Retirement Readiness Quiz [Are You Actually Ready to Retire?]

If your boss walked in tomorrow and said, “your last day is in 90 days” — would you be okay? Or would your stomach drop?

Most people have a general sense they’re either “on track” or “behind” for retirement. But almost nobody has actually measured it. And here’s the thing most financial content gets wrong: retirement readiness is not a single savings number. You can have $2 million saved and still not be ready — if you haven’t planned for taxes, healthcare, or how you’ll actually turn that money into monthly income.

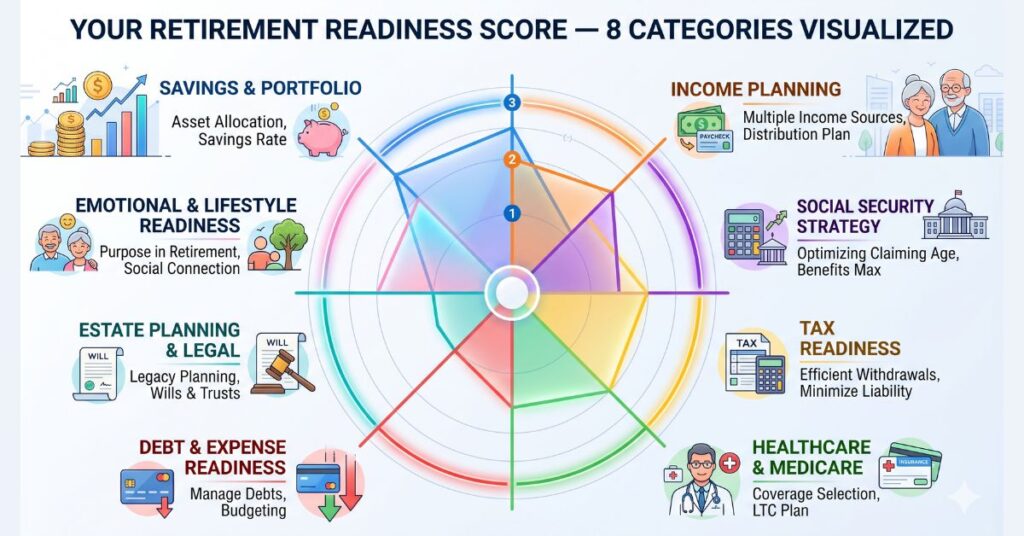

By the end of this guide, you’ll have a concrete readiness score across 8 categories, a clear picture of your strongest and weakest areas, and specific next steps based on where you land. This quiz is also designed to be taken more than once — it’s a living diagnostic tool worth revisiting every 1–2 years as your plan evolves.

Score yourself honestly in each section. No one is grading you — and the only wrong answer is the one you’re not honest about.

How This Quiz Works — Your Scoring System

Before you dive in, here’s the framework. Each of the 8 categories below is scored on a 0–3 point scale:

- 0 — Not started / No plan in place

- 1 — Early stages / Partially addressed

- 2 — Good progress / Mostly addressed

- 3 — Fully addressed / Confident and complete

The 8 categories covered in this quiz:

- Savings & Portfolio Readiness

- Income Planning

- Social Security Strategy

- Tax Readiness

- Healthcare & Medicare Planning

- Debt & Expense Readiness

- Estate Planning & Legal Documents

- Emotional & Lifestyle Readiness

Maximum possible score: 24 points.

Your result tier (scored at the end):

- 0–8: Early Stage — significant groundwork still needed

- 9–14: Building Momentum — real progress with key gaps to address

- 15–19: Nearly Ready — strong foundation with important finishing touches

- 20–24: Retirement Ready — comprehensive plan in place

Print this page or open a notes app before you begin. Write down your score for each category as you go — you’ll need the total at the end. And be honest: a score that flatters you today won’t protect you in 20 years.

Category 1 — Savings & Portfolio Readiness (0–3 points)

This is the category most people expect — but the right frame isn’t just your account balance. It’s whether your savings are sufficient and sustainable for the retirement you’re planning.

Score yourself:

- Score 0 — I have less than 1 year of living expenses saved in retirement accounts and no clear savings target.

