Delaying Social Security to 70 – Is It Worth It?

Waiting until 70 to claim Social Security is the single most recommended piece of retirement advice in America. Financial advisors say it. Government websites say it. Your financially savvy neighbor says it. But “wait until 70” is not always right — and for some people it is genuinely the wrong decision. This post gives you the honest, complete analysis.

“Delay to 70” has been repeated so many times it has become reflex — stripped of the nuance that makes any financial strategy worth following. The right claiming age is deeply personal. It depends on your health, your finances, your marital status, your tax situation, and your tolerance for risk. Delaying to 70 is genuinely optimal for some people. For others, it is the wrong move.

Before you decide whether delaying Social Security to 70 is worth it, you deserve a balanced, complete analysis: the strongest case for delaying, the strongest case against delaying, the break-even mathematics, and a personalized decision framework.

This post matters most if you are within 3–7 years of your target retirement date and are actively working through the claiming decision. If that’s you, read every section — because your claiming age is one of the most consequential financial decisions you will make.

Let’s start with the math — because the numbers are the foundation of every good claiming decision.

The Mathematics of Delaying — What Age 70 Actually Gets You

Before any strategy discussion, you need to understand exactly what waiting until 70 pays. The numbers are specific, and they matter.

The Delayed Retirement Credit

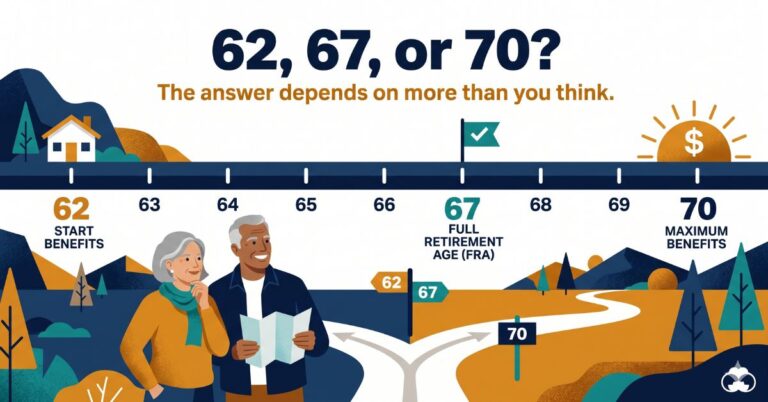

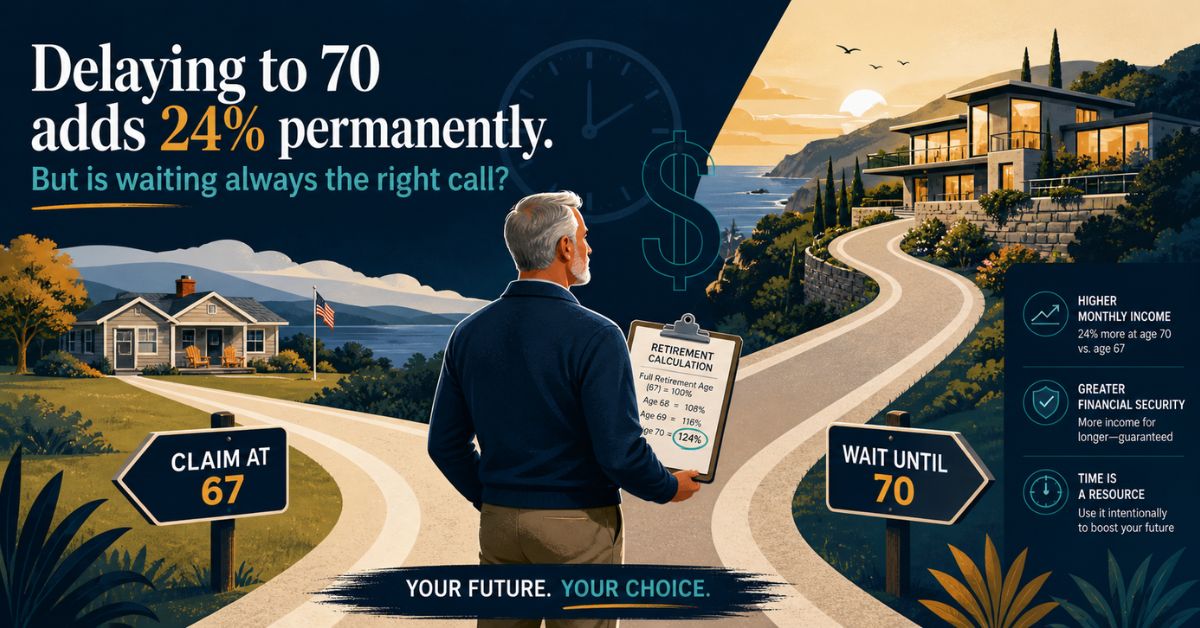

For every year you delay claiming Social Security past your Full Retirement Age (FRA) — which is 67 for anyone born in 1960 or later — your monthly benefit grows by 8% per year, or 2/3 of 1% per month.

Delay from 67 to 70 earns exactly 36 months × 2/3% = 24% more than your FRA benefit — permanently.

Two important clarifications:

- There is no benefit to waiting past 70. Delayed retirement credits stop accruing at exactly age 70. Waiting until 71 or 72 earns you nothing additional.

- The 8% annual growth is additive, not compounding. It is 8% of your Primary Insurance Amount (PIA) each year — not 8% of an already-growing number.

A Named Example With Real Numbers

Kevin’s Social Security PIA — his Full Retirement Age benefit — is $2,400/month.

- Claim at 67: $2,400/month ($28,800/year)

- Delay to 70: $2,400 × 124% = $2,976/month ($35,712/year)

- Monthly difference: $576/month

- Annual difference: $6,912/year

Every single year Kevin lives past 70, he receives $6,912 more than he would have collected by claiming at 67 — permanently, with Cost of Living Adjustments applied on top of the higher base.

