Divorced Spouse Social Security Rights [2026 Guide]

Important Note: Social Security divorced spouse benefits cannot be waived or eliminated in a divorce settlement. If you signed a divorce agreement that included language about Social Security, it has no legal effect on your federal benefit rights. Your rights exist regardless of what any court order says.

If you were married for 10 or more years and are now divorced, you may be entitled to Social Security benefits worth hundreds of dollars per month — based entirely on your ex-spouse’s earnings record. Most divorced Americans never claim this benefit. Many don’t even know it exists.

Divorce after a long marriage can leave one partner — often the lower-earning spouse — in a significantly more vulnerable retirement position. Social Security’s divorced spouse benefit exists specifically to address this reality. It recognizes that a long marriage is a shared economic partnership, and the lower-earning spouse is entitled to a share of the Social Security benefit built during that partnership.

This guide is not just an explanation of the rules. It is a complete framework for understanding your divorced spouse Social Security rights and using them to maximize your lifetime retirement income. It’s most critical for people who divorced after a long marriage, left the workforce to raise children or support a spouse’s career, and anyone significantly out-earned by their ex-spouse.

Let’s start with the five eligibility requirements — because knowing whether you qualify is the essential first step.

The Five Eligibility Requirements — Do You Qualify?

Eligibility is the first question on every reader’s mind. Here are the five requirements with plain-English explanations — including the nuances where people most commonly self-disqualify incorrectly.

Requirement 1 — The 10-Year Marriage Rule

Your marriage to the ex-spouse must have lasted at least 10 years. The SSA measures from the date of marriage to the date the divorce became legally final — not the date of separation. Even a years-long separation does not count as divorce for SSA purposes.

The threshold is applied exactly:

- 9 years and 11 months: does not qualify

- 10 years and 1 day: qualifies

If you were married to more than one person for at least 10 years each, you may be eligible on more than one ex-spouse’s record — though you can only receive one benefit at a time. Each marriage is evaluated independently.

Example: Linda married James in 1988 and their divorce was finalized in 1998 — exactly 10 years. Linda qualifies. Her second marriage to Robert lasted 8 years — she does not qualify on Robert’s record. But her 10-year marriage to James preserves her divorced spouse benefit eligibility for life.

Requirement 2 — Current Marital Status

You must be currently unmarried at the time you claim. Remarriage disqualifies you from claiming on an ex-spouse’s record — but only for as long as that remarriage continues. If your subsequent marriage ends through death, divorce, or annulment, your eligibility on your original ex-spouse’s record is typically restored.

This has significant planning implications: remarrying before age 60 eliminates both divorced spouse benefits and divorced survivor benefits. Understanding this before making life decisions is a financial reality worth taking seriously.

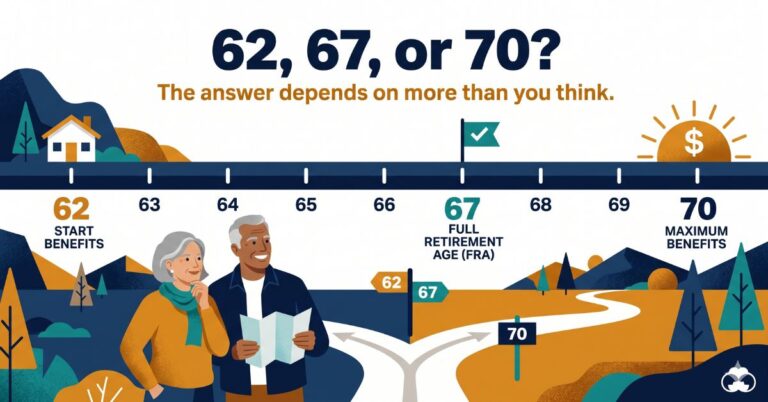

Requirement 3 — Age Requirement

You must be at least 62 years old to claim divorced spouse benefits. Claiming before your Full Retirement Age (FRA) results in a permanent reduction — the same proportional schedule as regular spousal benefits. At FRA, you receive the full divorced spouse benefit amount.

