How Social Security Is Calculated [The Complete 2026 Guide]

Your Social Security benefit is calculated from a formula so specific that two people with identical lifetime earnings can receive different monthly checks — simply because of when they were born, when they stopped working, and when they decided to claim.

Most people treat their Social Security benefit as a black box. They know roughly what the SSA says they’ll receive, but have no idea how that number was produced. That matters more than you might think — because understanding the formula reveals specific, actionable ways to increase your benefit before you ever file a claim.

This post walks through the SSA’s actual calculation method in plain English, with a real-world example carried through every step. It also shows you how to catch errors in your earnings record — errors that directly reduce your benefit and are far more common than most people realize.

The formula has four stages. By the end, you’ll be able to estimate your own benefit with nothing more than your earnings history and a calculator.

Why Your Social Security Benefit Is Not Random — The Four-Stage Formula

Before diving into each stage, here is the bird’s-eye view of how the entire calculation works. Think of this as your map before the journey.

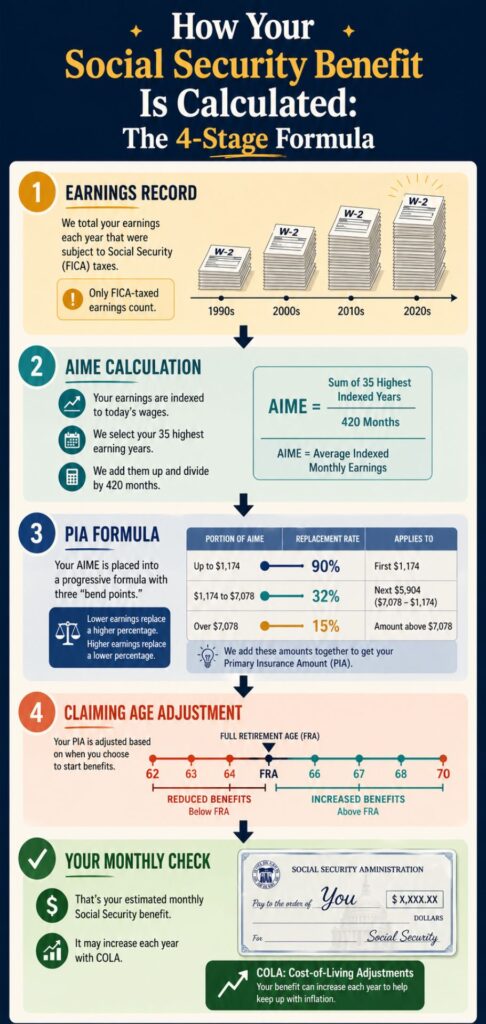

Stage 1 — Your Earnings Record The SSA collects your taxable wages and self-employment income for every year you worked. This is the raw data for the entire calculation.

Stage 2 — Indexed Earnings and AIME The SSA adjusts your historical earnings for wage inflation (called indexing), identifies your 35 highest-earning years, and calculates your Average Indexed Monthly Earnings (AIME) — a single monthly figure representing your career earnings power.

Stage 3 — The PIA Formula and Bend Points The SSA applies a progressive formula to your AIME using specific dollar thresholds called “bend points” to calculate your Primary Insurance Amount (PIA) — the benefit you receive at exactly your Full Retirement Age.

Stage 4 — Adjustments for Claiming Age Your PIA is then increased or decreased based on whether you claim before, at, or after your Full Retirement Age — producing your actual monthly check.

💡 The Formula in One Line: Earnings Record → Indexed to Today’s Dollars → 35-Year Average (AIME) → Progressive Formula (PIA) → Claiming Age Adjustment → Your Monthly Check

Every number on your Social Security statement is the output of this four-stage process. Understanding each stage shows you exactly where your benefit comes from — and where you can influence it.

We will follow David — a 62-year-old project manager from Ohio planning to retire at 67 — through every stage of the calculation. His numbers will stay consistent across every example and table.

Stage 1 — Your Earnings Record (The Raw Material)

The earnings record is the foundation of everything. An error here doesn’t just affect one calculation — it compounds through every subsequent stage and reduces your final benefit for the rest of your life.

What the SSA Tracks

The SSA records every dollar of wages earned as an employee — reported by your employer via W-2 forms — and every dollar of net self-employment income reported on Schedule SE of your federal return. These records go back to your very first job and are stored under your Social Security number.

