Social Security Strategy for Married Couples [2026]

Most married couples treat Social Security as two separate decisions. That single mistake can cost them $150,000 or more in lifetime benefits — and it cannot be undone once made.

Here is the core insight this entire post is built on: for married couples, Social Security is not two independent decisions. It is one coordinated household income strategy with interdependent moving parts. The timing of one spouse’s claim directly affects what the other spouse receives — both while both are alive, and after one of them dies.

That complexity — spousal benefits, survivor benefits, claiming sequences, earnings gaps, age differences — is genuinely difficult to navigate without a clear framework. By the end of this guide, you will have one. We will cover every major scenario married couples face, with named examples, comparison tables, and specific recommendations for each situation.

This post is especially critical for three groups: couples with a significant earnings gap between spouses, couples with an age difference of three or more years, and couples where one spouse has health concerns. If any of those describe you, read carefully — the stakes are highest in exactly those situations.

Let’s start with the foundation — the two benefit types that exist specifically for married couples and how each one is calculated.

The Two Benefits Married Couples Have That Singles Don’t

The Social Security system offers two distinct benefits designed specifically for married couples — spousal benefits and survivor benefits. These are different in calculation, eligibility, and strategy. Most people know the names. Very few understand how they actually work.

Spousal Benefits — Income While Both Spouses Are Alive

A spousal benefit is a benefit available to a married person based on their spouse’s earnings record rather than their own. It is worth up to 50% of the working spouse’s Primary Insurance Amount (PIA) — the benefit they would receive at their Full Retirement Age. A spouse who never worked a single day in a covered job can still qualify. No earnings record required.

Key eligibility rules:

- Must be currently married (divorced spouses have separate rules — covered later in this guide)

- The working spouse must have already filed for their own Social Security before the non-working or lower-earning spouse can claim a spousal benefit

- Minimum age to claim: 62 (with a permanent reduction) or Full Retirement Age (for the full 50%)

- Must have been married for at least one continuous year before claiming

One critical nuance — own benefit comes first: If the lower-earning spouse has their own Social Security record, they cannot choose between their own benefit and the spousal benefit. The SSA automatically pays the higher of the two. In practice, the SSA pays the lower earner’s own benefit first, then adds a “spousal supplement” if 50% of the higher earner’s PIA would be larger. This is called deemed filing — both benefits are filed simultaneously, automatically.

What the spousal benefit is NOT: The spousal benefit does not increase if the higher earner delays past Full Retirement Age. It is permanently capped at 50% of the higher earner’s PIA — regardless of when the higher earner actually claims. This is the most misunderstood rule in married couple Social Security planning, and we address it head-on in the next section.

Survivor Benefits — Income After a Spouse Dies

When a spouse dies, the surviving spouse can receive the deceased spouse’s actual monthly benefit — including all delayed retirement credits earned. This is worth up to 100% of what the deceased spouse was receiving. It is the most financially powerful benefit in the entire Social Security system for married couples — and the most underweighted in planning decisions.

Key eligibility rules:

- Must have been married for at least 9 months before the spouse’s death (exceptions for accidental death)

- Earliest age to claim: 60 (or 50 if disabled)

- Claiming before Full Retirement Age results in a permanent reduction — down to 71.5% of the deceased spouse’s benefit if claimed at 60

- At FRA, the survivor receives 100% of the deceased spouse’s benefit

The critical difference from spousal benefits: Survivor benefits DO reflect delayed retirement credits. If the higher earner claimed at 70 and was receiving $3,200 per month, the surviving spouse receives $3,200 per month — not just 50% of PIA. This is why the higher earner delaying to 70 is not just a personal income strategy. It is a direct investment in the surviving spouse’s financial security for the rest of their life.

💡 Pro Tip: Survivor benefits and spousal benefits are completely separate programs with different rules, different amounts, and different optimal claiming strategies. Spousal benefit = 50% of PIA while both spouses are alive. Survivor benefit = 100% of the deceased spouse’s actual benefit after death. Keep these two straight — confusing them leads to costly claiming mistakes.