Requirement 4 — The Ex-Spouse’s Eligibility (With a Crucial Exception)

A current (married) spouse cannot claim spousal benefits until the working spouse has actually filed for their own benefit. Divorced spouses are different. After at least 2 years of divorce, you can claim your divorced spouse benefit completely independently — regardless of whether your ex has filed or not.

Example: Patricia, 63, divorced Michael, 64, four years ago. Michael plans to delay his own Social Security until 70. A current spouse would have to wait for Michael to file. Because Patricia has been divorced for more than 2 years, she can claim her divorced spouse benefit right now — without Michael’s knowledge, consent, or action.

This independent filing right is one of the most powerful advantages divorced spouses have over current spouses. For a broader look at how the earnings-based calculation works, see our guide on how Social Security is calculated.

Requirement 5 — Your Own Benefit Comparison

If you have your own Social Security work record, the SSA pays the higher of your own retirement benefit or the divorced spouse benefit (up to 50% of your ex’s Primary Insurance Amount, or PIA). You cannot receive both in full simultaneously.

Under deemed filing rules, if you’re eligible for both benefits, you’re required to file for both at once and receive the higher amount. You cannot strategically claim only one while delaying the other (with a very limited exception for those born before January 2, 1954 — most of whom have already passed age 70 by 2026).

Eligibility Requirements Quick Reference

| Requirement | The Rule | Common Mistake |

|---|---|---|

| Marriage length | At least 10 years (to final divorce date) | Counting from separation instead of final divorce |

| Current marital status | Must be currently unmarried | Assuming remarriage permanently eliminates eligibility |

| Age | At least 62 | Claiming before FRA without understanding reduction |

| Ex-spouse eligibility | Must be 62+ and divorced 2+ years | Waiting for ex to file — not required after 2-year divorce |

| Own benefit comparison | SSA pays higher of own or divorced spouse benefit | Expecting to receive both in full simultaneously |

Source: Social Security Administration divorced spouse benefit rules, 2026.

How Much Is the Divorced Spouse Benefit — Calculating Your Amount

The maximum divorced spouse benefit is 50% of your ex-spouse’s PIA — the benefit they would receive at their Full Retirement Age. This maximum is only available if you claim at your own FRA. Claiming earlier permanently reduces it.

Critical distinction: The divorced spouse benefit is based on your ex’s PIA, not what they actually receive. If your ex delayed to age 70 and collects $4,000/month, your benefit is still based on their FRA amount. Delayed retirement credits earned by your ex do not flow through to you — there is no advantage to waiting for them to claim. For a complete picture of how FRA and delayed credits work, read our post on the best age to claim Social Security.

Divorced Spouse Benefit at Different Claiming Ages (ex-spouse PIA: $3,000)

| Your Claiming Age | % of Maximum | Monthly Benefit | Annual Amount |

|---|---|---|---|

| 62 | 65% | $975 | $11,700 |

| 63 | 70% | $1,050 | $12,600 |

| 64 | 75% | $1,125 | $13,500 |

| 65 | 83.3% | $1,250 | $15,000 |

| 66 | 91.7% | $1,375 | $16,500 |

| 67 (FRA) | 100% | $1,500 | $18,000 |

Source: Illustrative calculations using SSA divorced spouse benefit reduction schedule, 2026. Individual benefits vary.

Own-benefit offset example:

Susan’s own PIA is $900/month. Her ex-husband David’s PIA is $3,200. The divorced spouse maximum is 50% of $3,200 = $1,600. Susan’s top-up = $1,600 − $900 = $700/month. At FRA, Susan receives her own $900 plus a $700 supplement = $1,600/month total.

Pro Tip: To estimate your potential divorced spouse benefit, you need your ex-spouse’s PIA — not their permission. Contact your local SSA office, or estimate their PIA using Social Security benefit calculators if you have a general sense of their career earnings. The SSA will verify the actual amount when you apply. To understand what the PIA calculation involves, see our explainer on how Social Security is calculated.

The Independent Filing Advantage — The Most Valuable Right Divorced Spouses Have

The ability to file independently is the single most powerful practical advantage divorced spouses hold over current spouses. Here’s what it means in full:

After 2 years of divorce, a divorced spouse can file for benefits regardless of whether the ex-spouse has filed. The SSA does not notify your ex-spouse. Their benefit is completely unaffected by your claim. Their current spouse’s benefits are also unaffected.

