Social Security Survivor Benefits Explained [2026 Guide]

When a spouse dies, the financial decisions that follow are among the most consequential a person will ever make — and they must be made during the hardest weeks of their life. Social Security survivor benefits exist specifically to protect surviving family members. Understanding them before you need them — or exactly when you need them — can make an enormous difference.

This guide will walk you through everything you need to know about Social Security survivor benefits explained in plain language: who qualifies, how much you can receive, when to claim, and the strategic decisions that will affect your income for the rest of your life.

One thing worth knowing right away: survivor benefits cover far more people than most realize. Beyond widows and widowers, they extend to children, divorced spouses, and in some cases dependent parents. Many eligible people never claim what they are fully entitled to receive. That is something we want to change.

Let’s begin with who qualifies — because the eligibility rules are broader than most people realize, and knowing them is the first step toward financial security after loss.

Who Qualifies for Social Security Survivor Benefits — The Complete Eligibility Map

Widows and Widowers

To qualify for survivor benefits as a widow or widower, you must have been legally married to the deceased worker, and the marriage must have lasted at least 9 months immediately before their death. Exceptions apply if the death was accidental, if the worker was in uniformed service and died in the line of duty, or if you had a child together born of the marriage.

Age requirements:

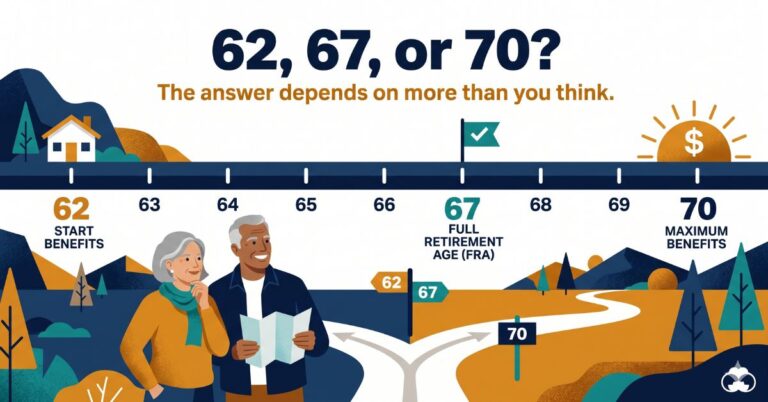

- Full survivor benefit is available at your own Full Retirement Age (FRA) — currently 67 for anyone born in 1960 or later

- Reduced survivor benefit is available as early as age 60

- Disabled widows and widowers can claim as early as age 50

- No age minimum applies if you are caring for the deceased worker’s child who is under 16 or disabled

Remarriage rules matter: Remarrying before age 60 disqualifies you from survivor benefits on your deceased spouse’s record. Remarrying at 60 or later does not affect your eligibility at all. And if a later marriage ends — by death, divorce, or annulment — eligibility on the earlier spouse’s record may be restored.

Catherine’s story: Catherine, 61, lost her husband Gerald when he was 63. They had been married 28 years. Catherine claimed a reduced survivor benefit at 61 — receiving approximately 82.9% of Gerald’s full benefit. This provided meaningful income during the years before she could access her own retirement benefit or Medicare.

Divorced Surviving Spouses

A divorced spouse can qualify for survivor benefits if the marriage lasted at least 10 years. You must currently be unmarried — or have remarried at or after age 60. The divorce itself does not disqualify you. Only the length of the marriage and your current marital status matter.

The benefit amount is the same as for a current widow or widower — up to 100% of the deceased ex-spouse’s benefit at your FRA. Importantly, your benefit does not reduce or affect what any current spouse or other survivors receive. The SSA processes divorced survivor claims independently, with no notification to other family members.