The COLA Amplification Effect

This is one of the most underappreciated arguments for delay. Cost of Living Adjustments are applied as a percentage of your current benefit — which means a higher starting benefit generates larger absolute increases every year.

- 3% COLA on $2,400 = $72/month increase

- 3% COLA on $2,976 = $89.28/month increase

That $17/month difference compounds. Over 20 years of 3% annual COLAs, the gap between the two benefit streams widens substantially — the higher base amplifies every future adjustment. During high-inflation periods, this amplification becomes especially significant.

The Opportunity Cost

Delaying from 67 to 70 means forgoing 36 months of benefits. Using Kevin’s numbers: 36 × $2,400 = $86,400 in foregone FRA benefits. That is the cost of waiting — money you could have collected but didn’t.

The break-even analysis answers the key question: how long must Kevin live past 70 to recoup that $86,400 through the higher monthly benefit?

The Mathematics of Delay at a Glance

Kevin’s example — PIA = $2,400/month

| Claiming Age | Monthly Benefit | Annual Benefit | Foregone vs. FRA | Simple Break-Even |

|---|---|---|---|---|

| 62 | $1,680 | $20,160 | — | — |

| 67 (FRA) | $2,400 | $28,800 | Baseline | Baseline |

| 68 | $2,592 | $31,104 | $28,800 | ~Age 80 |

| 69 | $2,784 | $33,408 | $57,600 | ~Age 82 |

| 70 | $2,976 | $35,712 | $86,400 | ~Age 82–83 |

Illustrative calculations using SSA delayed retirement credit formula. Break-even assumes constant benefit, no COLA adjustments. For educational purposes only.

The pure mathematics of delaying to 70 are compelling — a 24% permanent increase, COLA-amplified for life. Whether those mathematics apply to your situation depends entirely on how long you will live to collect them.

The Break-Even Analysis — The Number That Drives Everything

The break-even age is the single most important concept in the delay-to-70 decision. Understand it completely.

What Is the Break-Even Age?

The break-even age is the point at which your total lifetime benefits from waiting until 70 equal total lifetime benefits from claiming at FRA.

- Past break-even: the delay strategy has produced more total lifetime income

- Before break-even: the person who claimed at FRA has collected more total income

Calculating the Break-Even

Using Kevin’s numbers ($2,400 PIA):

- Monthly difference between age 70 and FRA claims: $576/month

- Total foregone FRA benefits during 3-year delay: $2,400 × 36 = $86,400

- Break-even: $86,400 ÷ $576 = 150 months after age 70 = approximately age 82–83

In plain English: if Kevin lives past 82–83, waiting until 70 produces more lifetime income. If he dies before 82–83, claiming at FRA would have produced more.