The 2-year waiting period exists to prevent people from divorcing specifically to exploit this right. During the first 2 years after divorce, the rules mirror those for current spouses — you would need to wait for your ex to file.

Why this matters: If your ex has decided to delay to age 70, you do not wait. You optimize your own claiming timeline completely independently — with no coordination, communication, or notification to your ex required.

Common Mistake: Waiting years for an ex-spouse to file before claiming divorced spouse benefits. After 2 years of divorce, you have the legal right to claim at your own optimal time. Waiting unnecessarily means losing years of benefit income you can never recover. If you’re eligible and over 62, contact the SSA now.

Divorced Spouse Benefits vs. Your Own Retirement Benefit — Building the Optimal Strategy

The core strategic question is: which is higher — your own Social Security benefit (potentially maximized at age 70) or 50% of your ex-spouse’s PIA (maximized at your FRA)?

Under deemed filing, the SSA automatically pays the higher of the two when you claim. Your strategic focus should be choosing the right claiming age to maximize whichever benefit comes out on top. This decision is part of a larger framework — our post on the Social Security for married couples strategy covers the same FRA and delay tradeoffs that apply here.

Three Strategic Scenarios

Scenario A — Own benefit at 70 exceeds divorced spouse benefit at FRA:

Carol’s own PIA is $2,000. At 70, her own benefit = $2,480 (24% delayed credit). Her ex-husband’s PIA is $3,500; divorced spouse maximum = $1,750. Since $2,480 > $1,750, Carol’s own benefit at 70 wins. Strategy: delay to 70.

Scenario B — Divorced spouse benefit at FRA exceeds own benefit at 70:

Maria’s own PIA is $800. At 70, her own benefit = $992. Her ex-husband’s PIA is $3,800; divorced spouse maximum = $1,900. Since $1,900 > $992, the divorced spouse benefit is better. Strategy: claim at FRA (67) — no benefit to waiting past FRA since divorced spouse benefits don’t earn delayed credits.

Scenario C — Benefits are close:

Jennifer’s own PIA is $1,400. At 70, her own benefit = $1,736. Her ex’s PIA is $3,200; divorced spouse maximum = $1,600. The $136/month difference has a break-even of 423 months — age 105. Jennifer is unlikely to reach 105. Strategy: almost certainly claim divorced spouse benefit at FRA.

Strategic Comparison: Own Benefit vs. Divorced Spouse Benefit

| Situation | Own Benefit at 70 | Divorced Spouse at FRA | Recommended Strategy |

|---|---|---|---|

| Own benefit at 70 > divorced spouse at FRA | $2,480 | $1,750 | Delay to 70 — own benefit wins |

| Divorced spouse at FRA > own benefit at 70 | $992 | $1,900 | Claim at FRA — divorced spouse wins |

| Small difference favoring own benefit at 70 | $1,736 | $1,600 | Usually claim at FRA — break-even too far |

| Very large own benefit at 70 | $3,500 | $1,800 | Delay to 70 — own benefit clearly wins |

| Minimal own benefit record | $400 | $1,500 | Claim at FRA — divorced spouse dominant |

Source: RetireWealthPath.com analysis based on SSA benefit calculation rules. Illustrative purposes only.

Bottom line: For most divorced spouses — especially those who took time away from the workforce — the divorced spouse benefit at FRA is the dominant benefit. Waiting past FRA adds nothing to the divorced spouse benefit.

Divorced Survivor Benefits — The Critical Benefit Most People Miss

When an ex-spouse dies, a new and potentially larger benefit becomes available: the divorced survivor benefit. This is worth up to 100% of what the deceased ex-spouse was receiving — far larger than the divorced spouse benefit, which maxes at 50% of PIA. For a full explanation of survivor benefit mechanics, see our post on Social Security survivor benefits explained.