Children

Eligible children receive up to 75% of the deceased worker’s Primary Insurance Amount (PIA):

- Unmarried children under age 18

- Unmarried children under 19 if still enrolled full-time in high school

- Unmarried children of any age who were disabled before age 22 — these individuals can receive survivor benefits for life

Biological children, adopted children, stepchildren who were financially dependent on the deceased, and in certain cases grandchildren (when the grandparent was the primary caregiver) all qualify.

Dependent Parents of the Deceased Worker

This is the least-known survivor benefit in the entire program. A parent who was financially dependent on the deceased worker for at least half of their support — and who is age 62 or older — may qualify:

- 82.5% of the worker’s PIA if one parent qualifies

- 75% each (150% combined) if both parents qualify

Pro Tip: Many families don’t know dependent parents can qualify. If an elderly parent relied financially on a child who died, they should contact the SSA immediately — regardless of whether they already receive their own Social Security. The additional benefit could be meaningful for the rest of their life.

How Much Is the Survivor Benefit — Calculating Your Amount

The survivor benefit is based on what the deceased worker was receiving — or would have received — at the time of death, including any delayed retirement credits they had earned.

- If the deceased had not yet claimed: the survivor benefit is based on their PIA (their benefit at FRA)

- If the deceased claimed early: the survivor receives the greater of the reduced amount the worker was receiving OR 82.5% of the deceased’s full PIA — a floor provision that protects survivors

- If the deceased delayed past FRA: the survivor benefit reflects the higher amount, including all delayed retirement credits earned

The survivor’s own claiming age determines the percentage received:

| Survivor Claiming Age | % of Deceased’s Benefit |

|---|---|

| 60 | 71.5% |

| 61 | 75.6% |

| 62 | 79.6% |

| 63 | 83.7% |

| 64 | 87.8% |

| 65 | 91.9% |

| 66 | 95.9% |

| 67 (FRA) | 100% |

| Disabled widow/widower at 50 | 71.5% |

Source: Social Security Administration survivor benefit reduction schedule, 2026. FRA for survivors born 1962 or later is 67.

Harold and Dorothy’s story: Harold delayed his Social Security to age 70 and was receiving $3,840/month when he died at 72. His wife Dorothy was 65. Dorothy’s own benefit would have been $1,200/month at her FRA of 67. She waited until 67 to claim the full survivor benefit — receiving $3,840/month for the rest of her life. Harold’s decision to delay directly and permanently secured Dorothy’s financial future.

Don’t forget the lump-sum death payment. A one-time payment of $255 is available to the surviving spouse or eligible children. Though the amount has not changed since 1954, it must still be claimed — the SSA does not pay it automatically. Apply within 2 years of the worker’s death.

The Family Maximum Benefit — When Multiple Survivors Are Involved

When multiple family members claim benefits on the same worker’s record, the total cannot exceed the Family Maximum Benefit (FMB) — typically between 150% and 180% of the deceased’s PIA, depending on their earnings history.

If combined survivor benefits exceed the FMB, each survivor’s benefit is proportionally reduced until the total equals the cap.

Victor’s family: Victor died at 52, leaving his wife Angela (48) and three children ages 8, 11, and 14. His PIA was $2,400 and his FMB was approximately $4,200. Each family member was entitled to up to 75% of $2,400 ($1,800/month). Combined, that totaled $7,200 — far above the FMB. Each benefit was reduced proportionally to $1,050/month. As each child aged out at 18, the remaining recipients’ benefits increased, up to their individual maximums.

Common Mistake: Never assume all family members automatically receive the full benefit percentage. If multiple people are claiming on the same record at the same time, the FMB cap will reduce each person’s amount proportionally. Ask the SSA to explain the FMB calculation for your specific family situation before making any decisions.