Why the Earnings Gap Between Spouses Changes Everything

The difference between the higher earner’s PIA and the lower earner’s own PIA is the single most important variable in married couple Social Security strategy. The larger the gap, the more the entire strategy shifts — and the more the survivor benefit becomes the central planning priority.

When the earnings gap is small: Both spouses earned similarly throughout their careers. The spousal benefit has little value because both spouses likely receive more from their own record than from a spousal top-up. Strategy focus becomes individual claiming age optimization for each spouse.

When the earnings gap is large: One spouse significantly out-earned the other, or one worked part-time or not at all. The spousal benefit becomes strategically important — and the survivor benefit becomes the most critical financial protection in the entire plan.

Here is how that plays out across three scenarios using real numbers:

Scenario A — Small Gap (both spouses have similar earnings): Spouse 1 PIA = $2,200. Spouse 2 PIA = $1,900. The spousal benefit for Spouse 2 would be 50% of $2,200 = $1,100 — less than their own benefit of $1,900. The spousal benefit has no value here. Both spouses claim their own benefit and optimize individually.

Scenario B — Moderate Gap (one spouse earned significantly more): Spouse 1 PIA = $2,800. Spouse 2 PIA = $1,100. The spousal benefit = 50% of $2,800 = $1,400 — higher than the $1,100 own benefit. Spouse 2 receives their own $1,100 plus a $300 spousal top-up = $1,400 total. Strategy now focuses on the higher earner’s claiming timing and survivor benefit maximization.

Scenario C — Large Gap (one spouse never worked or worked minimally): Spouse 1 PIA = $3,200. Spouse 2 PIA = $0. The spousal benefit = $1,600 — the only Social Security income Spouse 2 will ever receive during both their lifetimes. Spouse 2’s entire Social Security future depends entirely on Spouse 1’s record and claiming decisions.

| Higher Earner PIA | Lower Earner Own PIA | Spousal Benefit (50%) | Net Spousal Top-Up | Spousal Benefit Has Value? |

|---|---|---|---|---|

| $3,500 | $0 | $1,750 | $1,750 | Yes — full spousal |

| $3,000 | $800 | $1,500 | $700 | Yes — partial top-up |

| $2,800 | $1,100 | $1,400 | $300 | Yes — small top-up |

| $2,400 | $1,400 | $1,200 | None ($1,400 > $1,200) | No — own benefit higher |

| $2,200 | $1,900 | $1,100 | None ($1,900 > $1,100) | No — own benefit higher |

Source: Illustrative calculations based on SSA spousal benefit rules, 2026. Individual benefits vary. For educational purposes only.

The larger the earnings gap, the more critical the higher earner’s claiming strategy becomes — because it sets the floor for the surviving spouse’s income for potentially decades.

The Most Misunderstood Rule in Married Couple Social Security Planning

This one misconception causes more planning errors than anything else in this post, so we are addressing it directly before going any further.

The misconception: Many couples believe that if the higher earner delays to 70 — earning a 24% increase via Delayed Retirement Credits — the lower earner’s spousal benefit will also grow by 24%. This is incorrect.

The reality: The spousal benefit is always capped at 50% of the higher earner’s PIA — the amount at Full Retirement Age — not 50% of the higher earner’s actual claimed benefit. Delayed Retirement Credits increase the higher earner’s personal benefit, but they do not flow through to the spousal benefit.

“Michael’s PIA is $3,000. If he delays to 70, he receives $3,720 per month (a 24% increase). His wife Sandra has no work record. Her spousal benefit is 50% of Michael’s PIA of $3,000 = $1,500 per month — not 50% of $3,720. The delayed retirement credits benefit Michael personally and will eventually benefit Sandra as a survivor benefit — but not as a spousal benefit during Michael’s lifetime.”

The strategic implication: The lower-earning spouse has no financial incentive to wait for the higher earner to delay before claiming their own spousal benefit. The lower earner can claim their spousal benefit at their own Full Retirement Age for the maximum spousal amount — regardless of what the higher earner is doing. The higher earner should still delay — but for the survivor benefit, not the spousal benefit.