Eligibility for divorced survivor benefits:

- Married to the deceased ex-spouse for at least 10 years

- Currently unmarried — OR remarried at age 60 or later

- At least age 60 (or 50 if disabled)

- No minimum time since the divorce — even a divorce finalized 30 years ago still qualifies

The divorced survivor’s benefit does capture delayed retirement credits. If your ex delayed to 70, your divorced survivor benefit is based on their full delayed amount.

Example: Helen, 67, was married to Frank for 15 years before their 1995 divorce. Frank recently passed away at 74, having delayed his Social Security to 70 and receiving $4,100/month. Helen has been collecting her own benefit of $1,600/month. She is now eligible for a divorced survivor benefit of $4,100/month — more than 2.5× her own benefit. Frank’s current wife receives her own independent survivor benefit; Helen’s claim does not affect it.

Dual benefit strategy for divorced survivors: You can claim your own retirement benefit early at 62, then switch to the divorced survivor benefit at FRA when it maxes out — or claim the divorced survivor benefit at 60 and switch to your own benefit at 70 if that will ultimately be larger. Choose based on which benefit is biggest at its maximum.

Pro Tip: The SSA does not proactively notify divorced former spouses of a death. If you were married to someone for at least 10 years and have lost contact with their family, consider periodically checking public records or obituary services. A divorced survivor benefit worth thousands per month may be available without your knowledge.

Myth-Busting — The Seven Most Damaging Misconceptions About Divorced Spouse Benefits

Misconceptions about these benefits are extraordinarily common — and each one costs real money.

Myth 1 — “Claiming on my ex’s record will reduce their benefit.” Reality: Your divorced spouse benefit has zero effect on your ex-spouse’s monthly benefit. The SSA calculates and pays your benefit entirely separately.

Myth 2 — “My ex-spouse has to agree or be notified before I claim.” Reality: The SSA does not notify your ex-spouse when you file. You need no permission, cooperation, or even their knowledge. After 2 years of divorce, you file independently.

Myth 3 — “I gave up my right to these benefits in the divorce settlement.” Reality: Social Security divorced spouse benefits cannot be waived or eliminated in a divorce settlement. They are established by federal law. No divorce attorney or judge can remove them. This is arguably the single most important fact in this entire post.

Myth 4 — “I already remarried so I’ve permanently lost this benefit.” Reality: If your subsequent marriage ends by death, divorce, or annulment, your eligibility on your original ex-spouse’s record is typically restored.

Myth 5 — “If I wait for my ex to claim at 70, I’ll get a bigger benefit.” Reality: The divorced spouse benefit is capped at 50% of your ex’s PIA — their FRA amount. Delayed credits earned by your ex do not increase your divorced spouse benefit. There is no advantage to waiting for them to claim.

Myth 6 — “I can’t get these benefits because I don’t know my ex’s Social Security number.” Reality: While an SSN speeds up the process, it is not strictly required. The SSA can locate records using the ex-spouse’s full name, date of birth, and state of birth.

Myth 7 — “I make too much money to qualify.” Reality: There is no income limit that disqualifies you from divorced spouse benefits. Investment income, rental income, IRA withdrawals, and pension income do not affect eligibility or benefit amounts. The only complication is earned income (wages or self-employment) for those below FRA — which triggers the earnings test, temporarily reducing but not eliminating benefits.

Common Mistake: Relying on your divorce attorney, a family member, or a financial advisor who isn’t specifically knowledgeable about Social Security. Divorced spouse rights are governed entirely by federal SSA regulations — not state divorce law or court orders. When in doubt, contact the SSA directly or consult a certified Social Security specialist.

The Earnings Test and Taxes — How They Affect Divorced Spouse Benefits

The Earnings Test Before FRA

If you claim divorced spouse benefits before FRA and continue working, the earnings test applies exactly as it does to regular retirement benefits.

- 2026 threshold: $22,320/year ($1,860/month)

- For every $2 earned above the threshold, $1 in benefits is withheld

- In the calendar year you reach FRA: higher threshold of $59,520, $1 withheld per $3 over

Withheld benefits are not lost — they are credited back at FRA as a permanent benefit increase. Investment income, rental income, and IRA withdrawals do not trigger the earnings test. See our full post on how work in retirement affects SS benefits for more detail.