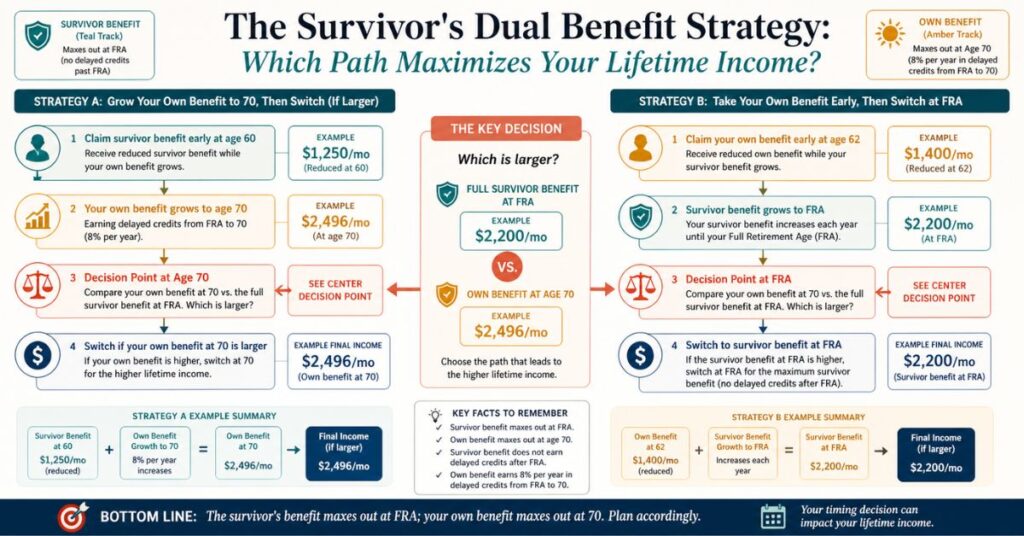

The Survivor’s Most Important Strategic Decision — Own Benefit vs. Survivor Benefit

This is where most survivors leave significant money on the table.

If you have your own Social Security work record, you have a powerful option that most people never fully understand: you can claim one benefit first and switch to the other later. To understand the full claiming picture, it helps to first read how Social Security is calculated — particularly how your PIA is determined.

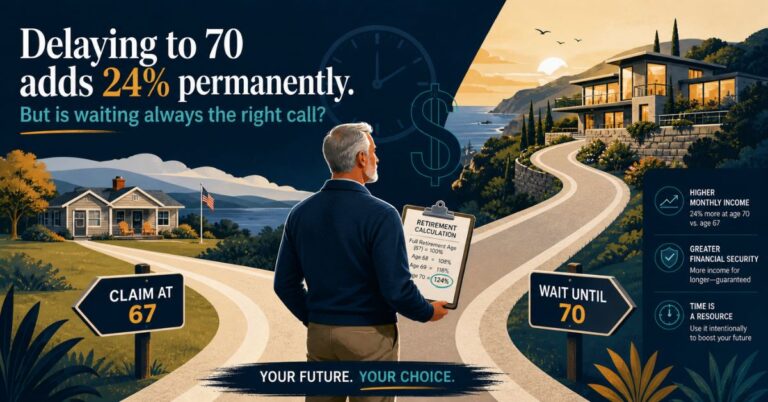

Why this matters: Your own retirement benefit grows by 8% per year from FRA to age 70 due to delayed retirement credits. The survivor benefit, by contrast, does not earn delayed retirement credits past FRA. It maxes out at FRA. This asymmetry creates two distinct strategies.

Strategy A — When your own benefit at 70 will be larger than the full survivor benefit:

- At age 60, claim the reduced survivor benefit to generate income

- Let your own retirement benefit grow untouched toward age 70

- At 70, switch to your own retirement benefit — which has grown 24% beyond your FRA amount

- Receive the higher of the two benefits for the rest of your life

Strategy B — When the full survivor benefit at FRA will always be larger:

- At age 62, claim your own reduced retirement benefit for immediate income

- At FRA (67), switch to the full survivor benefit — which is likely significantly larger

- Receive the full survivor benefit for the rest of your life

Margaret’s story: Margaret, 60, was widowed. Her late husband Paul’s survivor benefit at her FRA was $3,200/month. Her own benefit at 70 would have been just $1,984/month. Since the survivor benefit was larger, Margaret used Strategy B: she claimed her own reduced benefit at 62 ($1,120/month) for immediate income, then switched to Paul’s full survivor benefit at 67 ($3,200/month) — a $2,080/month permanent increase.