- Score 1 — I have some retirement savings but less than 10× my annual expenses. I know I’m behind but haven’t calculated my specific gap.

- Score 2 — I have between 10× and 20× my annual expenses saved, or I’m on a clear trajectory to reach my retirement number by my target date.

- Score 3 — I have saved 20× or more of my planned annual retirement expenses (or my portfolio plus guaranteed income fully covers my retirement budget). I know my withdrawal rate and have stress-tested my plan.

Why “20× annual expenses” instead of a round number like “$1 million”? Because a benchmark that doesn’t reflect your actual lifestyle is meaningless. A person spending $40,000/year needs far less than one spending $120,000/year — and both need a different target than a blanket $1M suggests.

Note: trajectory matters as much as current balance. A 50-year-old with $300,000 and maxing contributions is on a different path than one with $300,000 and contributing nothing. Also, this score should reflect liquid retirement assets only — not home equity, business value, or expected inheritance.

| Age | Savings Target (multiple of annual salary) | Example: $70,000 salary |

|---|---|---|

| 30 | 1× | $70,000 |

| 40 | 3× | $210,000 |

| 50 | 6× | $420,000 |

| 55 | 7× | $490,000 |

| 60 | 8× | $560,000 |

| 67 (retirement) | 10× | $700,000 |

📝 My Category 1 Score: ___ / 3

Category 2 — Income Planning (0–3 points)

Having savings is one thing. Having a reliable plan that turns those savings into a monthly paycheck is another. This is often the piece people have thought about least — and it matters enormously.

Score yourself:

- Score 0 — I have no idea how I will generate monthly income in retirement. I plan to “figure it out when I get there.”

- Score 1 — I know my main income sources (Social Security, 401k withdrawals) but have no specific withdrawal strategy or income sequencing plan.

- Score 2 — I’ve mapped my income sources, estimated monthly retirement income, and have a general withdrawal order in mind (taxable → tax-deferred → Roth).

- Score 3 — I have a comprehensive income plan: specific monthly income from each source, a written withdrawal strategy, a contingency for market downturns (cash buffer or bucket strategy), and I know my income will cover expenses in year 1 of retirement.

Income planning isn’t “I have a 401k.” It’s knowing the specific monthly dollar amount coming from each source and in what order you’ll tap them. A withdrawal rate without a sequence plan is incomplete — the order of withdrawals has massive tax implications. (See our guide to the 3-bucket retirement income strategy for the most approachable framework for structuring this.)

⚠️ Common Mistake: Planning to withdraw “whatever I need each month” from your 401k without a strategy is one of the most expensive approaches possible. Without a withdrawal sequence plan, you may inadvertently push yourself into higher tax brackets, trigger Medicare IRMAA surcharges, or deplete taxable accounts before Roth accounts — costing tens of thousands in unnecessary taxes.

📝 My Category 2 Score: ___ / 3

Category 3 — Social Security Strategy (0–3 points)

Social Security is the single largest financial decision most retirees will make — and it’s irreversible once claimed. Yet most people spend less time on this decision than they spend choosing a car.

Score yourself:

- Score 0 — I haven’t checked my Social Security statement. I plan to claim “when I retire” without thinking about timing.

- Score 1 — I’ve checked my SSA.gov account and know my approximate benefit. I understand that claiming age affects the amount but haven’t modeled scenarios.

- Score 2 — I know my Full Retirement Age, my benefit at 62 vs. FRA vs. 70, and have a general sense of my optimal claiming strategy based on my health and financial situation.

- Score 3 — I have a documented Social Security strategy: I know the exact monthly benefit at each claiming age, I’ve modeled the break-even analysis, I’ve considered spousal/survivor benefit coordination if married, and I’ve decided on my claiming age and why.

The difference between claiming at 62 vs. 70 for an average earner can exceed $200,000 in lifetime benefits. Unlike most financial decisions, Social Security claiming cannot be undone after the 12-month “do-over” window. For married couples, it’s even more complex — the higher earner’s claiming decision affects the surviving spouse’s benefit for potentially decades.