The break-even is essentially a bet on whether you will outlive the median American. The median life expectancy for a 67-year-old American man is approximately 84; for a woman, approximately 86. On a statistical basis, most people who are currently healthy at 67 will outlive the break-even age.

What If Kevin Invests Instead?

A more complete analysis asks: what if Kevin claimed at FRA and invested the $2,400/month he received from 67–70?

At a 5% annual return, investing $2,400/month for 36 months grows to approximately $93,000 by age 70. That invested capital shifts the effective break-even higher — typically by 1–2 years. At a 7% return, the break-even moves to approximately 84–85.

This matters for the “invest the difference” argument explored in the counterarguments below.

Break-Even Comparison by Delay Length

| Comparison | Monthly Gain | Foregone Benefits | Simple Break-Even | With 5% Investment Return |

|---|---|---|---|---|

| Age 67 → 68 | $192/mo | $28,800 | ~Age 80 | ~Age 82 |

| Age 67 → 69 | $384/mo | $57,600 | ~Age 82 | ~Age 84 |

| Age 67 → 70 | $576/mo | $86,400 | ~Age 82–83 | ~Age 84–85 |

| Age 62 → 70 | $1,296/mo | $241,920 | ~Age 80–81 | ~Age 82–83 |

Illustrative calculations. Investment return scenario assumes 5% annual return on foregone benefits. For educational purposes only.

The Critical Limitation of Break-Even Analysis

Break-even math treats every dollar as equal regardless of timing. But a dollar of Social Security income received at 67 — during your active, healthy retirement years — may have far more lifestyle value than the same dollar at 82.

Retirement spending research consistently identifies a “go-go phase” (ages 62–75) when retirees spend the most on travel, leisure, and experiences. The simple break-even calculation ignores this temporal value — and for some people, that omission is significant.

The Strongest Case FOR Delaying to 70 — Five Compelling Arguments

These are genuine, rigorous arguments — not promotional talking points.

Argument 1: Longevity Risk Is the Greatest Retirement Threat

The most dangerous financial event in retirement is not a market crash. It is outliving your money.

Social Security is the only source of retirement income that is guaranteed for life, inflation-adjusted, and literally cannot be outlived. Delaying to 70 maximizes this guarantee — the higher benefit creates a larger floor of income that continues regardless of how long you live.

A 70-year-old woman today has a 50% chance of living to 88 and a meaningful chance of living into her mid-90s. For the 15–25% of retirees who live into their late 80s and 90s, the lifetime income advantage of delaying is not marginal — it is enormous.

Delaying to 70 is fundamentally an insurance purchase against extreme longevity. And like all insurance, it becomes more valuable the more you need it.

Argument 2: The 8% Return Is Essentially Unbeatable on a Risk-Adjusted Basis

The 8% annual delayed retirement credit is a government-guaranteed, inflation-adjusted return that requires zero investment risk.

Compare to 2026 alternatives: 10-year Treasury bonds yield approximately 4–5%; a diversified bond portfolio yields similarly; even a moderate-risk balanced portfolio averages 6–7% with significant volatility. The 8% guaranteed, inflation-adjusted return available through Social Security delay beats virtually every comparable risk-free investment available today.

For risk-averse retirees who have already secured their portfolio, the Social Security delay is the single best “investment” available.

Argument 3: Married Couples Should Delay for the Survivor Benefit

This is often the most financially significant argument for delay — and the most overlooked.

The higher earner’s Social Security benefit becomes the surviving spouse’s income for potentially decades after death. Delaying the higher earner’s benefit to 70 is not just about personal income — it is about purchasing the maximum possible inflation-adjusted survivor income for a spouse who will likely outlive you.

For a married couple where the higher earner is a man (statistically lower life expectancy) and the lower earner is a woman (statistically higher life expectancy), the delay decision is primarily about protecting her income for the decades after his death.

To understand this in full detail, read our Social Security for married couples strategy guide — the survivor benefit impact is explored there with complete examples and calculations.

Consider Raymond’s situation:

Raymond’s personal break-even for delaying to 70 is age 83 — and he is not certain he will live that long given his family history. But Raymond’s wife Susan is 5 years younger and in excellent health. If Raymond dies at 78, Susan will receive his benefit as a survivor benefit for potentially 15–20 more years. Raymond’s delay from 67 to 70 adds $576/month — and that $576/month flows to Susan as a survivor benefit for potentially 20 years. $576 × 240 months = $138,240 in additional survivor income. Raymond delays.