The rule of thumb: survivor benefit maxes out at FRA. Your own benefit maxes out at 70. Compare both numbers before committing to any claiming sequence. For a deeper look at how your own benefit interacts with these decisions, see our guide on the best age to claim Social Security.

When Survivor Benefits Begin — Timing, Application, and Retroactive Claims

Apply promptly. Survivor benefits generally cannot be paid for months before the application is filed — with one important exception. Survivors can receive up to 6 months of retroactive benefits dating back before their application date. A widow who waited 8 months to apply can receive benefits dating back 6 months from the application date.

How to apply:

- By phone at 1-800-772-1213 (the SSA can initiate a survivor claim over the phone)

- In person at a local Social Security office — often recommended for survivor claims given the complexity

- Online applications for survivor benefits are limited — most survivor scenarios require a phone call or in-person visit

Documents to gather: death certificate, marriage certificate (or divorce decree if applicable), the deceased’s Social Security number, your Social Security number, birth certificates for any eligible children, and bank account information for direct deposit.

Pro Tip: Apply for survivor benefits as soon as you are eligible — even if you are unsure whether to start collecting immediately. You can request that benefit payments be withheld temporarily while you evaluate your strategy. Filing the application establishes your protected start date and preserves your retroactive benefit window. The SSA does not automatically know a worker has died — you must proactively initiate the claim.

On Medicare: Survivor benefits have no effect on Medicare eligibility. Medicare remains available at age 65 regardless of when you claim survivor benefits. Disabled widows and widowers receiving survivor benefits before 65 may qualify for Medicare after 24 months of disability benefits.

Note that if you plan to work while receiving survivor benefits before your FRA, the earnings test applies — benefits may be temporarily reduced if your earnings exceed the annual limit.

Survivor Benefits and Taxes — The Widow’s Tax Trap

Survivor benefits are taxed under the same “combined income” formula as all Social Security benefits:

Combined income = Adjusted Gross Income + Non-taxable interest + 50% of Social Security benefits

Single filers: Above $25,000 → up to 50% of benefits taxable; above $34,000 → up to 85% taxable Married filing jointly: Above $32,000 → up to 50% taxable; above $44,000 → up to 85% taxable

Here is the trap many surviving spouses walk into: the year after a spouse’s death, most survivors file as single — which dramatically lowers the taxation threshold from $32,000 to $25,000. The same income that was below the threshold as a married couple suddenly becomes significantly taxable as a single filer.

Richard and Nancy’s story: Richard and Nancy filed jointly with combined income of $58,000 — below the 85% SS taxation threshold. After Richard died, Nancy’s income remained similar ($56,000), but filing as a single filer changed everything. Her combined income of approximately $39,600 now exceeded both the $25,000 and $34,000 single filer thresholds, making 85% of her survivor benefit taxable — a significant tax increase with no actual increase in income.

Mitigation strategies:

- Roth conversions during lower-income years immediately after loss — before large Required Minimum Distributions begin — can reduce future taxable income

- Qualified Charitable Distributions (QCDs) from IRAs reduce AGI while satisfying charitable intentions

- Review IRA withdrawal timing in high-taxation years if cash flow allows

Common Mistake: Filing taxes the year after a spouse’s death without reviewing the changed taxation threshold. Many surviving spouses face a significant tax increase in the year following their loss — not because their income increased, but because their filing status changed.

Survivor Benefits for Children — A Guide for Surviving Parents

The caregiver benefit: A surviving spouse caring for the deceased worker’s child under age 16 (or a disabled child) qualifies for a survivor benefit immediately — with no age minimum. A 32-year-old widow with a 5-year-old qualifies for up to 75% of the deceased’s PIA right away, without waiting until 60.