What counts toward your benefit:

- Wages and salaries on which Social Security (FICA) taxes were paid

- Net self-employment income after the self-employment tax deduction

- In 2026, Social Security taxes apply only to the first $176,100 of wages — earnings above this are not taxed for Social Security and do not count toward your benefit

What does NOT count:

- Investment income — dividends, capital gains, interest

- Rental income

- Pension or annuity payments

- Income earned in certain government jobs covered by a separate pension system

This is worth understanding clearly: someone who retires at 60 and lives on investment income for the next decade is not building Social Security credits during those years. Those are potential zero years in the 35-year calculation — more on that in Stage 2.

The Earnings Record Error Problem

The SSA processes hundreds of millions of W-2 forms annually. Errors occur more frequently than most people realize. Common problems include missing years of employment (especially from early-career jobs or self-employment), incorrect wage amounts, and earnings credited to the wrong Social Security number.

The SSA estimates that roughly 4% of earnings records contain at least one error. An error in your record directly reduces your calculated benefit — often permanently if not corrected before you claim.

💡 Pro Tip: Review your Social Security earnings record at least once every three years — and always within the year before you plan to claim. Go to ssa.gov/myaccount, create your free account, and download your complete earnings history. Compare it against your W-2s and tax returns for any year that looks wrong. Correcting an error before claiming can add meaningful dollars to your monthly benefit for life.

Stage 2 — Indexing Your Earnings and Calculating Your AIME

This is where the math begins. The concept of “indexing” sounds technical, but the logic behind it is straightforward once you understand the problem it solves.

Why Indexing Exists — The Fairness Problem

A dollar earned in 1985 is not the same as a dollar earned in 2015. Wages have grown significantly due to inflation and overall economic growth. Without adjusting for this, someone who earned $25,000 in 1985 would appear to have earned the same as someone earning $25,000 in 2015 — even though $25,000 in 1985 represented far greater purchasing power and relative earnings.

Indexing converts all historical earnings to today’s equivalent wages — making the comparison fair across your entire career. The SSA uses the National Average Wage Index (NAWI) to perform this conversion.

One important technical note: the SSA only indexes your earnings up through the year you turn 60. Earnings after age 60 are used at face value without adjustment.

How Indexing Works

The indexing factor for each year is calculated as:

Indexing Factor = NAWI in your indexing year ÷ NAWI in the year the wages were earned

Your earnings for that year are multiplied by this factor to produce your “indexed” earnings.

“David earned $18,000 in 1985 at age 22. The NAWI in 1985 was $16,823. His indexing year is 2022 (the year he turned 60), when the NAWI was $63,795. His indexing factor: $63,795 ÷ $16,823 = 3.79. His indexed 1985 earnings: $18,000 × 3.79 = $68,220. That $18,000 from 1985 is treated as if David earned $68,220 — accurately reflecting how that income compared to today’s wages.”

The 35-Year Rule — Only Your Best Years Count

After indexing, the SSA identifies your 35 highest-earning years. These are the only years that count toward your benefit.

If you worked fewer than 35 years, zeros are inserted for the missing years — which directly drags down your average. This is one of the most important and underappreciated aspects of the entire calculation.

Here is what zero years cost you, using $60,000 as the average indexed earnings in working years:

| Years Worked | Zero Years | Total Indexed Earnings | Monthly AIME |

|---|---|---|---|

| 35 | 0 | $2,100,000 | $5,000 |

| 32 | 3 | $1,920,000 | $4,571 |

| 30 | 5 | $1,800,000 | $4,286 |

| 25 | 10 | $1,500,000 | $3,571 |

| 20 | 15 | $1,200,000 | $2,857 |

Source: Illustrative calculations based on SSA 35-year averaging methodology. For educational purposes only.

The drop from 35 working years to 30 is $714/month in AIME — which, as we’ll see in Stage 3, translates directly into a permanently lower monthly benefit.

Calculating the AIME

Once the 35 highest indexed years are identified, the SSA adds them together and divides by 420 — that is 35 years multiplied by 12 months.

“David’s 35 highest indexed earning years total $1,890,000. Divided by 420 months: $1,890,000 ÷ 420 = $4,500. David’s AIME is $4,500 per month.”

⚠️ Common Mistake: Many people assume that working more than 35 years doesn’t matter. It does. Every additional year you work replaces the lowest-earning year in your 35-year calculation with a (presumably higher) current-year earning. For anyone with low-income early career years, even a few extra working years in a higher-paying role can meaningfully increase the AIME — and the lifetime benefit that flows from it.

