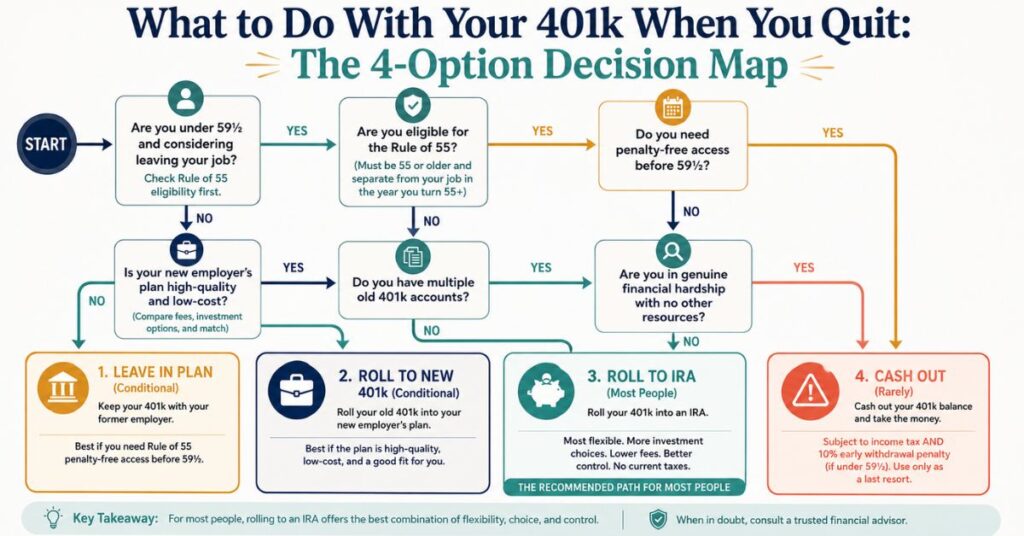

What to Do With Your 401k When You Quit: 4 Options Explained

When you leave a job, most people spend more time thinking about their exit interview than their 401k. That’s a $50,000 mistake waiting to happen.

The decision you make about your old employer’s 401k in the weeks after you quit will affect your retirement wealth for decades — and one of the four options available to you is so costly it should almost never be chosen. Yet it’s the option thousands of people default to every year, simply because no one told them the others existed.

The average American changes jobs 12 times in their career. Each transition is a 401k decision point. The accumulated impact of handling each one correctly — or incorrectly — is enormous. If you’re already behind on retirement savings, making the wrong call here only widens the gap.

There’s also a time dimension most people miss entirely. Some employers require you to make a rollover decision within 60 days of departure. Others allow you to leave the account indefinitely. Knowing which applies to you matters — and so does knowing what to do before your very last day of work.

This guide covers all four options for what to do with your 401k when you quit — with honest assessments of each, step-by-step rollover instructions, and a clear recommended path based on your specific situation. Whether you have a new job lined up, you’re heading into self-employment, or you’re approaching early retirement, the right answer is here.

Let’s map all four options — starting with the one most people choose by default, which is also the one with the most hidden risks.

Understanding Your Four Options — The Complete Map

Before evaluating any option, you need the complete lay of the land. The single most expensive mistake in 401k transitions is acting on the first option you encounter without knowing all the alternatives exist. Here are all four, named clearly.

Option 1 — Leave the money in your former employer’s 401k plan. Keep the account exactly where it is — no action required, no immediate decision needed. The money continues to grow in the plan’s investment options. Most plans allow this, though some require action if your balance falls below a minimum threshold.

Option 2 — Roll over to your new employer’s 401k plan. Move the money directly from your old plan to your new employer’s 401k — maintaining tax-advantaged status and consolidating your retirement accounts in one place.

Option 3 — Roll over to an Individual Retirement Account (IRA). Move the money to a self-directed IRA at a brokerage of your choice — Fidelity, Vanguard, or Schwab — maintaining tax-advantaged status while gaining full investment flexibility and control.

Option 4 — Cash it out. Withdraw the money and receive a check for the balance minus mandatory withholding. This triggers immediate income taxes plus a 10% early withdrawal penalty if you’re under 59½. Almost always the worst option.

The default trap: Many departing employees do nothing — which often defaults to Option 1. Doing nothing is sometimes fine, but it should be a deliberate choice, not an accidental one. Former employers who cannot locate you after years of inactivity can transfer your 401k balance to your state’s unclaimed property fund, where it can take significant effort to recover.