⚠️ Common Mistake: Waiting to claim the spousal benefit because you think it grows while the higher earner delays. It does not. The spousal benefit is permanently capped at 50% of the higher earner’s PIA. Only the survivor benefit captures the full value of delayed retirement credits — and only after the higher earner dies.

The Four Most Common Married Couple Claiming Strategies

With the foundational concepts in place, here are the four strategies used most often — with named examples and a side-by-side comparison table so you can see where your situation fits.

Strategy 1 — The 62/70 Split Strategy

Best for: Couples with a significant earnings gap; household needs some income before the higher earner turns 70

How it works: The lower-earning spouse claims their benefit at or near age 62 to provide household income. The higher-earning spouse delays to 70 to maximize both their personal benefit and the eventual survivor benefit.

“Robert (62) and Linda (60) are planning retirement. Robert is the higher earner with a PIA of $3,200; Linda’s PIA is $900. Linda claims her own benefit at 62, receiving $630 per month after reduction. Robert delays to 70, receiving $3,968 per month. Combined household income: $4,598 per month. When Robert dies, Linda immediately transitions to Robert’s $3,968 per month survivor benefit — more than six times her own early benefit.”

The “cost” of Linda’s reduced early benefit is relatively small compared to the lifetime value of Robert’s maximized survivor benefit. This is the most widely applicable strategy for couples with a meaningful earnings gap and a higher earner in good health.

Strategy 2 — Both Claim at Full Retirement Age

Best for: Couples with similar earnings records; moderate health; preference for simplicity over optimization

How it works: Both spouses claim at their individual Full Retirement Ages (67 for those born 1960 or later). Each receives 100% of their own PIA. Any spousal top-up applies at FRA automatically.

“James (66) and Carol (64) have similar earning histories — James’s PIA is $2,400 and Carol’s is $2,100. Both claim at 67. Combined household income: $4,500 per month. When one dies, the survivor receives the higher of the two benefits — $2,400 per month.”

Clean, simple, no complex coordination required. This strategy leaves some lifetime income on the table compared to the 62/70 split or both-delay strategies — but the simplicity has real value for couples who want a clear, low-maintenance plan.

Strategy 3 — Both Delay to 70

Best for: Couples in excellent health with strong family longevity; substantial retirement savings to bridge the income gap; both spouses have significant earnings records

How it works: Both spouses delay to 70, funding living expenses from retirement savings during the gap years. Both receive the maximum 24% Delayed Retirement Credit bonus.

“Patricia (62) and David (62) are both in excellent health with family histories of longevity. Patricia’s PIA is $2,600 and David’s is $2,200. They have $1.4 million in combined retirement savings. From age 62–70 they draw down from their IRA and 401(k). At 70: Patricia receives $3,224 per month; David receives $2,728 per month. Combined: $5,952 per month — guaranteed, inflation-adjusted, for life.”

The IRA and 401(k) withdrawals from 62–70 are often done in the lowest-tax years of retirement, creating a simultaneous Roth conversion opportunity that compounds the long-term benefit. If you have not yet modeled whether your savings can support this bridge period, the retirement readiness quiz Category 2 (Income Planning) and Category 1 (Savings) scores are a useful starting point.

Strategy 4 — Staggered Claiming Based on Age Difference

Best for: Couples with a meaningful age gap of three or more years between spouses

How it works: The older spouse claims first — ideally at or near FRA or 70. The younger spouse delays as long as financially feasible. Timing is driven by the age difference and each spouse’s health outlook.

“Margaret (65) is 5 years older than her husband Thomas (60). Margaret claims at 67 (her FRA), providing household income immediately. Thomas delays his own benefit until 70, continuing to work part-time. When Thomas turns 70 and claims $2,890 per month, Margaret is 75 receiving $2,300 per month from her own record. Combined: $5,190 per month. If Margaret predeceases Thomas, he would claim her survivor benefit if it exceeds his own — receiving whichever is higher.”