One note on the “Social Security won’t be there” concern: even if trust funds are depleted by 2033, the program is projected to pay approximately 77% of scheduled benefits — not zero. Don’t let uncertainty about the future become a reason to claim early without running the numbers. If you haven’t yet, create a free SSA.gov account today and check your projected benefit.

📝 My Category 3 Score: ___ / 3

Category 4 — Tax Readiness (0–3 points)

Taxes in retirement are the category that surprises people the most — and cost the most. People who score low here are often sitting on large pre-tax accounts with no plan for the tax bill waiting at RMD age.

Score yourself:

- Score 0 — All (or nearly all) of my retirement savings are in traditional pre-tax accounts (401k, traditional IRA). I’ve given no thought to tax diversification or retirement tax strategy.

- Score 1 — I understand that retirement withdrawals will be taxed but haven’t done specific tax planning. I have some Roth savings but no conversion strategy.

- Score 2 — I have tax-diversified savings across pre-tax and Roth accounts. I understand how Social Security taxation works and know roughly what tax bracket I’ll be in during retirement.

- Score 3 — I have a written tax strategy: I know my pre-RMD planning window, have a Roth conversion plan (if applicable), understand IRMAA thresholds, know my optimal withdrawal order, and have modeled my RMD amounts starting at age 73.

The Pre-Tax Time Bomb

Many people have spent decades building large traditional 401k/IRA balances — which is excellent for accumulation. The problem: every dollar withdrawn is taxed as ordinary income, and at age 73, Required Minimum Distributions force withdrawals whether you need the money or not. A $1.5M traditional IRA generates roughly $58,000 in year-one RMDs — which, combined with Social Security, can push a retiree into a surprisingly high tax bracket.

The solution: strategic Roth conversions in the years between retirement and age 73 — the “sweet spot” tax window when your income is often at its lowest.

Tax Diversification in Plain English

- Pre-tax bucket (traditional 401k/IRA) — taxed on withdrawal

- After-tax bucket (Roth) — never taxed again

- Taxable bucket (brokerage) — taxed on dividends and capital gains, often at lower rates

Having all three gives you flexibility to manage your taxable income year by year in retirement. It’s one of the most powerful — and most overlooked — tools retirees have.

💡 Pro Tip: If you’re retired and under 73, every year you’re not doing at least some Roth conversions is a potential missed opportunity. The window between retirement and RMD age is often the lowest-tax period of your adult life — use it intentionally.

📝 My Category 4 Score: ___ / 3

Category 5 — Healthcare & Medicare Planning (0–3 points)

Healthcare is the most emotionally charged and financially underestimated category in retirement planning. It’s where many people feel most vulnerable — and least prepared.

Score yourself:

- Score 0 — I haven’t thought about healthcare in retirement beyond “Medicare will cover it.” I don’t know when I’m eligible or what it covers.

- Score 1 — I know Medicare starts at 65 and understand the basic parts (A, B, D). I haven’t chosen a supplemental plan or estimated out-of-pocket costs.

- Score 2 — I’ve researched Medicare options (original Medicare vs. Medicare Advantage, Medigap plans), estimated annual healthcare costs, and have a general plan for healthcare if retiring before 65.

- Score 3 — I have a complete healthcare plan: I know my Medicare enrollment date and have a plan for the 7-month enrollment window; I’ve chosen between original Medicare + Medigap vs. Medicare Advantage; I’ve budgeted for dental, vision, hearing, and long-term care; I have an HSA strategy; and I’ve estimated my lifetime healthcare costs.

A few critical points on healthcare that most people discover too late:

- The gap risk: Retiring before 65 means a healthcare coverage gap. COBRA, ACA marketplace, health-sharing, or spousal coverage are your options — each with trade-offs.

- Long-term care: Medicare covers very little long-term care. The average nursing home cost in 2026 exceeds $108,000/year. Medicaid requires spending down almost all assets first.

- The Medicare enrollment trap: Missing the initial enrollment window (7 months around your 65th birthday) results in permanent premium penalties.