Four 401k Options at a Glance

| Option | Tax Impact | Penalty Risk | Investment Control | Ideal For |

|---|---|---|---|---|

| Leave with former employer | None — tax-deferred continues | None | Limited to plan options | Large balance, excellent plan, Rule of 55 eligible |

| Roll to new employer 401k | None — tax-deferred continues | None | Limited to new plan options | Simplicity, Rule of 55, loan access |

| Roll to IRA | None — tax-deferred continues | None | Full investment freedom | Most situations — maximum flexibility |

| Cash out | Full income tax due | 10% penalty if under 59½ | N/A — money leaves retirement | Almost never — genuine emergency only |

Source: IRS Publication 575 and 401k plan rules. Individual plan provisions vary.

Three of the four options preserve your retirement wealth intact. One destroys a significant portion of it immediately. The real decision is choosing wisely among the three that make financial sense — and the right choice depends entirely on your specific situation.

Option 1 — Leave the Money With Your Former Employer

Leaving the money in place is the path of least resistance — and sometimes the correct choice. But it comes with real risks and limitations that most people never consider.

When leaving the money in place is allowed:

Most plans allow former employees to maintain their account indefinitely if the balance exceeds $5,000. For balances between $1,000 and $5,000, the employer may automatically roll the account into an IRA at a default provider — you may not have a choice. For balances below $1,000, the employer may automatically cash out the account, withholding 20% for taxes and potentially triggering a penalty. Verify your balance against these thresholds the moment you decide to leave.

The legitimate reasons to leave the money in place:

Reason 1 — The Rule of 55. This is one of the most powerful and least-known exceptions to the 10% early withdrawal penalty. If you separate from your employer in or after the year you turn 55 (or 50 for certain public safety employees), you can take penalty-free withdrawals from that employer’s 401k — without waiting until 59½. This exception only applies to the 401k at the employer you left at age 55 or older. It does not apply to IRAs or to 401ks from previous employers. Rolling the money to an IRA eliminates the Rule of 55 benefit entirely — this is the single most important reason to consider leaving assets with a former employer for workers aged 55–59.

Reason 2 — Superior plan quality. Some large employers offer institutional-class index funds with expense ratios of 0.02–0.05% — lower than anything available to individual investors. If your former employer’s plan has genuinely excellent, low-cost options, leaving the money there may be preferable to rolling to an IRA with retail-class fund expenses.

Reason 3 — Creditor protection. ERISA-qualified 401k plans have robust federal creditor protection — generally shielded from creditors in bankruptcy and judgment proceedings. IRA creditor protection varies by state. For anyone in a profession with high lawsuit risk (physicians, attorneys, business owners), the creditor protection difference may favor keeping funds in a 401k.

The risks of leaving the money in place:

The most common risk is simply losing track of the account. Over a career with multiple job changes, a forgotten 401k is genuinely common — and the National Registry of Unclaimed Retirement Benefits estimates billions of dollars sit in accounts that former employees have lost contact with. You also lose the ability to make new contributions, and the plan’s fund lineup may change over time without your awareness. If your former employer is acquired or closes, the plan may be terminated, forcing a rollover decision under time pressure.

Named Example: David, 56, left his corporate job to pursue consulting. His former employer’s 401k holds $340,000. Because David separated from this employer at age 56, the Rule of 55 allows him to take penalty-free withdrawals from this specific 401k to fund business startup costs. If David rolls the money to an IRA, he loses this benefit entirely — and withdrawals before 59½ would trigger a 10% penalty on top of income taxes. David keeps the money in the former employer’s plan and takes selective withdrawals as needed. He plans to roll it to an IRA after turning 59½, when the early withdrawal penalty no longer applies.

Pro Tip: If you leave your 401k with a former employer, set a calendar reminder to review the account at least annually. Log in, verify your investment allocation is still appropriate, confirm your beneficiary designations are current, and make sure the plan administrator has your current contact information. An abandoned 401k can be transferred to unclaimed property if you become unreachable.

Option 2 — Roll Over to Your New Employer’s 401k Plan

Rolling to a new employer’s 401k is the simplest consolidation strategy — but it comes with plan quality trade-offs that most people don’t evaluate before executing.

