount, claiming SS in that year may produce benefits with minimal or zero withholding.

Quick Decision Guide — Should You Claim SS While Working? (2026)

| Annual Work Earnings | Age | Recommendation | Primary Reason |

|---|---|---|---|

| Under $22,320 | Below FRA | Claiming possible — evaluate based on health and need | No earnings test withholding |

| $22,320–$40,000 | Below FRA | Caution — partial withholding likely | Weigh cash flow vs. permanent reduction |

| $40,000–$59,520 | Below FRA | Generally wait — most benefits withheld | Permanent reduction without full cash benefit |

| Above $59,520 | Below FRA | Wait until FRA — all benefits likely withheld | Claiming early has no cash flow benefit |

| Any amount | Year of FRA | Evaluate — higher threshold reduces impact | Less withholding; FRA ends test mid-year |

| Any amount | FRA or older | Claim whenever optimal — no earnings test | Full benefit regardless of earnings |

RetireWealthPath.com analysis based on 2026 SSA earnings test rules. For educational purposes only. Individual situations vary.

How Working in Retirement Affects Taxes on Social Security — The Hidden Layer

The earnings test is only half the story. Work income can also increase the taxation of your Social Security benefits in ways that many retirees don’t anticipate. Understanding both layers — withholding and taxation — gives you the complete picture.

The Combined Income Formula

Social Security benefits become taxable when your “combined income” exceeds certain IRS thresholds. Combined income is calculated as: Adjusted Gross Income + Non-taxable interest + 50% of Social Security benefits.

The thresholds work in two tiers:

- Single filers above $25,000 (or married filing jointly above $32,000): up to 50% of SS benefits become taxable

- Single filers above $34,000 (or married filing jointly above $44,000): up to 85% of SS benefits become taxable

Work earnings flow directly into your Adjusted Gross Income — which means they directly increase your combined income and can push you into higher SS taxation territory.

Raymond, 64, collects $1,800/month ($21,600/year) in Social Security and earns $30,000 from part-time work. His combined income: $30,000 + $10,800 (50% of SS) = $40,800. As a single filer, that figure sits above both the $25,000 and $34,000 thresholds — meaning up to 85% of his $21,600 in SS benefits ($18,360) is potentially taxable as ordinary income. Raymond’s CPA recommends contributing to a traditional IRA to reduce his AGI, bringing his combined income below the 85% taxation threshold.

The state tax layer adds another dimension: 13 states currently tax Social Security benefits to some degree at the state level, while states like Florida, Texas, Tennessee, and Nevada impose no state income tax at all.

Pro Tip: If you’re working in retirement and collecting Social Security, consider increasing contributions to a traditional 401(k) or IRA to reduce your AGI — which reduces combined income and potentially reduces or eliminates Social Security taxation. This strategy is especially powerful for workers with access to an employer retirement plan, where contributions directly reduce W-2 wages reported to the IRS.

Practical Steps for Working Retirees — Managing the Earnings Test Without Stress

Here is everything in this post distilled into a clear, actionable management process.

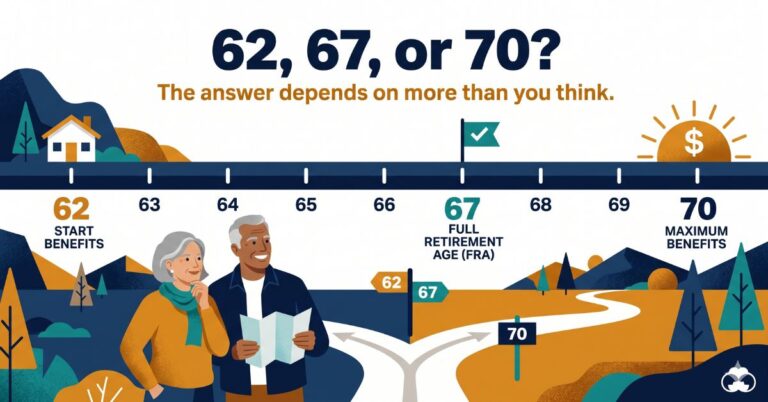

Step 1 — Know your FRA date precisely. Your FRA is determined by your birth year, not your retirement date or claiming date. For anyone born in 1960 or later, FRA is 67. Know the exact month and year — because that is the date when everything changes.

Step 2 — Estimate your annual work earnings before claiming. Before claiming Social Security any earlier than FRA, project your expected annual work earnings and compare to the $22,320 Phase 1 threshold. If earnings will consistently exceed the threshold, reconsider whether early claiming makes sense for your situation.

Step 3 — Report expected earnings to the SSA accurately. When you claim, the SSA will ask for your expected annual earnings. Report accurately — overestimating leads to unnecessary withholding and delayed refunds; underestimating leads to repayment demands.