For a deep dive on the mechanics behind this, see our full post on Social Security survivor benefits explained.

Argument 4: Portfolio Withdrawal Sequencing Benefits

Using portfolio withdrawals to bridge from 67 to 70 — rather than claiming Social Security early — often produces better long-term outcomes on multiple dimensions simultaneously.

During the bridge period, retirees withdraw from pre-tax accounts (401k, traditional IRA) during the lowest-income tax years of retirement, before Required Minimum Distributions begin at age 73. This serves double duty: funding living expenses AND doing implicit Roth conversion work by drawing down pre-tax balances before mandatory distributions kick in.

Lower pre-tax balances at 73 = lower RMDs = lower taxable income = lower Medicare IRMAA premiums.

Argument 5: Cognitive Decline and Late-Life Simplicity

Research consistently shows that financial decision-making ability declines meaningfully after age 80 for a significant portion of the population.

A higher guaranteed income from Social Security simplifies late-life finances — reducing dependence on portfolio management, withdrawal decisions, and active financial oversight. For retirees who worry about cognitive decline affecting their ability to manage investments in their 80s, maximizing the guaranteed SS income floor creates a more robust, less actively managed financial structure.

This argument is often dismissed in formal financial planning — but it is genuinely important for real-world retirement security.

The Strongest Case AGAINST Delaying to 70 — Five Legitimate Counterarguments

These are real, legitimate reasons not to delay — not straw men. Intellectual honesty requires presenting them with the same rigor as the affirmative case.

Counterargument 1: Health and Family History Make the Break-Even Unreachable

If you have a serious health condition, chronic illness, or strong family history of early death, the break-even analysis shifts decisively against delay.

A retiree who genuinely expects to live to 75–78 will almost certainly collect more lifetime income by claiming at 62 or 67 than by waiting until 70. Delaying is a bet on longevity — and if your honest assessment of your longevity is below average, the bet does not pay off.

This is not pessimistic — it is rational financial planning. Claiming earlier and spending that income on quality of life during your healthier years may be the genuinely correct decision. No financial advisor should reflexively recommend delay without explicitly asking about the client’s health.

Counterargument 2: Immediate Financial Need Cannot Wait

Many Americans approaching retirement face genuine financial pressure — reduced income, high debt, unexpected expenses, or job loss.

For someone laid off at 63 with minimal savings who cannot find re-employment, claiming Social Security at 62 or 63 may not be a suboptimal choice — it may be the only viable option. The theoretical ideal of delaying to 70 is only available to people who have the financial resources to bridge the gap. That is a privilege, not a universal position.

“Delay to 70” advice that ignores real financial constraints is not helpful — it is disconnected from the reality many retirees face.

Counterargument 3: The Portfolio Bridge Has Real Costs and Risks

Funding a 3-year bridge from 67 to 70 by withdrawing from retirement accounts has genuine costs:

- Withdrawing $2,400/month for 36 months = $86,400 removed from the portfolio, plus the lost growth on that capital

- In a down market, forced selling of assets to fund bridge income is precisely the sequence of returns risk that permanently damages retirement plans

- For retirees with limited portfolio assets (under $400,000–$500,000), the bridge cost is not trivial — it can represent 15–20% of total retirement savings

Delaying makes strong financial sense when bridge funding is easy. It makes far less sense when the bridge itself strains the portfolio.

Counterargument 4: The Money Has More Value in Your Active Years

A dollar of Social Security income at 67 is worth more in lifestyle terms than a dollar at 82.

Research on retirement spending consistently identifies the “retirement spending smile” — highest spending in the early go-go years (ages 62–75), lower spending in the slow-go middle years (75–85), and higher again late (ages 85+, dominated by healthcare costs).

An extra $576/month received during the active, travel-and-leisure years of 67–70 has greater lifestyle impact than the same amount received at 82 when health and mobility may be significantly reduced. The pure break-even calculation ignores the temporal utility of money — and for some retirees, front-loading income during their healthiest years is the genuinely correct preference.

Counterargument 5: Single Retirees With No Dependents Have a Lower-Stakes Decision

The single most compelling argument for delay — the survivor benefit for a spouse — does not apply to single retirees with no dependents.

Without a spouse, the delay decision is purely personal: does the higher monthly benefit justify the wait, given your specific health and financial situation? For a single retiree in moderate health with limited savings, claiming earlier and reducing portfolio withdrawals during the same period may produce equivalent or better outcomes.