How a rollover to a new employer plan works: Contact your new employer’s HR or plan administrator and confirm the plan accepts incoming rollovers — most do, but some plans have waiting periods before new employees can roll funds in. Request a direct rollover from your old plan to your new plan. The funds transfer directly without passing through your hands, maintaining full tax-deferred status with no taxes and no penalties.

The legitimate reasons to roll to a new employer’s 401k:

Simplicity is the biggest argument. One account is easier to manage than accounts scattered across former employers. A unified investment allocation across one larger balance is simpler to rebalance and monitor, and you only have one beneficiary designation to maintain. Understanding terms like vesting schedules and beneficiary designations makes the transition significantly smoother.

If you plan to retire from your new employer at or after age 55, rolling your old 401k balance into the new plan means that entire balance — including the rolled-over funds — potentially becomes eligible for the Rule of 55 at the new employer. Verify that the new plan accepts rollovers and permits Rule of 55 withdrawals before proceeding.

Many 401k plans also allow participants to borrow from their balance — IRA accounts do not allow loans. If you anticipate needing access to the funds before retirement and prefer the loan mechanism, keeping the money in a 401k preserves this option.

The risks and limitations:

Many employers — particularly small and mid-size businesses — offer plans with limited investment options and higher expense ratios. Rolling $280,000 from a former Fortune 500 plan (with 0.03% expense ratio institutional funds) into a small business plan (with 0.75% expense ratio retail funds) is a meaningful long-term cost. Before rolling to a new plan, review every available fund’s expense ratio and compare to what you could access in an IRA.

Many new employers also impose a waiting period before new employees can participate in the 401k — often 30–90 days, sometimes up to a year. During a waiting period, you cannot roll into the plan.

Roll to New Employer 401k vs. Roll to IRA

| Factor | New Employer 401k | IRA Rollover |

|---|---|---|

| Investment options | Limited to plan menu | Virtually unlimited |

| Expense ratios | Varies (plan-dependent) | As low as 0.03% (index funds) |

| Loan availability | Usually yes | No |

| Creditor protection | Strong (ERISA federal) | Varies by state |

| Rule of 55 applicability | Possible (if new employer, age 55+) | No |

| Setup complexity | Low (HR handles most steps) | Low-moderate (you choose provider) |

Source: RetireWealthPath.com analysis based on ERISA regulations and IRA rules, 2026.

Option 3 — Roll Over to an IRA (The Most Flexible Choice)

The IRA rollover is the right answer for most people in most situations — but only if executed correctly. Here’s why it wins, and precisely how to do it without triggering the costly mistakes that trap so many people.

Why the IRA rollover wins for most people:

An IRA at Fidelity, Vanguard, or Schwab gives you access to virtually any publicly traded investment — index funds with expense ratios of 0.03–0.10%, individual stocks, bonds, ETFs, REITs, and Treasury securities. For someone moving from a high-cost 401k to a low-cost IRA, the expense ratio reduction alone can add $50,000–$150,000 over a 20-year retirement horizon. For a deeper look at the comparison, see Roth IRA vs Traditional IRA: Which One Wins in 2026?

You’re also no longer dependent on your former employer remaining solvent, maintaining plan quality, or being reachable years into the future. You own and control the account directly at a major brokerage.

An IRA rollover also creates the ideal platform for Roth conversion strategies — rolling to a traditional IRA first, then converting to Roth in low-income years, is the foundation of one of the most powerful retirement tax strategies available. This option is not available within a 401k plan.

The step-by-step IRA rollover process:

Step 1 — Choose your IRA provider. Major providers: Fidelity, Vanguard, Charles Schwab — all offer rollover IRAs with zero account fees and access to ultra-low-cost index funds. Avoid insurance company IRAs (often paired with high-fee annuity products) and bank IRAs (limited investment options, often low returns). Open a “Rollover IRA” or “Traditional IRA” — the account type matters for tax purposes.

Step 2 — Request a direct rollover (NOT an indirect rollover). Contact your former employer’s 401k plan administrator and request a direct rollover to your new IRA. In a direct rollover, the check is made payable to “Fidelity FBO [Your Name]” — it never passes through your hands. This is critical: a check payable to you triggers mandatory 20% withholding, and you must deposit 100% of the original balance (including the withheld 20% from your own funds) within 60 days to avoid taxes and penalties on the withheld amount.