The caregiver benefit ends when the youngest child turns 16 — at which point the surviving parent must wait until age 60 to claim again as a widow or widower. This gap is known as the “blackout period,” and it can last many years for young surviving families.

Danielle and Marcus: Danielle, 35, lost her husband Marcus. They had two children ages 3 and 7. Marcus’s PIA was $2,800. Danielle received $2,100/month immediately as a caregiver (75% of PIA), plus benefits for each child — subject to the family maximum. When her youngest turned 16 (when Danielle was 48), the caregiver benefit ended. Danielle faced a 12-year blackout period before age 60. Planning for that gap — through life insurance, savings, and her own career — became her most critical financial priority.

Children’s benefits end at 18 — or 19 if the child is still enrolled full-time in high school (college does not extend the benefit). For disabled children who became disabled before age 22, survivor benefits can continue for life — among the most valuable and least-claimed benefits in the entire Social Security system.

Special Circumstances — Remarriage, Multiple Marriages, and Non-Traditional Families

Remarriage: Remarrying before age 60 ends eligibility for survivor benefits on the deceased spouse’s record. Remarrying at 60 or later has no effect on eligibility. If a later marriage ends, eligibility on the original deceased spouse’s record may be restored.

Multiple marriages: If you are eligible for survivor benefits on more than one deceased spouse’s record, the SSA pays the higher amount. You cannot receive both simultaneously.

When the deceased never claimed: The survivor benefit is calculated based on what the worker would have received at FRA — not their age at death. However, if the worker died between FRA and age 70, the survivor benefit may include any partial delayed retirement credits earned up to the point of death.

Edward’s case: Edward died at 68 having never claimed. His PIA was $2,600, but he had earned one year of delayed retirement credits (8%), bringing his accrued benefit to $2,808. His widow received a survivor benefit based on $2,808 — not the lower PIA amount.

Minimal work history: For survivor benefits, the requirements are lower than for retirement benefits. A worker only needs to be “currently insured” — 6 quarters of coverage in the 13 quarters before death — for their family to qualify. A young worker who died early may still have enough credits for their children and spouse to receive survivor benefits.

Non-traditional families: Common-law marriages valid under state law, same-sex marriages, financially dependent stepchildren, and grandchildren where the grandparent had primary legal and financial responsibility — all may qualify. If you are unsure whether your situation qualifies, contact the SSA directly. Do not self-disqualify before getting an official determination.

The Survivor Benefit Action Checklist — What to Do and When

Immediately after the death:

- [ ] Obtain at least 10 certified copies of the death certificate from the funeral home or county vital records office

- [ ] Gather the deceased’s Social Security number, your Social Security number, your marriage certificate or divorce decree, and birth certificates for any eligible children

- [ ] Call the SSA at 1-800-772-1213 to report the death — do not assume the funeral home has done this

- [ ] Stop any direct deposits of the deceased’s own SS benefit — payments received after the month of death must be returned

Within the first month:

- [ ] Apply for the $255 lump-sum death payment — do not wait, though the deadline is 2 years

- [ ] Identify your eligibility category: widow/widower, divorced surviving spouse, caregiver parent, disabled survivor, or dependent parent

- [ ] Create an account at ssa.gov/myaccount to review your own Social Security statement and PIA estimates

Within the first 3 months:

- [ ] Consult a fee-only financial advisor or Social Security specialist to model your dual-benefit strategy — compare your own benefit at 70 vs. the full survivor benefit at FRA

- [ ] Review your new tax situation with a CPA — particularly the widow’s tax trap and whether Roth conversions make sense this year

- [ ] Update all beneficiary designations on your own accounts to reflect your changed circumstances

- [ ] Review any life insurance, pension survivor options, and employer death benefits

Before filing for survivor benefits:

- [ ] Compare your full survivor benefit at FRA vs. your own benefit at 70 — determine which strategy fits your situation

