Best Age to Claim Social Security Benefits [2026 Guide]

The difference between claiming Social Security at 62 versus waiting until 70 can exceed $200,000 in lifetime benefits. And unlike most financial decisions, this one cannot be undone.

Nearly everyone approaching retirement has heard they should “probably wait” to claim. But very few people understand the actual mechanics well enough to make a confident, eyes-open decision — one they won’t second-guess for the rest of their lives.

Here is what this guide will give you: the foundational math behind every claiming age, a five-factor framework you can apply to your own situation, and clear directional recommendations for the most common scenarios you are actually likely to face. You will leave with either a clear decision or a clear process for making one.

One important note before we dive in. After the 12-month “do-over” window closes, your claiming age is permanent. That is a reason to think carefully — not to panic. Let’s start with the three ages the Social Security Administration gives you and what each one actually means for your monthly check.

The Three Claiming Ages — What the SSA Actually Offers You

Most people know that 62, 67, and 70 are the key milestones. Very few understand what each one means in real dollar terms. Here is the foundational math before any strategy discussion.

Age 62 — The Earliest Option

You can claim as early as the month you turn 62 — but your benefit is permanently reduced. For anyone born in 1960 or later, whose Full Retirement Age is 67, claiming at 62 means receiving only 70% of your Full Retirement Age benefit. That 30% reduction does not go away when you reach 67. It follows you for life, and it affects any survivor benefit your spouse may eventually receive.

The appeal is real and legitimate: immediate cash flow, especially if you have health concerns, need to stop working, or face pressing financial needs. The benefit is reduced, but you receive it for more years — which is precisely why break-even analysis matters.

Age 67 — Your Full Retirement Age (FRA)

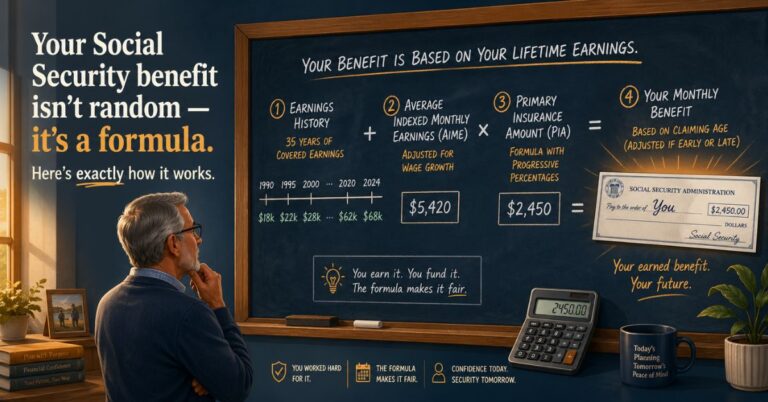

For everyone born in 1960 or later, Full Retirement Age is 67. Claiming at FRA gives you 100% of your Primary Insurance Amount (PIA) — the benefit calculated from your 35 highest-earning years. FRA is the neutral option: no permanent reduction, no delayed retirement credits.

Most Americans claim before FRA. The average claiming age in the U.S. is approximately 64, meaning most people accept a permanent benefit reduction. Claiming at exactly FRA makes sense in specific circumstances — covered in detail later in this guide.

Age 70 — The Maximum Benefit

For every year you delay past FRA up to age 70, your benefit grows by 8% per year — called Delayed Retirement Credits. Waiting from 67 to 70 adds a permanent 24% increase to your monthly benefit for life, adjusted annually for inflation via Cost of Living Adjustments (COLAs). There is no benefit to waiting past 70. Delayed Retirement Credits stop accruing at exactly that age.

The 8% annual growth is essentially a guaranteed, inflation-adjusted return — difficult to match in any conventional investment product. For long-lived retirees, it is one of the most powerful financial moves available.