Stage 3 — The PIA Formula and the Bend Points

This is the most misunderstood — and most progressive — stage of the Social Security calculation. Understanding it changes how you think about the program entirely.

What Is the Primary Insurance Amount (PIA)?

The PIA is the monthly benefit you would receive if you claimed Social Security at exactly your Full Retirement Age. It is the anchor number for everything else — early claiming reductions, delayed retirement credits, spousal benefits, and survivor benefits are all calculated as percentages of your PIA.

Understanding Bend Points — Why Social Security Is Progressive

The SSA does not give you a flat percentage of your career earnings as your benefit. Instead, it applies different replacement rates to different portions of your AIME — giving a higher percentage to lower earners and a lower percentage to higher earners.

This is the progressive design of Social Security: it replaces a larger share of income for lower-wage workers. The dollar thresholds where these replacement rates change are called bend points, and they are adjusted annually for wage inflation.

2026 Bend Points and Replacement Rates:

| Portion of AIME | Replacement Rate | What It Means |

|---|---|---|

| First $1,226 | 90% | High replacement for low earnings |

| $1,226 to $7,391 | 32% | Moderate replacement for middle earnings |

| Above $7,391 | 15% | Lower replacement for high earnings |

Source: Social Security Administration, 2026 bend point thresholds. Adjusted annually based on the National Average Wage Index.

Calculating David’s PIA — Step by Step

David’s AIME is $4,500.

Step 1: Apply 90% to the first $1,226 of AIME $1,226 × 90% = $1,103.40

Step 2: Apply 32% to the AIME between $1,226 and $4,500 ($4,500 − $1,226) × 32% = $3,274 × 32% = $1,047.68

Step 3: Nothing in the third tier — David’s AIME of $4,500 is below the $7,391 second bend point.

Step 4: Add the results $1,103.40 + $1,047.68 = $2,151.08

Step 5: Round down to the nearest $0.10 David’s PIA = $2,151.00 per month — the benefit he would receive at exactly age 67.

Here is how the PIA calculation plays out across different AIME levels using 2026 bend points:

| Monthly AIME | PIA Calculation | Estimated PIA | Income Replacement Rate |

|---|---|---|---|

| $1,000 | 90% × $1,000 | $900 | 90.0% |

| $2,000 | (90% × $1,226) + (32% × $774) | $1,351 | 67.6% |

| $3,500 | (90% × $1,226) + (32% × $2,274) | $1,831 | 52.3% |

| $4,500 | (90% × $1,226) + (32% × $3,274) | $2,151 | 47.8% |

| $6,000 | (90% × $1,226) + (32% × $4,774) | $2,631 | 43.9% |

| $8,000 | (90% × $1,226) + (32% × $6,165) + (15% × $609) | $3,136 | 39.2% |

Source: Illustrative calculations using 2026 SSA bend points. Actual benefits vary. For educational purposes only.

💡 Pro Tip: Notice that someone with an AIME of $1,000 gets back 90 cents for every dollar of average monthly earnings — while someone with an AIME of $8,000 gets back only about 39 cents per dollar. Social Security is specifically designed to be a stronger safety net for lower earners. If you are a higher earner, this is exactly why your retirement number needs to account for a larger contribution from your 401(k), IRA, and other savings — Social Security will replace a smaller share of your pre-retirement income.

Stage 4 — Adjusting for Claiming Age

Your PIA is not your final benefit. The last stage adjusts it upward or downward based on when you actually claim. This is where timing becomes everything.

Early Claiming Reductions

Claiming before FRA permanently reduces your monthly benefit below your PIA. The reduction is calculated in two tiers:

- For the first 36 months before FRA: benefit reduced by 5/9 of 1% per month (approximately 6.67% per year)

- For months beyond 36 before FRA: benefit reduced by 5/12 of 1% per month (approximately 5% per year)

For someone with an FRA of 67 claiming at 62 — 60 months early:

- First 36 months: 36 × (5/9 × 1%) = 20% reduction

- Next 24 months: 24 × (5/12 × 1%) = 10% reduction

- Total reduction: 30% — leaving 70% of PIA

“David’s PIA is $2,151. If he claims at 62 — 60 months before his FRA of 67 — his benefit is reduced by 30%: $2,151 × 70% = $1,505.70/month. That reduction follows him for life.”