Federal Taxation of Divorced Spouse Benefits

Divorced spouse Social Security benefits are taxed under the same combined income formula as all SS benefits.

Combined income = AGI + Non-taxable interest + 50% of Social Security benefits

| Combined Income (Single Filer) | % of SS Benefits Taxable |

|---|---|

| Below $25,000 | 0% |

| $25,000 – $34,000 | Up to 50% |

| Above $34,000 | Up to 85% |

Divorced individuals file as single, which means lower thresholds than married couples — potentially resulting in a higher SS tax burden at the same total income level.

Tax mitigation strategies worth exploring:

- Traditional IRA contributions (if still earning income) to reduce AGI

- Qualified Charitable Distributions (QCDs) after age 70½ to reduce AGI

- Roth conversions in lower-income years to reduce future taxable IRA withdrawals

- Strategic timing of IRA withdrawals to stay below the 85% taxation threshold

Divorced Spouse Benefit After Tax Impact (Single Filer, 2026)

| Annual Divorced Spouse Benefit | Other Annual Income | Combined Income | % of SS Taxable | After-Tax Benefit (Est.) |

|---|---|---|---|---|

| $18,000 | $15,000 | $24,000 | 0% | $18,000 |

| $18,000 | $20,000 | $29,000 | Up to 50% | ~$15,750 |

| $18,000 | $30,000 | $39,000 | Up to 85% | ~$13,590 |

| $18,000 | $45,000 | $54,000 | Up to 85% | ~$13,590 |

Illustrative calculations based on 2026 IRS Social Security taxation formula. Actual tax impact depends on deductions, credits, and state taxes.

Special Situations — Multiple Ex-Spouses, Long Gaps, and Complex Histories

Multiple Ex-Spouses

If you were married to more than one person for at least 10 years each, you may be eligible on multiple records — but you can only receive one benefit at a time. The SSA pays the highest available.

Example: Patricia was married to Alan for 12 years (divorced 1992) and George for 11 years (divorced 2010). Alan’s PIA is $3,400; George’s is $2,800. Patricia claims on Alan’s record ($1,700/month). If Alan later dies, she can evaluate switching to Alan’s divorced survivor benefit (up to 100% of what he was receiving).

When the Ex-Spouse Is Significantly Younger

The ex-spouse must be at least 62 for you to claim. If your ex is significantly younger, you may need to wait for them to reach 62 — even if you’ve already passed your own FRA.

The Windfall Elimination Provision (WEP) and Government Pension Offset (GPO)

If you receive a pension from non-SS-covered employment (some state/local government jobs):

- WEP may reduce your own Social Security benefit — but it does not affect your divorced spouse benefit

- GPO is more significant: it reduces your divorced spouse benefit by two-thirds of your government pension amount, which can eliminate the divorced spouse benefit entirely

Pro Tip: If you worked in state or local government and receive a pension, ask the SSA specifically about GPO impact before making any plans based on divorced spouse benefits. Discovering this at claiming time can be financially devastating. For a full explanation of WEP and GPO terms, our retirement planning vocabulary guide is a helpful reference.

Step-by-Step Action Plan — Claiming Your Divorced Spouse Benefits

Everything in this guide comes down to seven actionable steps you can start today.

Step 1 — Verify your eligibility this week

- [ ] Marriage lasted at least 10 years to final divorce date?

- [ ] Currently unmarried (or remarried at 60 or later)?

- [ ] At least 62 years old?

- [ ] Ex-spouse at least 62 and divorced 2+ years? (Or already deceased?)

- [ ] No government pension that would trigger GPO?

If you check all five boxes, proceed. If anything is uncertain, contact the SSA for an official determination. Our retirement readiness quiz includes a Social Security category that can help you identify gaps in your planning.

Step 2 — Gather your ex-spouse’s information Collect: full legal name, date of birth, Social Security number (helpful but not required), state of birth, your marriage certificate, and your divorce decree.

Step 3 — Pull your own Social Security statement Log into ssa.gov/myaccount and download your full statement. Note your PIA and your projected benefit at 62, FRA, and 70. Verify your earnings record for errors.