Step 4 — Update the SSA if your earnings change significantly. If your work situation changes mid-year — a raise, reduced hours, or new freelance income — contact the SSA to update your earnings estimate. This prevents both overpayment and underpayment complications.

Step 5 — Track your withheld months. Keep a running record of how many monthly benefit payments have been withheld due to the earnings test. At FRA, verify with the SSA that your benefit has been adjusted upward to credit back those withheld months — and confirm the adjustment is correct.

Step 6 — Check for the post-FRA benefit recalculation every January. After FRA, if you continue working, check your benefit statement each January. The SSA will have automatically increased your benefit if your prior year’s earnings replaced a lower-earning year in your 35-year average.

Step 7 — Model the tax impact separately. The earnings test and the Social Security taxation calculation are two different systems. Run both calculations annually to understand your total net SS income after withholding and taxation — and explore IRA contribution strategies to reduce AGI where SS taxation is significant.

Frequently Asked Questions

If the SSA withholds my Social Security due to the earnings test, do I get that money back?

Yes — every dollar withheld due to the earnings test is credited back to you at Full Retirement Age through a permanent upward adjustment to your monthly benefit. The SSA treats each withheld month as if you claimed one month later, which reduces your early-claiming penalty proportionally. You don’t receive a lump-sum repayment, but your higher monthly benefit starting at FRA will return all withheld amounts — typically within 2–3 years of reaching FRA.

I’m 65 and my only income is IRA withdrawals and rental property income. Does the earnings test apply to me?

No. The earnings test applies only to wages from employment and net profit from self-employment. IRA withdrawals, rental income (unless you operate it as a formal business), investment income, dividends, and capital gains do not count toward the earnings test threshold. You can withdraw any amount from your IRA and collect any amount in rental income while receiving your full Social Security benefit before FRA, with zero earnings test reduction.

What if I claim Social Security, the earnings test withholds all my benefits, and then I decide to stop working?

The SSA will restore your full monthly benefit immediately once your earnings drop below the threshold. Contact the SSA to notify them of your change in work status and request benefit reinstatement. Any months withheld will still be credited back at FRA through the benefit recalculation. Additionally, if you claimed less than 12 months ago, you may be eligible to withdraw your entire Social Security application (Form SSA-521), repay all benefits received, and restart fresh at a later age.

Can I deliberately reduce my hours to stay under the earnings test threshold and collect Social Security?

Absolutely — this is one of the most common and effective strategies for working retirees. If you can manage your work hours to keep annual earnings at or below $22,320 (Phase 1) or $59,520 (year of FRA), you collect your full Social Security benefit without any withholding. Many retirees in phased retirement deliberately structure consulting hours, part-time work, or seasonal employment around the earnings test threshold — allowing them to collect SS income alongside meaningful work income simultaneously.

Does working after FRA affect my Social Security benefit in any way?

Yes — positively. After FRA, there is no earnings test, so work income cannot reduce your benefit. However, if you continue working and your current-year earnings are higher than one of your 35 lowest indexed earning years, the SSA automatically recalculates your benefit each January and increases it accordingly. This recalculation is automatic and permanent — you don’t need to request it. The increase is typically modest but real, and it applies to every future monthly payment for the rest of your life.

The Bottom Line

Working in retirement does not have to mean sacrificing Social Security — it means understanding the rules well enough to do both on your own terms.

Here are the three facts worth remembering from everything covered in this guide:

First, the earnings test withholds benefits temporarily — it does not permanently reduce them. Every dollar withheld comes back at FRA as a permanently higher monthly benefit.

Second, the earnings test applies only to wages and self-employment income — not to investment income, IRA withdrawals, rental income, or pension payments. Your total income doesn’t determine your exposure; the source of that income does.

Third, after FRA, the earnings test disappears entirely. You can earn any amount from any source and receive your full Social Security benefit without restriction — and continued work can actually increase your monthly benefit over time.

Now that you understand how work affects your Social Security, the next logical question is timing. Read our complete guide to the best age to claim Social Security for a full strategy walkthrough on maximizing lifetime income — or explore our Social Security for married couples strategy if you want to coordinate your claiming decision with your spouse’s.

Work in retirement doesn’t have to mean sacrificing Social Security — it means understanding the rules well enough to do both on your own terms.

Disclaimer: The content on RetireWealthPath.com is for informational and educational purposes only and does not constitute financial, tax, or legal advice. We are not licensed financial advisors. The Social Security earnings test thresholds, withholding formulas, taxation rules, and benefit recalculation provisions referenced in this article reflect 2026 SSA guidelines and are subject to change by legislation or SSA policy. All calculations and named examples — including Sandra, Thomas, Barbara, William, and Raymond — are for illustrative and educational purposes only and do not represent guaranteed outcomes. Individual benefits, withholding amounts, and tax situations vary significantly based on personal earnings, claiming age, filing status, and other factors. Always consult a qualified financial professional, tax advisor, or Social Security specialist before making claiming or work decisions in retirement.