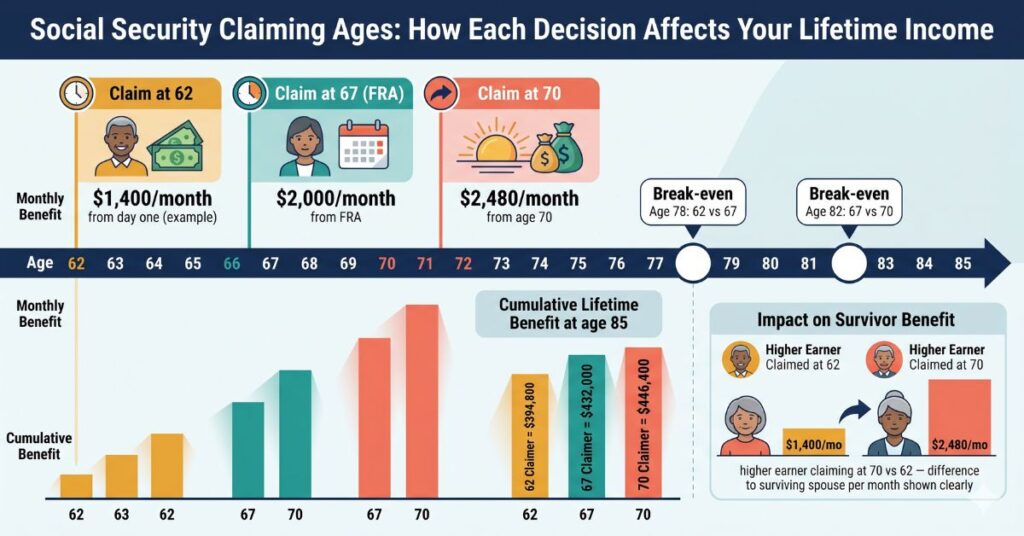

Here is what the math looks like using a $2,000 FRA monthly benefit as the example:

| Claiming Age | % of FRA Benefit | Monthly Benefit | Annual Benefit | 20-Year Total |

|---|---|---|---|---|

| 62 | 70% | $1,400 | $16,800 | $336,000 |

| 63 | 75% | $1,500 | $18,000 | $360,000 |

| 64 | 80% | $1,600 | $19,200 | $384,000 |

| 65 | 86.7% | $1,733 | $20,800 | $415,900 |

| 66 | 93.3% | $1,867 | $22,400 | $448,000 |

| 67 (FRA) | 100% | $2,000 | $24,000 | $480,000 |

| 68 | 108% | $2,160 | $25,920 | $518,400 |

| 69 | 116% | $2,320 | $27,840 | $556,800 |

| 70 | 124% | $2,480 | $29,760 | $595,200 |

Source: Social Security Administration benefit calculation guidelines, 2026. Example assumes $2,000 FRA monthly benefit and does not include COLA adjustments or taxes. For illustrative purposes only.

The monthly difference between claiming at 62 and 70 in this example is $1,080 — every single month, for life. Over 20 years that is $259,200. The question is whether waiting earns that premium — and that depends on your break-even point.

The Break-Even Analysis — The Math That Actually Drives the Decision

The break-even point is the most important concept in Social Security claiming strategy and the most underexplained. It is the age at which the total lifetime benefits from waiting equal the total lifetime benefits from claiming early. Past that point, the higher monthly benefit wins. Before it, the early claimer has collected more in total.

Here is how to calculate your break-even point:

Step 1: Calculate the monthly difference between the two claiming ages.

Step 2: Calculate the total amount given up by waiting — months of no benefit multiplied by the monthly benefit at the earlier age.

Step 3: Divide the total given up by the monthly difference in benefits.

Example: Waiting from 62 to 70 means giving up 96 months × $1,400 = $134,400 in foregone benefits. The monthly gain from waiting is $1,080. Break-even: $134,400 ÷ $1,080 = 124.4 months after age 70 = approximately age 80 years and 4 months.

What this tells you: if you expect to live past your break-even age, waiting produces more lifetime income. If you expect to live less, claiming early produces more. For the 62 vs. 70 comparison, the break-even is typically around age 80–81. For the 67 vs. 70 comparison, it is around age 82–83.

One important nuance: break-even analysis treats money as having no time value. A dollar received at 62 can be invested and grow. A more sophisticated analysis accounts for this opportunity cost and generally shifts the break-even age higher by one to two years. For most long-lived people, it still does not change the final decision — but it is worth understanding before drawing firm conclusions.

Pro Tip: The SSA’s official break-even calculator at ssa.gov/benefits/retirement/planner/breakeven.html lets you plug in your actual benefit estimates and see your personalized break-even age in minutes. Use it alongside this guide for your most accurate analysis.