Step 3 — Complete the paperwork. Your new IRA provider will typically have a rollover request form or online process that initiates the transfer directly with your former plan. Processing time is typically 5–15 business days for funds to appear in your new IRA.

Step 4 — Invest the rolled-over funds. When the money arrives, it will sit in a money market fund initially — uninvested. This is a critical step many people miss. The money must be actively invested in your chosen funds — it does not invest automatically. Select your target asset allocation and invest the full rollover amount promptly.

Named Example: Margaret, 52, receives a check for $178,000 from her former employer’s plan — payable directly to her. She didn’t know the check should have been made payable to the IRA. The plan withheld 20% ($35,600), so Margaret’s check is for $142,400. To complete a valid rollover and avoid taxes and penalties, Margaret must deposit the full $178,000 into her IRA within 60 days. She must come up with the $35,600 difference from her own savings — or $35,600 is treated as a taxable distribution, generating $7,832 in income tax (22% bracket) plus a $3,560 early withdrawal penalty. Margaret scrambles to find the $35,600 — a stressful and entirely avoidable situation. Always request the direct rollover.

The 60-day rollover rule: If you receive a distribution (indirect rollover), you have exactly 60 calendar days to deposit the full original amount into an IRA or new employer’s 401k. The IRS allows one 60-day rollover per 12-month period — this is a hard limit. Missing the deadline results in the full amount being taxable as ordinary income in that year, plus the 10% penalty if you’re under 59½. The direct rollover eliminates this risk entirely. Use it.

Common Mistake: Leaving the rolled-over funds sitting in the IRA’s default money market fund for months or years after the rollover. The money market fund inside your rollover IRA may earn 4–5% in 2026 — but a diversified index fund portfolio earns a historical average of 7–10%. Every month of delay is compounding opportunity lost permanently. Log in and invest your rollover within the same week it arrives.

Option 4 — Cashing Out Your 401k (The Option That Almost Never Makes Sense)

This option deserves complete, honest coverage — including a precise quantification of what it costs — while acknowledging the limited circumstances where it may be genuinely necessary.

What cashing out actually costs:

When you cash out a 401k before age 59½, the plan immediately withholds 20% for federal taxes. You then owe full ordinary income tax on the entire balance — added to your other income for the year — plus the 10% early withdrawal penalty, plus potential state income tax. And you lose all future tax-deferred compounding on the withdrawn amount forever.

The Real Cost of Cashing Out a $100,000 401k (Under Age 59½, 22% Federal Bracket)

| Component | Amount | Notes |

|---|---|---|

| Starting balance | $100,000 | Pre-tax 401k balance |

| Federal income tax (22%) | −$22,000 | Added to taxable income |

| Early withdrawal penalty (10%) | −$10,000 | Waived at 59½ or specific exceptions |

| State income tax (example: 5%) | −$5,000 | Varies — zero in some states |

| Amount actually received | $63,000 | You receive 63 cents of every dollar |

| Lost future growth (7%, 15 years) | −$163,000 | The $100,000 would have grown to $263,000 |

| Total cost of cashing out | ~$200,000 | Direct tax + opportunity cost |

Source: Illustrative calculations based on 2026 federal tax rates and 10% early withdrawal penalty. State tax varies. For educational purposes only.

The act of cashing out doesn’t just cost the taxes and penalty. It costs 20 years of tax-deferred compounding on the full $100,000. One of the most common retirement myths is that cashing out a small old 401k is “not a big deal.” The math disagrees every time.

When is cashing out ever acceptable? Honestly, almost never. But genuine hardship exceptions exist: severe financial crisis with no other assets and no access to credit, a medical emergency requiring immediate funds from no other source, or facing homelessness or utility shutoff with no other options.

Before reaching for the cash-out button, exhaust these alternatives first: a 401k loan (if still employed with the plan), the Rule of 55 if you’re 55 and recently separated, IRA withdrawal exceptions (disability, 72(t) substantially equal periodic payments), or a home equity line of credit, personal loan, or family loan that preserves your retirement savings.

Named Example: Kevin, 47, receives a $68,000 401k distribution check after being laid off. His first instinct is to pay off credit card debt and cover living expenses. His financial advisor runs the numbers: after 20% mandatory withholding, 22% income tax, 10% penalty, and 4% state tax, Kevin nets $44,200 — losing $23,800 to taxes and penalties immediately. The $68,000 would have grown to approximately $267,000 by his planned retirement at 65. Kevin instead rolls the $68,000 to an IRA, lives on his emergency fund and part-time work for four months, and finds a new job. His retirement trajectory is preserved.