Strategy Comparison — Higher Earner PIA $3,000, Lower Earner PIA $1,200:

| Strategy | Higher Earner Monthly | Lower Earner Monthly | Combined Monthly | Survivor Benefit | Best For |

|---|---|---|---|---|---|

| Both claim at 62 | $2,100 | $840 | $2,940 | $2,100 | Poor health; urgent income need |

| 62/70 Split | $3,720 (at 70) | $840 (from 62) | $4,560 | $3,720 | Most couples with earnings gap |

| Both claim at FRA | $3,000 | $1,200 | $4,200 | $3,000 | Moderate health; simplicity |

| Both delay to 70 | $3,720 | $1,488 | $5,208 | $3,720 | Excellent health; strong savings |

Source: Illustrative calculations using SSA benefit adjustment formulas, 2026. For educational purposes only.

The Survivor Benefit — The Most Important Decision Most Couples Never Discuss

This section is the emotional and financial core of everything in this post. Most couples spend less time thinking about the survivor benefit than they spend choosing a cell phone plan. That needs to change.

The stark financial reality: One spouse will almost certainly outlive the other — statistically, by an average of 8–10 years for couples of similar age (longer if there is an age gap). In most married couples, the higher earner is the husband, and husbands have a shorter average life expectancy than wives. The widow scenario is therefore not a distant hypothetical. It is statistically likely — and the quality of that surviving spouse’s income depends almost entirely on one decision the higher earner makes decades earlier.

Quantifying the difference:

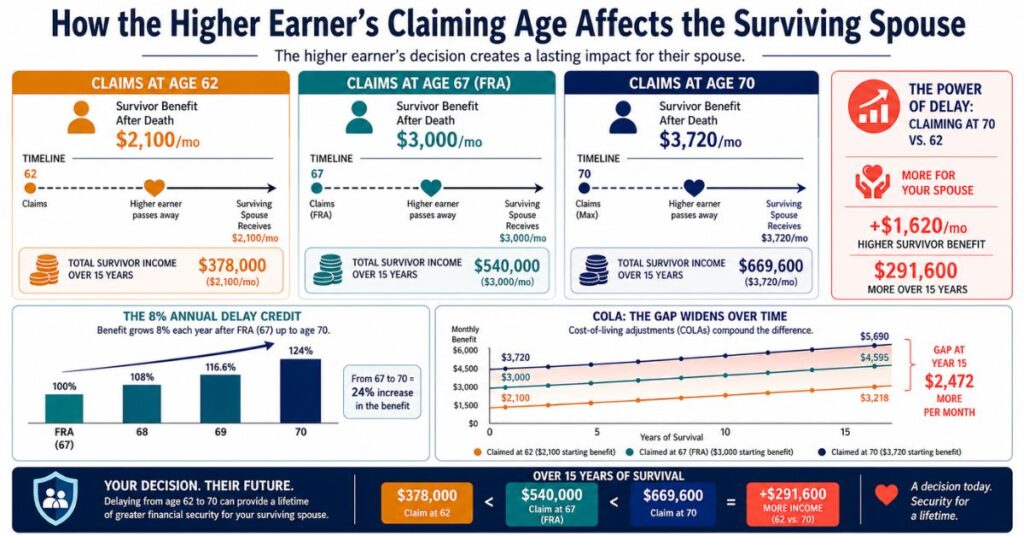

“John and Susan are both 62. John’s PIA is $3,000; Susan’s PIA is $1,100.

In Scenario A, John claims at 62 ($2,100 per month). John dies at 78. Susan, now 78, transitions to John’s survivor benefit of $2,100 per month — replacing her own $1,100 per month.

In Scenario B, John delays to 70 ($3,720 per month). John dies at 78. Susan transitions to $3,720 per month — $1,620 more per month than Scenario A.

Over Susan’s remaining 15-year life expectancy: $1,620 × 180 months = $291,600 in additional income — from one decision John made at 62.”

That $291,600 does not include COLA adjustments, which would widen the gap further every year inflation runs. It also does not account for the psychological security of knowing your income cannot be outlived, cannot decline with markets, and requires no management decisions from a grieving widow navigating finances alone.