Single retirees should run a pure personal break-even analysis without the survivor benefit weight pulling the calculation toward delay. If you are divorced and evaluating your options, our divorced spouse Social Security rights guide covers the additional benefit options available to you.

Common Mistake: Treating “delay to 70” as universally correct without examining your own specific situation. The recommendation to delay is sound for many people — but it is built on assumptions about longevity, financial resources, marital status, and portfolio strength that may not apply to you. The correct answer for you depends entirely on your facts — not on what works for the average American.

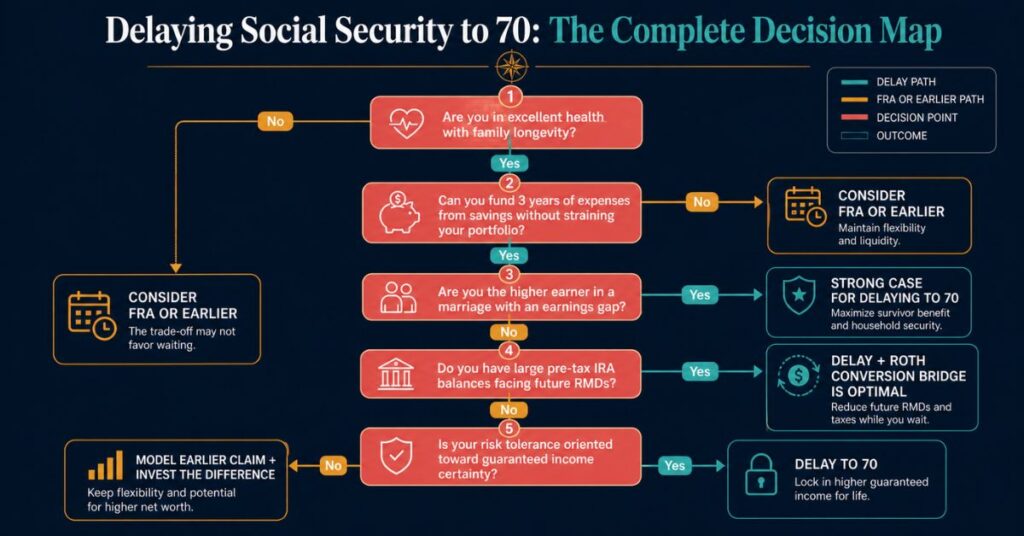

The Personalized Decision Framework — Finding YOUR Answer

After presenting both sides with full rigor, the practical question is: which path is right for you? Here is a clear, five-factor decision framework.

The Five Factors That Determine the Right Answer

Factor 1 — Health and Longevity Expectation

- Excellent health, family history of longevity (parents/siblings to 85+), no serious chronic conditions → Strong case for delay to 70

- Average health, no major concerns, neutral family history → FRA to 68–69 range is often optimal

- Serious health condition, family history of early death, significant chronic illness → Earlier claiming is often correct

Factor 2 — Financial Bridge Capacity

- Can fund 3 years of expenses from portfolio without straining it (portfolio $500K+) → Delay to 70 is financially feasible

- Moderate portfolio — bridge possible but tight → Consider 68–69 as a compromise

- Limited savings, bridge would represent 15–20%+ of total portfolio → Claim at or near FRA to reduce portfolio risk

Factor 3 — Marital Status and Earnings Disparity

- Married, higher earner, significant earnings gap with spouse → Strong case for delay — survivor benefit is the dominant factor

- Married, similar earnings → Model survivor benefit for each scenario

- Single with no dependents → Pure personal break-even decision — survivor benefit is not a factor

Factor 4 — Tax Situation and Portfolio Composition

- Large pre-tax IRA/401k balances facing large future RMDs → Delay SS while doing Roth conversions — tax efficiency amplifies the delay benefit significantly

- Already Roth-heavy or minimal pre-tax balances → Tax efficiency argument for delay is weaker — evaluate on other factors

- High-income retiree concerned about Medicare IRMAA premiums → SS delay may reduce IRMAA exposure — model carefully

Factor 5 — Risk Tolerance and Peace of Mind

- Risk-averse retiree who values guaranteed income certainty above all → Delay provides the highest guaranteed floor — strong fit

- Risk-tolerant retiree comfortable managing a portfolio → Earlier claim + invested difference may be competitive — model both scenarios