Pro Tip: Before cashing out a 401k for any reason, call your plan administrator and specifically ask: “Do I qualify for any penalty-free withdrawal exceptions?” Common exceptions include age 59½+, separation from service at age 55+, disability, substantially equal periodic payments, and medical expenses exceeding 7.5% of AGI. You may have access to penalty-free funds without knowing it — and that changes the entire calculation.

The Timing Decision — When Do You Need to Act?

Most people don’t realize that 401k decisions after leaving a job have real time constraints — and that some actions must happen before your last day of work.

Before your last day:

Complete any outstanding 401k loan repayments if possible — upon separation, some plans require immediate loan repayment or treat the outstanding balance as a taxable distribution. Review your vesting schedule: unvested employer contributions are forfeited upon separation. Gather the plan administrator’s contact information — phone, website, and participant portal login — before access may be revoked or complicated.

Named Example: Patricia, 53, is leaving her employer after 4 years. Her employer uses a 6-year graded vesting schedule: 20% per year, reaching 100% at 6 years. After 4 years, Patricia is 80% vested. Her employer match balance is $42,000 — but only $33,600 is vested. The $8,400 unvested amount would be forfeited the day she leaves. Patricia checks the vesting schedule before resigning and negotiates a start date at the new company that gives her one additional month, pushing her past the next vesting anniversary and preserving an additional $8,400. That’s $8,400 for one phone call.

The timeline after leaving:

In the first 30 days after separation, receive your final account statement, verify your vested balance, and confirm all account details. In days 30–60, make your rollover decision and initiate the process if you’re moving funds. Note that some plans require action within 30–60 days for balances below certain thresholds.

The small balance force-out: If your vested balance is under $1,000, the plan can automatically cash you out. If your balance is $1,000–$5,000, the plan can automatically roll it into a default IRA. If your balance exceeds $5,000, you have full control and timing flexibility.

What to do if you have multiple old 401ks: Americans average 12 job changes — which means potentially 12 old 401k accounts to track. The National Registry of Unclaimed Retirement Benefits (unclaimedretirementbenefits.com) and the Department of Labor’s Abandoned Plan Database can help locate forgotten accounts. Consolidating multiple old accounts into a single IRA rollover simplifies management dramatically.

It’s also worth noting that your retirement readiness overall is directly tied to how efficiently you manage these transition moments. Every dollar left in a suboptimal account or, worse, cashed out, affects the final number you can rely on in retirement.

The Rollover IRA vs. New Traditional IRA — An Important Distinction

Many people don’t know there is a meaningful difference between a “Rollover IRA” and a regular traditional IRA — and that conflating the two can cost them retirement options they didn’t even know they had.

What is a Rollover IRA? A traditional IRA specifically designated to hold assets rolled over from an employer’s qualified plan (401k, 403b, 457b). Functionally identical to a traditional IRA in terms of investment options, contribution rules, and tax treatment — but the distinction matters for one critical reason: the ability to roll the funds back into a future employer’s 401k plan.

Why keeping the rollover IRA separate matters: If you keep your rolled-over 401k funds in a dedicated rollover IRA — not mixed with regular IRA contributions — you preserve the option to roll those funds into a future employer’s 401k plan. Once you mix rolled-over 401k funds with regular IRA contributions, some plans will not accept a subsequent rollover because they cannot verify the entire balance originated from a qualified plan.

The pro-rata rule complication: Mixing pre-tax 401k rollover funds with non-deductible IRA contributions creates a pro-rata problem for future backdoor Roth conversions. If you have $100,000 in a rollover IRA (pre-tax) and add $8,000 in non-deductible contributions, then attempt a backdoor Roth conversion, the pro-rata rule taxes 92.6% of any amount converted — eliminating the tax benefit of the strategy entirely. The solution: keep rollover IRA and regular IRA contributions in separate accounts. Alternatively, roll the pre-tax IRA funds back into a new employer’s 401k before executing a backdoor Roth.