Step 4 — Estimate your ex-spouse’s PIA Call the SSA (1-800-772-1213) and explain you’re a divorced spouse seeking benefit information. With identifying information about your ex, the SSA can help you understand the benefit available.

Step 5 — Model your optimal claiming strategy Compare your own benefit at 70 versus the divorced spouse benefit at your FRA using the framework from the strategy section above. If the divorced spouse benefit is larger — claim at FRA. If your own benefit at 70 is clearly larger — delay to 70.

Step 6 — Consider consulting a Social Security specialist For situations involving multiple ex-spouses, GPO impact, survivor benefits on a deceased ex-spouse, or complex tax situations, a fee-only financial advisor can model the full range of scenarios.

Step 7 — Apply for benefits Contact the SSA approximately 3 months before your planned claiming date:

- Call 1-800-772-1213 to schedule an appointment

- Visit your local Social Security office in person (recommended for divorced spouse claims — more complex than standard retirement claims)

- Bring: marriage certificate, divorce decree, birth certificate, and any deceased ex-spouse’s documentation if claiming survivor benefits

Frequently Asked Questions

My divorce was finalized 25 years ago. Is it too late to claim?

No — there is no time limit on claiming divorced spouse benefits. As long as you meet the five eligibility requirements, the elapsed time since divorce is completely irrelevant. People who divorced decades ago and have lost all contact with their ex often retain full eligibility. Contact the SSA with whatever identifying information you have.

My ex-spouse doesn’t know I plan to claim on their record. Will the SSA tell them?

No — the SSA does not notify your ex-spouse when you apply for divorced spouse benefits. Your claim is processed privately and independently. Your ex-spouse’s benefit is unaffected, so there is no reason for the SSA to contact them about your application.

Can my ex-spouse’s current wife claim spousal benefits at the same time I claim divorced spouse benefits?

Yes — both the current spouse and a divorced spouse can claim benefits on the same worker’s record simultaneously. Neither affects the other. The worker’s own benefit is also completely unaffected. Social Security divorced spouse benefits are specifically designed not to create conflict between current and former spouses.

My ex-spouse worked in cash and probably underreported income. Will that hurt my divorced spouse benefit?

Yes — the divorced spouse benefit is based entirely on your ex-spouse’s official SSA earnings record. Unreported cash income does not appear in their record and does not count toward their PIA. If your ex underreported consistently, their official PIA may be significantly lower than their actual earnings suggest.

I was a stay-at-home parent for 20 years and have almost no Social Security earnings of my own. Is the divorced spouse benefit my only option?

It may be your primary option — and it can be substantial. At FRA you would receive 50% of your ex-spouse’s PIA, which for a full-time worker over 35+ years could be $1,200–$2,000+ per month. If your ex-spouse predeceases you, the divorced survivor benefit increases to up to 100% of what they were receiving. Even part-time work in your remaining pre-retirement years can build your own SS record. A certified Social Security specialist can model all of your specific options.

Conclusion

You now understand exactly what the divorced spouse benefit is, who qualifies, how much it pays, and how to claim it. An unknown right has become an actionable financial resource.

Three takeaways to carry with you:

- The 10-year marriage rule is the key threshold — and the divorced spouse benefit cannot be taken away by any divorce settlement, court order, or ex-spouse’s decision.

- After 2 years of divorce, you can file completely independently — no coordination, permission, or notification to your ex is required.

- When your ex-spouse dies, the benefit can increase to 100% of what they were receiving as a divorced survivor benefit — check eligibility even decades after a divorce.

Now that you understand your divorced spouse rights, the next step is building your complete Social Security strategy. Read our guide on the best age to claim Social Security for the full claiming framework — or explore Social Security survivor benefits explained to understand what happens to your benefit when your ex-spouse passes away.

A long marriage built this benefit. The law says it belongs to you. Claim it.

Disclaimer: The content on RetireWealthPath.com is for informational and educational purposes only and does not constitute financial, tax, or legal advice. All calculations, named examples, and strategy comparisons are illustrative only. Social Security rules referenced reflect 2026 SSA guidelines and are subject to change. Always contact the Social Security Administration directly and consult a qualified financial professional before making claiming decisions.