The survivor benefit claiming rules worth knowing:

- The surviving spouse can claim the survivor benefit as early as age 60 (with a permanent reduction to 71.5%)

- If the surviving spouse is already receiving their own benefit, they can switch to the survivor benefit if it is larger

- Delayed Retirement Credits do NOT increase the survivor benefit past FRA — the survivor benefit maxes out at 100% of the deceased spouse’s benefit at FRA. Therefore, a surviving spouse should generally claim the survivor benefit at exactly their FRA — not delay it past that point

The strategic implication is simple: Delaying the higher earner’s benefit to 70 is not primarily a bet on the higher earner’s own longevity. It is fundamentally about purchasing the highest possible lifetime income stream for the surviving spouse. For a married couple where the higher earner is in reasonable health, this single decision carries more long-term financial weight than almost any other retirement choice they will make.

Age Differences Between Spouses — How They Change the Strategy

A 5-year age gap between spouses is common. It is also almost never discussed in general Social Security advice — and it changes the math considerably.

Why age differences matter: Social Security benefits are tied to individual ages, not household ages. A 5-year gap means the spouses reach Full Retirement Age 5 years apart, have different break-even horizons, and have different periods during which delay adds maximum value. The younger spouse has the most to gain from delay — more years to collect the higher benefit and more years of potential survivor benefit ahead.

Scenario A — Similar Ages (within 2 years): The 62/70 split or both-delay-to-70 strategies work essentially the same. Minor timing adjustments may be needed if one reaches FRA or 70 slightly earlier.

Scenario B — 3–5 Year Gap: The older spouse may want to claim at or near FRA to avoid too many years without any Social Security income. The younger spouse should delay as long as possible — they have the most to gain and the longest potential survivor benefit period ahead. The older spouse’s benefit provides household income that bridges the younger spouse’s delay period.

Scenario C — 6+ Year Gap: The older spouse is likely approaching FRA or even 70 before the younger spouse retires. The older spouse — especially if the higher earner — should aim for FRA or 70 to maximize what the younger spouse will eventually inherit. A significantly younger spouse may receive a survivor benefit for 20 or more years, making the older spouse’s delay decision extraordinarily valuable.

“Frank is 68 and his wife Maria is 57. Frank delays his Social Security to 70, receiving $3,840 per month. He dies at 79 — when Maria is only 68. Maria claims Frank’s full survivor benefit of $3,840 per month, which is larger than her own Social Security record. Maria collects that benefit for the rest of her life. Her 20-year survivor income from Frank’s delay decision: approximately $921,600 — before COLA adjustments.”

⚠️ Common Mistake: Assuming the younger spouse’s Social Security planning doesn’t matter because “we’ll figure it out later.” The younger spouse in a couple with a large age gap faces the greatest financial risk — the most years as a survivor, on a fixed income, with rising healthcare costs. Their planning needs more attention, not less.

Special Situations — Divorced Spouses, Widows, and Remarriage

Real life is complicated. Divorce, death, and remarriage all create Social Security situations that standard married-couple advice doesn’t cover. Here are the most common ones, handled clearly.

Divorced Spouse Benefits

You can claim Social Security benefits based on an ex-spouse’s record if you meet all of these conditions:

- Were married to the ex-spouse for at least 10 years

- Are currently unmarried

- Are at least 62 years old

- The ex-spouse is eligible for Social Security — and unlike current spouses, divorced spouses can claim based on an ex’s record without the ex having filed first, as long as both are at least 62 and have been divorced for at least 2 years

The benefit is up to 50% of the ex-spouse’s PIA — the same as a current spousal benefit. It does not affect the ex-spouse’s benefit or any current spouse’s benefit in any way. A divorced spouse can independently optimize their own claiming decision without coordinating with or even informing the ex-spouse.

Divorced surviving spouses can also claim survivor benefits on the same 10-year marriage rule if the ex-spouse dies. If you are navigating this, the retirement planning vocabulary guide defines the key terms — PIA, FRA, deemed filing, spousal supplement — that come up repeatedly in these conversations.