- HSA accounts: One of the most underused retirement healthcare tools. Funds contributed before Medicare enrollment can be invested and grow tax-free for future medical expenses.

For official Medicare enrollment guidance, visit medicare.gov.

📝 My Category 5 Score: ___ / 3

Category 6 — Debt & Expense Readiness (0–3 points)

Carrying debt into retirement is one of the most underrated retirement risks. This is also a category where many readers feel most in control — and often rightfully so. Give yourself credit for what you’ve built, while being honest about what’s still needed.

Score yourself:

- Score 0 — I carry significant high-interest debt (credit cards, personal loans) and/or a large mortgage balance that will extend well into retirement. I have no plan to eliminate it before I stop working.

- Score 1 — I have some debt but am actively paying it down. I expect to carry a mortgage or some obligations into the early years of retirement.

- Score 2 — I am debt-free or close to it (mortgage only, within 5 years of payoff). My planned retirement expenses are realistic and I’ve built a retirement budget.

- Score 3 — I am completely debt-free (including mortgage) or have a concrete payoff plan aligned with my retirement date. I have a written, realistic retirement budget tested against my income plan, and a 12-month emergency fund in liquid savings outside retirement accounts.

A few things worth knowing in this category: The conventional 3–6 month emergency fund rule needs to expand in retirement. Most planners recommend 1–2 years of expenses in cash or cash equivalents to buffer against sequence-of-returns risk — the risk that a market downturn in your first years of retirement permanently damages your portfolio.

Also worth noting: many retirees underestimate the “go-go years” spending spike (roughly ages 60–75), when travel, dining, and leisure often increase before the health-related slowdown of later years. Budget accordingly.

⚠️ Common Mistake: Retiring with credit card debt is one of the most expensive decisions possible. A $15,000 credit card balance at 22% interest costs over $3,300/year — which at a 4% withdrawal rate requires an extra $82,500 in retirement savings just to service. Pay off high-interest debt before retirement, not after.

📝 My Category 6 Score: ___ / 3

Category 7 — Estate Planning & Legal Documents (0–3 points)

Estate planning is the most avoided category in retirement readiness. Most people associate it with death and put it off indefinitely. Try reframing it this way: it’s not about you dying — it’s about protecting the people you love from chaos.

Score yourself:

- Score 0 — I have no will, no power of attorney, no healthcare directive, and no beneficiary designations reviewed in the past 5 years. My family would have to figure everything out in a crisis.

- Score 1 — I have a basic will but it is outdated (more than 5 years old or drafted before major life changes). I may have a power of attorney but am unsure if it is durable. Beneficiary designations haven’t been reviewed recently.

- Score 2 — I have a current will, a durable power of attorney, and a healthcare directive. My beneficiary designations are up to date on all accounts. I’ve communicated my basic wishes to my family.

- Score 3 — I have a comprehensive estate plan: current will or living trust, durable POA for finances, healthcare POA and living will, up-to-date beneficiary designations on all accounts, a documented plan for digital assets, and a family meeting has been held or scheduled to discuss the plan with loved ones.

The most important estate planning fact most people don’t know: retirement accounts and life insurance pass directly to named beneficiaries — they bypass the will entirely. An outdated beneficiary designation is a legal document that can override years of careful estate planning. The ex-spouse listed on a 401k from 2009 will inherit that account, regardless of what your will says.

Also on the list of genuinely underplanned areas: digital estate planning. Cryptocurrency, online accounts, subscription services, social media — these are complex to handle without guidance. A simple “digital asset inventory” document stored securely is a starting point. See our guide to how to create a simple estate plan for a step-by-step walkthrough.

💡 Pro Tip: Set a recurring calendar reminder every January 1st: “Review beneficiary designations.” This 30-minute annual task is the single most high-value estate planning action you can take — and it costs nothing.

📝 My Category 7 Score: ___ / 3

Category 8 — Emotional & Lifestyle Readiness (0–3 points)

This is the category nobody talks about — and the one that blindsides the most retirees. Financial readiness without emotional readiness leads to what researchers call the “retirement identity crisis.” You can have a perfect portfolio and a broken routine. This category deserves the same attention as your 401k balance.