Named Example: Susan, 49, rolls $220,000 from her former employer’s 401k into a traditional IRA at Vanguard. Two years later, she earns $185,000 — above the Roth IRA income limit — and wants to do a backdoor Roth. Her $220,000 rollover IRA balance triggers the pro-rata rule, making 96.5% of any conversion taxable. Susan’s solution: she rolls the $220,000 rollover IRA back into her new employer’s 401k (which accepts incoming rollovers), leaving her IRA balance at zero. Now she can execute the backdoor Roth without pro-rata complications. This rollback option was available specifically because she had maintained the rollover IRA separately from any regular IRA contributions.

Pro Tip: When setting up your rollover IRA, clearly label it as a “Rollover IRA” with the provider — Fidelity, Vanguard, and Schwab all offer this account designation. This labeling has no tax effect but serves as an administrative reminder to keep rolled-over funds separate from regular IRA contributions. The two minutes it takes to label the account correctly can preserve thousands of dollars in future strategic options.

Special Situations — Job Loss, Early Retirement, and Self-Employment

The standard four-option framework plays out differently in specific life situations. Here’s how to apply it when the circumstances are anything but standard.

Job Loss and Layoff

A layoff combines income disruption with the 401k decision — creating pressure to make a permanent decision while under financial stress. The worst outcomes almost always happen when these two problems are conflated. “I need money now” should not automatically mean “I’ll cash out my 401k.”

If you receive a severance package, your income for the year may be higher than normal — a Roth conversion or rollover in this year may push you into a higher bracket. Consider waiting until the following year for any Roth conversion if your income is elevated. If you have a 401k loan outstanding at the time of layoff, many plans require immediate repayment — failure to repay treats the outstanding balance as a taxable distribution plus potential penalty. Address this immediately, before any other 401k decision.

Early Retirement (Before Age 59½)

If you retire at or after the year you turn 55, penalty-free withdrawals from the 401k at the employer you just left are available under the Rule of 55. This is one of the rare cases where leaving the 401k with the former employer is strongly preferable to rolling to an IRA. Once rolled to an IRA, penalty-free access before 59½ requires the 72(t) SEPP strategy — more complex and less flexible than simply using the Rule of 55.

Early retirees between 55 and 59½ who use the Rule of 55 can take strategic partial withdrawals from their former employer’s 401k to fund living expenses — a “bridge income” strategy. This preserves the IRA rollover for later — rolled to an IRA after 59½ eliminates the penalty concern entirely. For context on how this interacts with Social Security timing, see Best Age to Claim Social Security Benefits — for many early retirees, the 401k bridge strategy is directly tied to delaying Social Security for a larger benefit.

If you’re setting your overall retirement number and wondering whether early retirement is even feasible, How to Set Your Retirement Number walks through the complete calculation.

Moving to Self-Employment or Consulting

Self-employed individuals can establish a Solo 401k — a 401k plan for the self-employed — which can accept incoming rollovers from former employer plans. Rolling an old 401k into a Solo 401k maintains 401k creditor protection, preserves rollback-to-401k optionality, and provides the highest possible contribution limits for self-employed savers. A Solo 401k also preserves the ability to do a clean backdoor Roth conversion by keeping IRA accounts separate from the Solo 401k rollover.

Named Example: Robert, 54, leaves a corporate position to start a consulting business. His former employer’s 401k holds $415,000. Robert establishes a Solo 401k for his consulting business and rolls the $415,000 directly from his former employer’s plan into his Solo 401k. He maintains federal ERISA creditor protection, retains the ability to roll back into a future employer’s plan, and can still make Solo 401k employee contributions from his consulting income — up to $31,000 per year at age 50+. Two years later, when his consulting income is strong and predictable, he converts portions of the Solo 401k to a Roth IRA annually in his lower-bracket years.

Frequently Asked Questions

How long do I have to roll over my 401k after leaving a job?

It depends on your balance and your plan’s rules. If your vested balance exceeds $5,000, most plans allow you to leave the money indefinitely — no immediate rollover deadline. If your balance is $1,000–$5,000, the plan may automatically roll it to a default IRA. If your balance is under $1,000, the plan may cash it out automatically. If you receive a distribution check (indirect rollover), you have exactly 60 calendar days to deposit the full original amount into a new IRA or employer plan. Use the direct rollover method to eliminate this deadline entirely.

Will I owe taxes on a 401k rollover if I do it correctly?