Widow and Widower Benefits

Key rules worth knowing:

- Can claim as early as age 60 — earlier than any other Social Security benefit

- Claiming before FRA produces a permanent reduction (down to 71.5% at age 60)

- At FRA, receives 100% of the deceased spouse’s benefit

- Delayed Retirement Credits do NOT increase the survivor benefit past FRA — the benefit maxes out at 100% at FRA, so delaying the survivor claim past FRA adds nothing

The widow/widower dual benefit strategy — one of the most underused in retirement planning:

“Helen, 62, is widowed. Her own PIA is $1,400. Her late husband’s benefit was $2,800. Helen claims her own reduced benefit at 62 ($980 per month) to generate immediate income. She does not claim the survivor benefit yet — she lets that clock run. At 67 (her FRA), she switches to the full survivor benefit of $2,800 per month — a $1,820 per month increase she locked in by waiting. If she had claimed the survivor benefit at 62 instead, she would have received only $2,002 per month permanently.”

Remarriage and Social Security

- Remarrying before age 60 disqualifies a widow or widower from claiming survivor benefits on the deceased spouse’s record

- Remarrying at or after age 60 does not disqualify — the survivor can still claim on the deceased ex-spouse’s record

- A divorced spouse who remarries loses eligibility for benefits on the ex-spouse’s record (unless that subsequent marriage also ends)

- A widow or widower who remarries at 60 or later can choose between survivor benefits from the deceased spouse and spousal benefits from the new spouse — whichever is higher

💡 Pro Tip: If you are widowed and considering remarriage before age 60, understand the survivor benefit impact before making any decisions. This is not a reason to avoid remarriage — but it is a financial reality worth factoring in. A fee-only financial advisor can model the long-term implications of remarriage timing for your specific numbers.

Building Your Couple’s Social Security Strategy — Step by Step

Here is the practical process for turning everything in this post into a concrete plan.

Step 1 — Pull both Social Security statements Both spouses create or log into their my Social Security accounts at ssa.gov/myaccount. Download both earnings records. Note the projected benefit at 62, FRA, and 70 for each spouse. Flag any years that look incorrect — especially years with multiple jobs, self-employment, or a name change.

Step 2 — Calculate the earnings gap Compare both spouses’ FRA benefits (PIAs). Determine whether the spousal benefit has value — 50% of the higher earner’s PIA versus the lower earner’s own PIA. If the spousal benefit adds value, note the maximum monthly top-up available.

Step 3 — Assess each spouse’s health and longevity outlook Have an honest conversation about health status, family longevity history, and life expectancy assumptions. For each spouse: estimate whether they are likely to live past the break-even age for delaying (approximately 80–82 for the 62 vs. 70 comparison). The higher earner’s health is especially critical — it drives the entire strategy.

Step 4 — Assess your financial bridge capacity How many years could you fund living expenses from retirement savings without any Social Security income? If you could fund 5–8 years, delaying to 70 is financially feasible. If funding even 2–3 years without Social Security is difficult, the strategy must account for that constraint. The how to set your retirement number post walks through the savings-to-expenses analysis that feeds directly into this answer.

Step 5 — Model your top two or three claiming scenarios Use the comparison table framework from the strategy section above with your actual PIA numbers. Model the survivor benefit outcome for each scenario. The free tool at opensocialsecurity.com models hundreds of combinations simultaneously — enter both spouses’ PIAs and life expectancy assumptions and it shows the optimal claiming combination in minutes.

Step 6 — Make the survivor benefit your north star After modeling all scenarios, evaluate each one through this lens: what does the surviving spouse receive, and for how long? The strategy that maximizes the survivor’s lifetime income — especially if the lower earner is significantly younger or in better health — should carry heavy weight in the final decision.

Step 7 — Decide, document, and review Write down your strategy: who claims when, from which benefit, and why. Review it annually — health changes, legislation changes, and financial circumstances change. Within five years of the first planned claiming date, consider a session with a fee-only financial advisor or Social Security specialist to stress-test the strategy with current numbers.

FAQs About Social Security for Married Couples

Can both spouses receive Social Security at the same time?

Yes — each spouse receives their own Social Security benefit independently and simultaneously. A lower-earning spouse may also receive a spousal top-up on top of their own benefit if the spousal benefit (50% of the higher earner’s PIA) exceeds their own benefit. However, a spouse cannot receive both their full own benefit and a full spousal benefit — the SSA pays the higher of the two amounts, not both in their entirety.

Does the lower-earning spouse have to wait for the higher earner to claim before getting spousal benefits?