Score yourself:

- Score 0 — I’ve given almost no thought to what I’ll do in retirement beyond “not work.” I define myself largely through my career and haven’t imagined my day-to-day retired life in detail.

- Score 1 — I have some ideas about hobbies, travel, or family time but no real structure or plan. I feel uncertain about the transition and sometimes wonder if I’ll feel purposeful or fulfilled.

- Score 2 — I have a clear picture of how I want to spend my retirement years — hobbies, social connections, purpose activities, and routines. I’ve discussed plans with my spouse or partner and we’re largely aligned.

- Score 3 — I have a written “retirement life plan”: I know my daily structure, have social connections outside work that will sustain me, have a sense of purpose that doesn’t depend on my job title, have addressed my partner’s retirement vision, and have thought through where I want to live and how that may change with age.

The Identity Question Nobody Asks Until It’s Too Late

Research from the American Psychological Association lists retirement as one of the top 10 most stressful life transitions — on par with divorce and relocation. The “who am I without my job?” question hits hardest the people who were most successful in their careers, because identity and career became deeply intertwined.

Two common early retirement experiences: the honeymoon phase (first 6–12 months feel like extended vacation), followed by the disenchantment phase (lack of structure and purpose becomes distressing). The solution is to build the retirement life before leaving work — not after.

The Couples Alignment Problem

Many couples retire with completely different visions of what retirement looks like — one wants to travel constantly, the other wants to stay close to grandchildren; one wants to downsize immediately, the other is attached to the family home. These misalignments, unaddressed, create significant marital stress in retirement. Recommendation: have at least three dedicated “retirement vision” conversations with your partner before your last day of work — covering daily life, location, social activity, finances, and roles around the home.

⚠️ Common Mistake: Planning a financial retirement without planning a life retirement. The happiest retirees don’t just leave something — they retire to something: a community, a passion, a purpose, a place. Start building that now, not on your last day.

📝 My Category 8 Score: ___ / 3

Your Results — What Your Score Means

Add up your scores from all 8 categories. Maximum possible: 24 points.

📝 My Total Score: ___ / 24

Score 0–8 — Early Stage

You’re in the early stages of retirement planning, and there are significant areas that need attention before retirement becomes a safe option. This is not cause for panic — it’s cause for immediate, focused action.

The good news: Early-stage scores are the most responsive to action. Every category you address meaningfully shifts your financial future.

Priority actions:

- Calculate your retirement number this week (see our guide: How to Set Your Retirement Number)

- Open or maximize a Roth IRA or 401(k) contribution immediately

- Create a free SSA.gov account and check your projected benefit

- Schedule a consultation with a fee-only financial advisor within 30 days

- Return to this quiz in 6 months and measure your progress

Score 9–14 — Building Momentum

You’ve made real progress in some key areas — likely savings and possibly Social Security awareness. But significant gaps remain, typically in tax planning, healthcare, and estate planning.

The good news: You have a foundation. The work ahead is about filling specific gaps, not starting from scratch.

Priority actions:

- Identify your lowest 2–3 scoring categories and tackle one per quarter

- If tax readiness is low: open a Roth IRA and research Roth conversion opportunities

- If healthcare is low: spend 30 minutes on Medicare.gov to understand your options

- If estate planning is low: start with a will and beneficiary designation review — both can be done in a single afternoon

Score 15–19 — Nearly Ready

You have a strong, well-rounded retirement plan with most major areas addressed. You’re likely 2–5 years from retirement or have been planning seriously for some time.

The good news: You’re in a stronger position than the vast majority of Americans your age. The remaining work is optimization, not gap-filling.

Priority actions:

- Work with a fee-only advisor to stress-test your income plan against sequence-of-returns scenarios

- Finalize your Social Security claiming strategy if you haven’t

- Complete any missing estate documents and schedule the family conversation

- Do a “practice retirement” — live on your planned budget for 90 days to validate it’s realistic

Score 20–24 — Retirement Ready

You have a comprehensive, well-thought-out retirement plan across all eight dimensions. You’ve addressed not just the financial mechanics but the lifestyle, tax, healthcare, and estate components that most people overlook entirely.