- Retiree who fears outliving their money → Delay is the longevity insurance that directly addresses this concern

Personalized Delay Decision Matrix

| Health | Bridge Capacity | Marital Status | Recommended Claiming Age | Primary Reason |

|---|---|---|---|---|

| Excellent | Strong | Married — earnings gap | 70 | Survivor benefit + longevity |

| Excellent | Strong | Single | 69–70 | Longevity odds favor delay |

| Excellent | Moderate | Married — earnings gap | 69–70 | Survivor benefit — delay as long as feasible |

| Good | Strong | Married — similar earnings | 67–69 | Model survivor benefit for both spouses |

| Good | Moderate | Single | 67–68 | Break-even within life expectancy range |

| Fair | Any | Any | 65–67 | Health uncertainty; claim near FRA |

| Poor | Any | Any | 62–64 | Break-even likely unreachable |

| Any | Cannot bridge | Any | FRA or earlier | Financial need overrides delay strategy |

RetireWealthPath.com analytical framework based on SSA benefit rules and retirement planning principles. For educational purposes only. Individual situations vary.

To understand where you land on this matrix, first confirm how Social Security is calculated and establish your exact PIA — then you have the personal numbers needed to run this framework. For a complete comparison of all claiming ages side by side, our best age to claim Social Security guide walks through every scenario in detail.

The Portfolio Bridge Strategy — How to Fund the Gap from 67 to 70

For readers who decide delay is right for them, the next question is practical: how do you fund living expenses from 67 to 70 without Social Security income?

What the Bridge Strategy Involves

The bridge strategy means deliberately withdrawing from retirement accounts (401k, traditional IRA, brokerage) from ages 67–70 to fund living expenses — intentionally forgoing Social Security during this period to earn the delayed retirement credits.

The bridge period is typically 36 months (3 years from FRA to 70), though many retirees bridge from their actual retirement date, which may be earlier than FRA.

Calculating Your Bridge Amount

Monthly bridge amount = Monthly living expenses − Other income sources (pension, rental income, part-time work, dividends)

If other income covers $2,000/month and your expenses are $4,000/month, the bridge draw-down is $2,000/month from retirement accounts — $72,000 total over 36 months.

If you are still working part-time during the bridge period, our guide on how work in retirement affects Social Security benefits explains how earnings can interact with your claiming decision.

The Tax Efficiency Bonus

Withdrawing from a traditional IRA or 401k between ages 67–70 — before RMDs begin at 73 — often occurs in the lowest-income tax bracket of your entire retirement.

Without Social Security income and without mandatory distributions, many retirees can withdraw $30,000–$60,000/year from pre-tax accounts while remaining in the 12% federal bracket. This is the prime Roth conversion window: converting additional IRA funds to Roth during this period reduces future mandatory distributions and their associated taxes for decades to come.

The bridge strategy and the Roth conversion strategy are, in practice, the same action — drawing from pre-tax accounts before RMDs while in a lower-tax environment.

When the Bridge Is Too Expensive

If the bridge requires withdrawing more than 5–6% of your portfolio annually, the sequence-of-returns risk during the bridge period may offset the value of the higher Social Security income.

A practical rule of thumb: if the 3-year bridge total exceeds 15–20% of your total retirement portfolio, delay may not be financially prudent.

- $72,000 bridge on a $400,000 portfolio = 18% → borderline; re-evaluate

- $72,000 bridge on a $700,000 portfolio = 10% → more comfortable

Three Real-World Scenarios — Delay vs. Don’t Delay

Numbers become real when they are attached to people. Here are three complete scenarios mapped to the framework above.

Scenario 1: The Case Where Delay to 70 Is Clearly Right

Eleanor, 67, just retired after 35 years as a nurse. Her PIA is $2,600. She is in excellent health — she runs four days a week, her mother lived to 94, and her doctor calls her “10 years younger than her age.” Eleanor is married to Thomas, 64, whose PIA is $1,100. They have $820,000 in combined retirement savings.

Eleanor delays to 70. From 67–70, she and Thomas withdraw approximately $2,200/month from their traditional IRA to bridge the income gap — and execute Roth conversions of $25,000/year during this period, staying in the 12% bracket.