No — a direct rollover from a 401k to an IRA (or new employer’s 401k) is a non-taxable event. The money moves from one tax-advantaged account to another without triggering any income tax or penalties. The critical requirement is that the transfer be “direct” — the check is payable to the new IRA custodian, not to you personally. If a check is payable to you, 20% mandatory withholding is triggered and you have 60 days to deposit the full original amount (including the withheld 20%) to complete the rollover without tax consequences.

Should I roll my 401k into a Roth IRA instead of a traditional IRA?

Rolling a pre-tax 401k directly into a Roth IRA is a Roth conversion rollover — and it is a taxable event. The entire converted amount is added to your taxable income in the year of conversion. For most people, converting a large 401k balance all at once would push them into a very high tax bracket. The better strategy: roll the pre-tax 401k to a traditional IRA first, then convert to Roth in strategic annual amounts over multiple years — staying in the 12–22% bracket each year. This staged approach minimizes the total tax paid on the conversion. The full comparison is in Roth IRA vs Traditional IRA: Which One Wins in 2026?

I have small 401k accounts at three former employers. What should I do?

Consolidate them — ideally into a single IRA rollover at Fidelity, Vanguard, or Schwab. Managing three separate accounts at former employers means tracking three plan administrators, three investment lineups, three fee structures, and three beneficiary designations — with the added risk of losing contact with any of them over time. A single IRA rollover simplifies everything, gives you full investment control, and reduces administrative risk. Open one IRA, then initiate direct rollover requests from each former employer’s plan.

My former employer’s 401k is invested in company stock. Do I need to do anything special before rolling it over?

Potentially yes. Investigate the Net Unrealized Appreciation (NUA) strategy before rolling company stock to an IRA. NUA allows you to distribute employer stock from the 401k in kind — paying only ordinary income tax on the original cost basis, while the appreciation is taxed at the lower long-term capital gains rate when eventually sold. This can be dramatically more tax-efficient than rolling the stock to an IRA, where all future withdrawals are taxed as ordinary income. NUA has specific eligibility requirements — consult a fee-only financial advisor or CPA before making any decision involving employer stock in a 401k.

The Bottom Line

The decision about what to do with your 401k when you quit is one of the most consequential and most neglected in all of retirement planning. Here are the three things that matter most.

The IRA rollover wins for most people in most situations. It offers the most investment freedom, the lowest costs, and the most strategic flexibility for future Roth conversions and retirement income management. Execute it as a direct rollover, invest the funds promptly upon arrival, and keep the rollover IRA separate from regular IRA contributions.

The Rule of 55 is the critical exception. If you are aged 55–59½ and need access to retirement funds before 59½, leaving the 401k with the former employer preserves penalty-free access that an IRA rollover eliminates. This is not a minor detail — it’s a potentially six-figure difference in tax exposure for early retirees.

Cash-out is almost never the right answer. The combined cost of taxes, penalties, and lost compounding typically destroys 35–40% of the balance immediately and eliminates decades of future growth. Exhaust every other option first.

Now that you know what to do with your old 401k, the next step is maximizing what you’re building in the new one. Read How to Maximize Your 401k in Your 50s for the complete contribution and investment strategy. Not sure if you’re fully on track? The Retirement Readiness Quiz takes five minutes and gives you a real-time picture of where you stand.

Your 401k has been growing quietly for years. The day you leave a job, it needs one good decision — not to be ignored, forgotten, or cashed out. Give it that decision, and it will keep growing for decades more.

Disclaimer: The content on RetireWealthPath.com is for informational and educational purposes only and does not constitute financial, tax, or legal advice. We are not licensed financial advisors. 401k rollover rules, early withdrawal penalty exceptions, the Rule of 55, mandatory withholding requirements, vesting schedule provisions, force-out balance thresholds, NUA strategy eligibility, and all other provisions referenced in this article reflect 2026 IRS and ERISA guidelines and are subject to change by legislation or regulatory policy. All calculations, named examples, and strategic recommendations — including David, Margaret, Kevin, Patricia, Susan, and Robert — are for illustrative and educational purposes only and do not represent guaranteed outcomes. Individual plan provisions vary significantly — always review your specific plan’s Summary Plan Description and consult with your plan administrator before making rollover decisions. Always consult a qualified financial professional, CPA, or tax advisor before making 401k distribution, rollover, or withdrawal decisions. Retirement planning involves risk and individual results will vary.