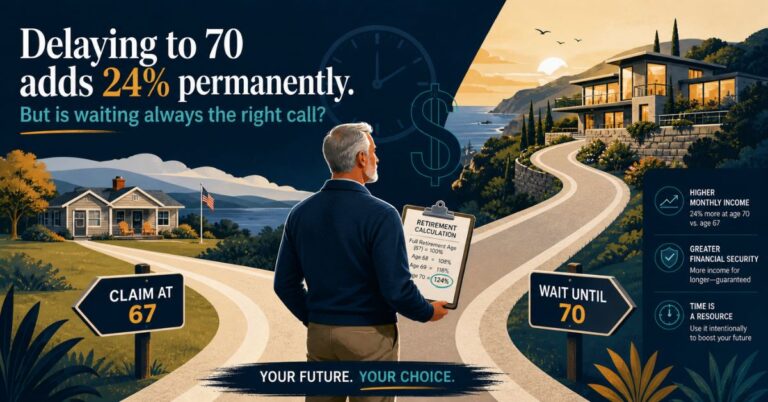

Delayed Retirement Credits

Delaying past FRA earns Delayed Retirement Credits of 8% per year (2/3 of 1% per month) up to age 70. These credits are applied on top of the full PIA.

“David’s PIA is $2,151. Delaying from 67 to 70 earns 36 months × (2/3 × 1%) = 24% increase: $2,151 × 124% = $2,667.20/month. That increase also follows him for life.”

Here is David’s complete benefit range across every claiming age:

| Claiming Age | Adjustment | Monthly Benefit | Annual Benefit | Difference vs. FRA |

|---|---|---|---|---|

| 62 | −30% | $1,505 | $18,060 | −$7,752/year |

| 63 | −25% | $1,613 | $19,356 | −$6,456/year |

| 64 | −20% | $1,721 | $20,652 | −$5,160/year |

| 65 | −13.3% | $1,865 | $22,380 | −$3,432/year |

| 66 | −6.7% | $2,007 | $24,084 | −$1,728/year |

| 67 (FRA) | 0% | $2,151 | $25,812 | Baseline |

| 68 | +8% | $2,323 | $27,876 | +$2,064/year |

| 69 | +16% | $2,495 | $29,940 | +$4,128/year |

| 70 | +24% | $2,667 | $32,004 | +$6,192/year |

Source: Illustrative calculations based on David’s PIA of $2,151 using SSA claiming age adjustment formulas. For educational purposes only.

The annual difference between claiming at 62 and 70 is $13,944 per year — for life, inflation-adjusted. Over a 20-year retirement that is $278,880. For a thorough breakdown of how to choose between these ages based on your health, finances, and marital status, the retirement readiness quiz includes a dedicated Social Security strategy scoring section that walks you through the decision systematically.

Cost of Living Adjustments (COLAs)

Once you begin receiving benefits, your monthly amount is increased each year by the Cost of Living Adjustment (COLA), tied to the Consumer Price Index for Urban Wage Earners. Recent COLAs: 8.7% in 2023, 3.2% in 2024, 2.5% in 2025.

COLAs apply to your actual monthly benefit — meaning a higher starting benefit generates larger absolute dollar increases every year. Over a 20–25 year retirement, this compounding effect significantly widens the gap between early and late claimers beyond what the simple table above shows.

Five Ways to Increase Your Social Security Benefit Before You Claim

Understanding the formula is powerful because it reveals exactly which levers you can pull. Here are five of them.

Strategy 1 — Work at Least 35 Years

Every zero-earning year in your 35-year average reduces your AIME — and therefore your PIA. If you have 30 years of earnings and 5 zeros, adding even 5 years of part-time work replaces those zeros with real earnings. The benefit increase from eliminating zero years can be substantial and permanent.

Strategy 2 — Replace Low-Earning Years With Higher-Earning Years

Already past 35 years of work? Additional working years replace your lowest-earning indexed years in the 35-year calculation. For anyone whose early career involved low-paid years, this lever is still available well into their 60s.

“Suppose David has a year in his record where his indexed earnings were $12,000 — a year he worked part-time. If he works one additional year and earns $80,000, that $80,000 replaces the $12,000 in his 35-year average — adding $68,000 to his total indexed earnings. At a 32% replacement rate through the bend point formula, that adds roughly $160/month to his PIA permanently.”

Strategy 3 — Maximize Earnings in Your Final Working Years

Because earnings after age 60 are used at face value without indexing, maximizing income in your final working years directly and proportionally increases your AIME — if those years rank among your top 35. Raises, promotions, and higher-income positions in your late 50s and early 60s are worth more to your Social Security benefit than the same earnings 20 years earlier.