At 70, Eleanor claims $3,224/month ($2,600 × 124%). Thomas claims at 65 — his own reduced benefit plus a spousal top-up to 50% of Eleanor’s PIA ($1,300). Combined household Social Security income: $4,224/month — guaranteed, inflation-adjusted, for life.

If Eleanor dies at 88, Thomas (then 85) transitions to her $3,224/month survivor benefit permanently. The delay decision was correct on every dimension: personal income, survivor protection, tax efficiency, and longevity coverage.

Factors that drove Eleanor’s decision: Excellent health, strong longevity history, large portfolio (bridge is only 10% of savings), married with an earnings gap, large pre-tax IRA balance ideal for Roth conversions.

Scenario 2: The Case Where Delay to 70 Is Clearly Wrong

Gerald, 65, worked in manufacturing for 30 years before being laid off at 63. He has $140,000 in a 401k and no pension. His PIA is $1,800. Gerald has Type 2 diabetes, a history of cardiac issues, and his father died at 71 and his brother at 69. Gerald is single.

Gerald’s break-even for delaying from FRA to 70 is approximately age 83 — an age he has meaningful reason to believe he will not reach. His $140,000 portfolio cannot sustain a 3-year bridge without serious risk.

Gerald claims at 63, shortly after his layoff, receiving approximately $1,350/month. This income, combined with part-time work, allows him to preserve his 401k for later needs. The decision is correct: his health and financial situation both argue against delay, and the survivor benefit argument is irrelevant because he is single.

Factors that drove Gerald’s decision: Serious health conditions, family history of early death, limited portfolio (bridge would require 60%+ of savings), single with no dependents, layoff made immediate income necessary.

Scenario 3: The Genuinely Close Case

Diane, 67, is widowed and in average health. Her PIA is $1,900. She is already receiving her late husband’s survivor benefit of $2,800/month — the higher of the two available benefits. Her own benefit at 70 would be $2,356.

Diane’s own benefit at any claiming age is less than the $2,800 survivor benefit she is already receiving. Delaying her own benefit to 70 would add nothing — she would still receive the higher survivor benefit regardless.

Diane has no reason to delay. She continues receiving the survivor benefit and focuses on managing her $380,000 IRA efficiently. The delay-to-70 question is simply irrelevant — her survivor benefit dominates at every claiming age.

The lesson from Diane’s scenario: Every claiming decision must be evaluated with the full picture of all available benefits. For complete details on survivor benefit mechanics, see Social Security survivor benefits explained.

Common Mistakes People Make on the Delay Decision

Specific, actionable errors — now that you have the framework to avoid them.

Mistake 1 — Using Average Life Expectancy Instead of Your Own The delay decision should be based on your honest assessment of your health and family history — not national averages. Average life expectancy includes everyone: smokers, people with serious chronic illness, people in poor health. If you are in excellent health, your personal life expectancy likely exceeds the average. Use your own picture.

Mistake 2 — Ignoring the Survivor Benefit in the Calculation Married couples who evaluate the delay decision purely on personal break-even analysis systematically undervalue delaying. The survivor benefit adds a second, often more financially significant dimension that the simple break-even calculation completely misses.

Mistake 3 — Conflating Retirement Date With Claiming Date The decision to retire and the decision to claim Social Security are completely independent. You can retire at 63 and claim at 70. Many people automatically claim when they retire — not realizing they have a choice. This conflation can cost years of delayed retirement credits.

Mistake 4 — Failing to Account for Taxes in the Break-Even The simple break-even compares gross benefits. But Social Security is partially taxable — and the rate depends on your other income. A retiree who claims early may have 85% of their SS income taxed at ordinary rates, while a retiree who delays and uses a Roth conversion bridge may face significantly lower overall taxation. The after-tax break-even is often more favorable to delay than the pre-tax version.

Mistake 5 — Assuming the Trust Fund Shortfall Makes SS Unreliable Some people claim early out of fear that Social Security will run out. The SSA Trustees Report makes clear that even under worst-case projections without legislative action, Social Security is projected to pay approximately 77% of scheduled benefits from ongoing payroll tax revenue. Claiming at 62 out of solvency fear typically costs far more in foregone lifetime income than the worst-case projected reduction.

Mistake 6 — Never Modeling the Decision With Your Actual Numbers The most common mistake of all. Making the delay decision based on general advice instead of personal numbers is how people get this wrong. Your PIA, your break-even age, your portfolio bridge capacity, your survivor benefit impact — these are specific, calculable numbers. The correct decision for you requires your numbers, not what works for the average American.