- [ ] If you have children under 16, file for your caregiver benefit and their children’s benefits at the same time

- [ ] Tell the SSA specifically whether you want to restrict your claim to the survivor benefit only, preserving your own retirement benefit to grow toward 70

Annually:

- [ ] Review your survivor benefit strategy, especially if your own retirement benefit is still growing toward 70

- [ ] Confirm the SSA is applying annual Cost of Living Adjustments to your survivor benefit each January

- [ ] Reassess the dual-benefit switch timing if your health or financial circumstances have changed

Also worth reviewing: our retirement readiness quiz includes a dedicated section on Social Security strategy — it can help you identify gaps in your overall plan beyond just survivor benefits.

Frequently Asked Questions

I was married for 9 years and 8 months when my husband died. Do I qualify?

The 9-month marriage requirement is strictly applied. However, exceptions exist: if you had a child together born of the marriage, if the death was accidental, or if the deceased was receiving Social Security disability benefits at the time of death. Contact the SSA directly to review your specific situation — do not assume you are ineligible without an official determination.

My ex-husband and I were married for 14 years before divorcing. He just passed away. Can I claim?

Yes. If you were married for at least 10 years and are currently unmarried (or remarried at 60 or later), you can claim survivor benefits on your ex-husband’s record. The divorce and the time elapsed since it do not disqualify you. Your benefit does not affect what his current spouse or other survivors receive.

I am 58 and my husband just died. Can I get any income from Social Security now?

Possibly. If you have children under 16 in your care, you qualify for the caregiver benefit immediately — no age minimum. If you are disabled, you can claim at 50. Otherwise, you will need to wait until 60 for a reduced survivor benefit. In the meantime, review your complete financial situation — including life insurance proceeds and available savings — with a financial advisor.

Can I claim the survivor benefit early and then switch to my own larger benefit at 70?

Yes — this is the dual-benefit strategy described above. When you apply, specifically tell the SSA you want to restrict your claim to the survivor benefit only. This preserves your own retirement benefit to grow toward 70. The SSA representative will guide you through the paperwork. For the complete context on this strategy, read our guide on Social Security for married couples strategy — your late spouse’s claiming decisions directly shaped the survivor benefit you are entitled to now.

Conclusion

The goal of this guide was simple: to make sure that anyone facing one of life’s most difficult moments has clear, complete, and compassionate information — information that empowers rather than overwhelms.

The three most important things to carry with you:

First, survivor benefits cover a broader circle than most people realize — spouses, divorced spouses after 10 years of marriage, children, disabled dependents, and even financially dependent parents may all qualify.

Second, the dual-benefit strategy — claiming one benefit early while letting the other grow — is the most powerful financial tool available to surviving spouses who have their own work record. Most survivors who have this option never use it.

Third, the survivor benefit maxes out at FRA. Your own retirement benefit maxes out at 70. Those are different ages with different growth rates, and understanding the difference is the foundation of a sound claiming strategy.

Survivor benefits exist because Social Security was built on a fundamental promise — that the contributions of a lifetime protect not just the worker, but the family they leave behind. You have earned this protection. Claim it.

Disclaimer: The content on RetireWealthPath.com is for informational and educational purposes only and does not constitute financial, tax, or legal advice. Social Security survivor benefit eligibility rules, benefit amounts, taxation thresholds, and application procedures referenced in this article reflect 2026 SSA guidelines and are subject to change. All calculations, reduction percentages, and named examples — including Catherine, Harold, Dorothy, Margaret, Richard, Nancy, Danielle, Marcus, Edward, and Victor — are for illustrative purposes only and do not represent guaranteed outcomes. Individual benefit amounts vary significantly based on the deceased worker’s earnings history, the survivor’s age at claiming, marital history, family composition, and other personal factors. Always contact the Social Security Administration directly at 1-800-772-1213 and consult a qualified financial professional before making survivor benefit claiming decisions.