Strategy 4 — Correct Errors in Your Earnings Record

As covered in Stage 1, earnings record errors are common. A missing year of $60,000 in indexed earnings reduces your 35-year total by $60,000 — which at a 32% replacement rate reduces your PIA by approximately $1,600 per year, every year of your retirement. Checking your record before claiming costs nothing. Failing to check it can cost a great deal.

Strategy 5 — Delay Claiming

The most straightforward lever: every year of delay past FRA adds 8% permanently. For David with a PIA of $2,151, delaying from 67 to 70 adds $6,192 per year — for life, inflation-adjusted. For anyone in good health with sufficient savings to bridge the gap, this remains one of the highest guaranteed returns available in retirement planning.

How Your Social Security Benefit Is Calculated – The 4-Stage Formula

Special Situations That Affect the Calculation

Several common life situations create important exceptions to the standard formula. If any of these apply to you, they are worth understanding before you estimate your benefit.

Windfall Elimination Provision (WEP)

WEP applies to workers who receive a pension from a job not covered by Social Security — certain state and local government jobs, some federal jobs pre-1984 — and who also have Social Security-covered earnings. WEP modifies the 90% replacement rate in the first bend point, reducing it to as low as 40%, which can significantly reduce the PIA.

This affects approximately 2 million beneficiaries. If you have worked in both covered and non-covered employment, research WEP before estimating your benefit — the standard SSA calculator does not always reflect WEP reductions accurately.

Government Pension Offset (GPO)

GPO applies to spousal and survivor benefits for people who receive a government pension from non-SS-covered employment. GPO reduces spousal and survivor Social Security benefits by two-thirds of the government pension amount — in many cases eliminating the spousal benefit entirely. This is a significant planning issue for couples where one spouse worked in a non-covered government position.

Self-Employment and the Calculation

Self-employed individuals pay both the employee and employer share of Social Security taxes — 12.4% of net self-employment income up to the wage base. Only net self-employment income after business expenses counts toward the AIME calculation.

Here is a genuine trade-off worth thinking through carefully: self-employed workers who minimize reported income to reduce their tax bill may be simultaneously minimizing their future Social Security benefit. The right answer depends on your specific income level and retirement timeline, but it is a trade-off to evaluate deliberately rather than ignore.

Career Gaps — Raising Children, Caregiving, Illness

Each year of zero earnings added to the 35-year average directly reduces the AIME. The good news: even modest earnings during gap years — $15,000 to $20,000 from part-time work — can replace a zero and meaningfully improve the final benefit. This is not a lecture on working during family leave. It is a math fact worth knowing so you can make an informed choice.

⚠️ Common Mistake: Assuming the benefit estimate on your SSA statement reflects your actual expected benefit. The statement assumes you will continue earning at your current income level every year until your full retirement age. If you plan to retire early, take a significant pay cut, or have career gaps ahead, your actual benefit will be lower than the statement shows. Always recalculate based on your real expected earnings path. If this affects your retirement number calculation, the gap can be meaningful.

How to Verify Your Own Calculation — Step by Step

Here is the practical process for checking your own numbers before you make any claiming decision.

Step 1 — Pull your earnings record from SSA.gov Create or log into your my Social Security account at ssa.gov/myaccount. Download your complete earnings history from your first job to the most recent filed return. Flag any years that look incorrect or missing.

Step 2 — Index your earnings (simplified approach) For a rough estimate, use the SSA’s online benefit calculator at ssa.gov/benefits/calculators — it performs the full indexing automatically. For a manual calculation, the SSA publishes the National Average Wage Index for every year at ssa.gov/oact/cola/AWI.html.

Step 3 — Identify your 35 highest-earning indexed years From your indexed earnings history, identify the top 35 years. If you have fewer than 35 years of earnings, count how many zeros you’ll be averaging in — and consider whether additional working years are worth it to you.

Step 4 — Calculate your AIME Add the 35 highest indexed annual earnings together and divide by 420. This is your estimated AIME.

Step 5 — Apply the bend point formula Use the current year’s bend points (published at ssa.gov/oact/cola/bendpoints.html). Apply 90% to the first $1,226, 32% to the amount between $1,226 and $7,391, and 15% to anything above $7,391. Add the three results and round down to the nearest $0.10. This is your estimated PIA.

Step 6 — Adjust for your planned claiming age Apply the reduction or credit percentage for your target claiming age using the formula from Stage 4.