Yes — unlike divorced spouses, a current spouse cannot claim a spousal benefit until the working spouse has filed for their own Social Security. This is the “trigger” requirement. It means that if the higher earner delays to 70, the lower earner cannot access the spousal benefit until the higher earner files — although the lower earner can claim their own retirement benefit independently at any time after age 62.

What happens to our Social Security if we divorce after 30 years of marriage?

If you divorce after 10 or more years of marriage, you retain eligibility for divorced spousal benefits (up to 50% of your ex-spouse’s PIA) and divorced survivor benefits (up to 100% of their benefit after they die) — as long as you remain unmarried. These benefits do not reduce or affect your ex-spouse’s own benefit or any benefit their current or future spouse may receive. A long marriage does not erase Social Security protection in a divorce.

Should the lower-earning spouse claim early if the higher earner is delaying to 70?

Often yes — this is the logic behind the 62/70 split strategy. The lower earner’s early claim provides household income during the years the higher earner delays. The permanent reduction on the lower earner’s benefit is relatively modest compared to the lifetime value of the higher earner’s maximized benefit and survivor benefit. Whether this is right for your household depends on the size of your earnings gap, each spouse’s health, and your financial resources during the delay period.

What if the higher earner dies before claiming Social Security?

If the higher earner dies before claiming, the surviving spouse can claim a survivor benefit based on what the deceased would have received — including any Delayed Retirement Credits earned up to the point of death. If the higher earner dies at 68 having delayed since FRA, the survivor receives the benefit that would have been paid at 68, including two years of credits. This is another argument for the higher earner to delay as long as their health permits — even partial delay captures valuable credits that flow directly to the survivor.

Is Social Security really going to be there when we retire?

This concern comes up in almost every retirement planning conversation, and it is addressed in detail in 10 Retirement Myths Debunked. The short answer: the Social Security trust fund faces a projected shortfall — not a shutdown. Even without legislative changes, payroll tax revenue is sufficient to pay approximately 77% of scheduled benefits. Congress has addressed every prior shortfall in the program’s history. Build your couple’s strategy around realistic assumptions, not worst-case fears.

The Bottom Line

You came into this post knowing Social Security was complicated for married couples. You are leaving with a clear framework for why — and exactly what to do about it.

Three things worth carrying into your planning:

- The higher earner delaying to 70 is primarily a survivor benefit strategy. It protects the spouse who will almost certainly live longer, on a guaranteed, inflation-adjusted income stream they cannot outlive. That is the north star of married couple Social Security planning.

- The spousal benefit does not grow when the higher earner delays. Only the survivor benefit captures delayed retirement credits. If you have been waiting to claim the spousal benefit thinking it is growing — it is not. The spousal benefit is capped at 50% of the higher earner’s PIA from day one.

- The 62/70 split strategy — lower earner claims early, higher earner delays to 70 — is the most widely applicable strategy for couples with an earnings gap. It provides immediate household income, maximizes the higher earner’s personal benefit, and sets the survivor benefit at its highest possible level.

If you want to make sure your Social Security plan connects to the full picture of your retirement finances, start with how Social Security is calculated to understand each spouse’s PIA in detail — then use best age to claim Social Security to model each spouse’s individual claiming decision before combining them into your couple’s strategy.

The best Social Security strategy for married couples isn’t about one spouse’s benefit — it’s about building the most secure income stream for whichever of you needs it longest.

Disclaimer: The content on RetireWealthPath.com is for informational and educational purposes only and does not constitute financial, tax, or legal advice. We are not licensed financial advisors. Social Security rules, benefit calculation methods, spousal benefit eligibility, survivor benefit amounts, and special situation provisions referenced in this article reflect 2026 SSA guidelines and are subject to change by legislation or SSA policy. All calculations, named examples, and strategy comparisons are for illustrative and educational purposes only and do not represent guaranteed outcomes. Individual and household Social Security benefits vary significantly based on each spouse’s earnings history, claiming age, health, and other personal factors. Always consult a qualified financial professional or certified Social Security specialist before making claiming decisions. Retirement planning involves risk and individual results will vary.