Frequently Asked Questions

If I claim at 67 and invest the $2,400/month in the stock market, won’t I likely beat the delay strategy?

Possibly — depending on the return achieved and how long you live. At a 7% average annual return, investing the FRA benefit from 67–70 and continuing to invest the monthly difference does shift the effective break-even to approximately 84–85. But this comparison ignores two critical factors: investment returns are not guaranteed (the 8% delayed retirement credit is), and it does not account for the survivor benefit impact for married couples. For single retirees with strong risk tolerance and confidence in their investment returns, this is a legitimate counterargument. For married couples and risk-averse retirees, the guaranteed return with survivor benefit is very difficult to beat.

What if Social Security reduces benefits before I reach 70? Does that change the analysis?

The trust fund shortfall creates real uncertainty — but it does not necessarily argue for claiming early. If benefits are reduced uniformly (the most likely legislative outcome), the reduction applies equally to all claiming ages, and the relative advantage of delaying remains intact. A 20% across-the-board cut reduces a $2,976 benefit to $2,381 — and reduces a $2,400 FRA benefit to $1,920. The delayed benefit is still 24% higher. Only a scenario where reductions specifically target higher benefits (politically unlikely) would change the relative advantage of delay.

I am 68 and already claimed at 67. Can I undo that and restart at 70?

Partially. If you claimed less than 12 months ago, you can withdraw your application (Form SSA-521), repay all benefits received, and restart the clock. After 12 months, the withdrawal option closes. However, at your Full Retirement Age you can voluntarily suspend your benefits — stopping payments without repaying what you have already received — and earn delayed retirement credits until age 70. Full guidance on the suspension option is available at ssa.gov/benefits/retirement/planner/suspend.html. Suspending at 68 and restarting at 70 earns 2 years of credits — a 16% total increase — meaningfully improving your benefit even if you missed the optimal delay window.

Does delaying to 70 affect my Medicare enrollment?

No — Medicare eligibility begins at 65 regardless of when you claim Social Security. If you are receiving Social Security when you turn 65, Medicare enrollment is automatic. If you are delaying SS, you must proactively enroll during your 7-month initial enrollment window around your 65th birthday. Failing to enroll on time results in permanent premium penalties for Medicare Part B and Part D. Do not conflate delaying Social Security with delaying Medicare — they are completely independent decisions.

My financial advisor says to always wait until 70. Should I just follow that advice?

“Always wait until 70” is a reasonable default heuristic for most people in good health — but it is not a universal truth. A good financial advisor should ask about your health history, family longevity, marital situation, portfolio bridge capacity, and tax situation before making a recommendation. If your advisor is recommending delay without examining these specific factors, ask them to walk through your personal break-even analysis and model the survivor benefit impact. The right answer for you requires your numbers — not a blanket rule.

The Bottom Line

Return to where we started: “delay to 70” is widely recommended — but it is not universally correct.

Here are the three most important takeaways from everything above:

- Delaying to 70 adds 24% permanently, COLA-amplified for life, with an 8% guaranteed annual return that beats nearly every risk-free alternative available in 2026. For the right person, it is a genuinely powerful financial move.

- The break-even age of approximately 82–83 means delay is correct for people with good health and reasonable longevity expectations — and potentially wrong for those with serious health concerns, immediate financial needs, or limited bridge capacity.

- The survivor benefit is the single most compelling argument for delay in married couples — it often matters more than the personal break-even calculation, and it is the factor most commonly overlooked in casual analysis.

Ready to model your personal decision? Start with our guide on how Social Security is calculated to confirm your exact PIA — then use our best age to claim Social Security analysis to run the full comparison across all claiming ages for your specific situation. Finally, check your retirement readiness to see how your claiming strategy fits into your complete retirement picture.

Delaying to 70 is worth it — for the right person, at the right time, with the right financial foundation. The goal of this post was to help you know which of those people you are.

Disclaimer: All content on RetireWealthPath.com is for informational and educational purposes only and does not constitute financial, tax, or legal advice. Benefit percentages, break-even calculations, and Social Security rules reflect 2026 guidelines and are subject to change. All examples and named individuals (including Kevin, Eleanor, Thomas, Gerald, Diane, and Raymond) are illustrative and do not represent specific individuals. Always consult a qualified financial professional before making Social Security claiming decisions.