Step 7 — Compare to your SSA statement Your manual estimate should be reasonably close to the SSA’s projection. A significant discrepancy may indicate an earnings record error worth investigating.

💡 Pro Tip: The SSA’s detailed calculator at ssa.gov/benefits/calculators/anypia.html — called “AnyPIA” — lets you input your actual earnings history year by year and calculates your exact PIA using the official formula. It’s the same tool SSA employees use. It requires downloading a small program but produces the most accurate manual estimate available outside of your official statement.

FAQs About How Social Security Is Calculated

Does Social Security look at my last 10 years of earnings or my entire career?

Social Security looks at your entire career — every year you had wages or net self-employment income subject to FICA taxes. However, only your 35 highest-earning years after adjusting for wage inflation are used in the final calculation. Earlier years don’t disappear — they are indexed to today’s wage levels and compared against your more recent years. Your full career history matters, and checking every year for errors is worthwhile.

What happens to my Social Security calculation if I take 5 years off to raise children?

Each year you don’t work counts as a zero in the 35-year averaging calculation. Five years of zeros reduce your total indexed earnings by five years’ worth of what you would otherwise have earned — which lowers your AIME and your PIA. However, if you already have more than 35 years of earnings, those five gap years replace your five lowest-earning years instead of being pure zeros — a smaller impact. Even modest part-time earnings during gap years can replace a zero and improve your benefit.

Do I pay Social Security taxes on investment income, rental income, or pension income?

No. Social Security taxes apply only to earned income — wages from employment and net profit from self-employment. Investment income, rental income, pension payments, and Social Security benefits themselves are not subject to FICA and do not count toward your earnings record or AIME calculation. This is why some retirees who live primarily on investment income may have a lower Social Security benefit than their total wealth would suggest.

If I work after claiming Social Security, does it increase my benefit?

Potentially yes. The SSA automatically reviews your earnings record each year after you claim. If your current-year earnings are higher than one of your 35 highest indexed years on record, the SSA replaces the lower year and recalculates your PIA — increasing your monthly benefit starting the following January. This recalculation happens automatically without any action required from you.

How does the calculation work for someone who was self-employed their whole career?

Self-employed workers follow the same four-stage formula as employees. The key difference is the reporting mechanism: self-employed individuals report net profit from Schedule C, and the AIME calculation uses net earnings after the self-employment tax deduction. Because self-employed people pay both halves of FICA — 12.4% total for Social Security — they have a higher tax burden than employees, but the same benefit formula applies to the income that gets reported. The planning implication: consistently underreporting income to minimize taxes has a direct cost to your future benefit that compounds over a full retirement. Our retirement planning vocabulary guide covers the key terms — AIME, PIA, bend points, FICA, COLA — if you want a quick reference alongside the formulas above.

The Bottom Line

The formula that determines your Social Security benefit has been calculating since your very first paycheck. You now know exactly what it has been doing — and how to make it work harder for you.

Three things worth carrying with you:

- Zero years in your earnings record cost you. Even modest additional working years replace zeros and increase your benefit — and every dollar added to your AIME flows through the bend point formula into a permanent monthly increase.

- Your SSA statement assumes you’ll keep earning at your current level until retirement. If you plan to retire early or expect career gaps, your actual benefit will be lower than stated. Recalculate based on your real expected earnings path.

- Errors in your earnings record are common and correctable. Checking your record at ssa.gov/myaccount is one of the highest-ROI actions available before you claim — and it costs nothing.

Now that you understand how your benefit is calculated, the logical next question is when to claim it for maximum lifetime income. The retirement readiness quiz scores your Social Security strategy — including whether your claiming timing, spousal coordination, and earnings record are in order — alongside seven other retirement readiness categories. It is a useful next step before you finalize any decisions.

The formula has been working in the background since your first job. Now you know what it’s been doing — and how to make it work harder for you.

Disclaimer: The content on RetireWealthPath.com is for informational and educational purposes only and does not constitute financial, tax, or legal advice. We are not licensed financial advisors. The Social Security benefit calculation formula, bend point thresholds, and COLA figures referenced in this article reflect 2026 SSA guidelines and are subject to change by legislation or SSA policy. All calculations and examples — including David’s case study — are for illustrative and educational purposes only and do not represent guaranteed benefit amounts. Individual benefits vary based on your personal earnings history, claiming age, and other factors. Always verify your benefit estimate through your official my Social Security account at ssa.gov and consult a qualified financial professional before making claiming decisions. Retirement planning involves risk and individual results will vary.