The good news: You’re in the top tier of retirement preparedness. The work now is maintenance, monitoring, and enjoying what you’ve built.

Priority actions:

- Schedule an annual plan review — not just a portfolio review, but all 8 categories

- Consider a final stress-test with a fee-only advisor before your retirement date

- Share this quiz with a friend or family member who might benefit from the wake-up call

- Start building your “retirement life plan” if you haven’t — the financial plan is complete; now build the life

How to Use This Quiz Going Forward

This quiz is most valuable not as a one-time verdict but as a recurring prioritization tool. Retake it every 12–18 months, or immediately after any major life event: a job change, marriage, divorce, health diagnosis, inheritance, or housing decision. Major events shift multiple categories simultaneously — your plan needs to reflect the new reality.

If you have a spouse or partner, try this: each of you scores yourselves independently, then compare and discuss differences. Gaps in scores often reveal gaps in planning conversations — and that conversation alone is worth the exercise.

Remember: your lowest-scoring category is your highest-priority action. The quiz doesn’t define you — it directs you.

📥 Want the Printable Version?

Subscribe to the RetireWealthPath newsletter and we’ll send you a free printable PDF of this quiz — complete with a score tracking sheet you can use year after year. It’s the easiest way to make this a habit instead of a one-time read.

Frequently Asked Questions

How accurate is this retirement readiness quiz?

This quiz is a self-assessment diagnostic tool, not a professional financial evaluation. It gives you a structured way to identify gaps across the eight most critical dimensions of retirement readiness — the same dimensions a formal financial plan would address. For a personalized professional assessment, a fee-only financial advisor can run detailed projections based on your specific numbers, tax situation, and goals.

I scored low — does that mean I can’t retire on schedule?

Not necessarily. A low score identifies areas that need work, not a verdict on your retirement date. Many people who score in the Early Stage or Building Momentum range can significantly improve their readiness within 12–24 months of focused action. The most important step is identifying which specific categories are dragging your score and addressing them one at a time.

My spouse and I scored very differently. Is that a problem?

It’s extremely common — and actually valuable information. Couples frequently have asymmetric financial knowledge and planning engagement. Use the gap as a conversation starter rather than a source of conflict. The lower-scoring partner’s weak areas often reveal blind spots for the whole household.

How often should I retake this quiz?

Once per year as a minimum — ideally in January when goal-setting is natural. Also retake it immediately after any major life change: a job transition, divorce, inheritance, significant health diagnosis, or housing decision. Major events shift multiple categories at once.

What’s the most important category if I can only focus on one?

If you scored 0 or 1 on savings and portfolio readiness, start there — it’s the foundation everything else rests on. If your savings score is already a 2 or 3, the highest-leverage next category for most people is tax readiness, because tax planning mistakes are irreversible and compounding. The window for Roth conversions closes permanently once RMDs begin at age 73.

The Bottom Line

So — if your boss walked in tomorrow and gave you 90 days’ notice, how would you score now?

Retirement readiness is not a single number. It’s a multidimensional picture across savings, income, Social Security, taxes, healthcare, debt, estate planning, and lifestyle — and you now have a clear snapshot of where you stand across all eight. Most people never measure their readiness at all. The fact that you finished this guide already puts you ahead of the majority.

Your lowest-scoring category is your highest priority. Start there — explore our Retirement Planning Vocabulary Guide if you need to build foundational knowledge first, or jump straight to How to Set Your Retirement Number to tackle Category 1 right now.

Retirement readiness isn’t built in a day — but it is measured in one. You just measured yours.

Disclaimer: The content on RetireWealthPath.com is for informational and educational purposes only and does not constitute financial, tax, or legal advice. We are not licensed financial advisors. The retirement readiness quiz in this article is a self-assessment tool designed for general educational purposes only — it is not a substitute for a personalized professional financial evaluation. Scores and recommendations are general in nature and may not reflect your individual circumstances. Always consult a qualified financial professional, tax advisor, or attorney before making retirement planning decisions. Retirement planning involves risk and individual results will vary.