The Five Factors That Determine YOUR Best Claiming Age

The math tells you how the system works. These five factors tell you where you fit within it. Work through each one honestly — your answers will point you toward a clear claiming direction.

Factor 1 — Your Health and Family Longevity

This is the single most important variable in the claiming decision.

If you have serious health conditions that meaningfully reduce your life expectancy below average, claiming early at 62 or 63 is often mathematically superior. If you are in excellent health, have parents or siblings who lived into their late 80s or 90s, and have no major chronic conditions, delaying to 70 almost always produces the highest lifetime benefit.

The Social Security system is designed to be approximately neutral for someone of average health — the average person breaks even at roughly the same age regardless of claiming date. That means the claiming decision is essentially a bet on your longevity relative to the average.

Take Gerald, 64, who has been managing Type 2 diabetes and had a cardiac event at 61. His cardiologist has advised him that his long-term health outlook is uncertain. Gerald claims at 62 — collecting benefits immediately rather than betting on living past 80. For Gerald, this is the right call.

His neighbor Patricia, also 64, is in excellent health, runs three days a week, and has a mother who lived to 94. Patricia delays to 70. She breaks even at 82 and collects a significantly higher benefit for every year she lives past that point.

Same age. Completely different correct answers.

Factor 2 — Your Financial Situation and Portfolio Size

If you have substantial retirement savings and do not need Social Security income to cover expenses in your 60s, delay. Use portfolio withdrawals to bridge the gap from retirement to 70, then let Social Security cover a larger share of ongoing expenses.

This is called the portfolio bridge strategy — deliberately withdrawing from your 401(k) or IRA from ages 62–70 to fund living expenses while your Social Security grows at 8% per year guaranteed. It often produces better tax outcomes too, by reducing pre-tax balances before Required Minimum Distributions begin at age 73.

If your retirement portfolio can sustain eight years of withdrawals without jeopardizing your long-term security, seriously consider delaying Social Security to 70.

If you have minimal retirement savings and Social Security is your primary income source, the calculus is more complex. Claiming early provides immediate income, but locking in a permanently lower benefit is a significant long-term risk — especially if you live well into your 80s or 90s. This is one of the situations covered in the retirement readiness quiz if you want to stress-test your specific scenario.

Factor 3 — Whether You Are Still Working

If you claim before your Full Retirement Age and continue working, the SSA reduces your benefits if you earn above a threshold. In 2026, that threshold is $22,320 per year. For every $2 you earn above this amount, $1 in Social Security benefits is withheld.

A critical nuance: withheld benefits are not permanently lost. They are recredited to your account when you reach FRA, permanently increasing your monthly benefit. However, the administrative complexity and cash flow disruption make claiming before FRA while working full-time almost never the optimal choice.

Simple Rule: If you are still working full-time and earning above $22,320 per year, do not claim Social Security before your Full Retirement Age.

Factor 4 — Your Marital Status and Spousal Considerations

For single individuals, the decision is purely personal longevity and financial math.

For married couples, the higher earner’s claiming decision has profound implications for both spouses — because when a spouse dies, the survivor inherits the deceased spouse’s monthly benefit as a survivor benefit. A higher monthly benefit for the primary earner means a higher survivor benefit for the widow or widower, potentially for decades.

Here is what that looks like in practice. James and Carol are both 62. James earned significantly more throughout his career; his FRA benefit is $3,200 per month. Carol’s is $1,400 per month. Carol claims at 62 — receiving $980 per month — to provide immediate household income. James delays to 70, when his benefit reaches $3,968 per month.

If James dies first, Carol receives James’s $3,968 per month as a survivor benefit — nearly four times what she would have received if James had claimed at 62. This single decision is worth more to Carol’s financial security than almost any other move they could make.

One additional note for divorced readers: if you were married for at least 10 years and are currently unmarried, you may be eligible for a spousal benefit on your ex-spouse’s record without affecting their benefit at all. Check your eligibility at SSA.gov before making your claiming decision.

Factor 5 — Your Tax Situation

Social Security benefits are taxable if your combined income — AGI plus non-taxable interest plus 50% of your Social Security — exceeds $25,000 for single filers or $32,000 for married filers. Up to 85% of your benefit can be subject to federal income tax.

Delaying Social Security reduces the number of years you pay taxes on benefits. But the interaction with Required Minimum Distributions matters: if you delay SS to 70 and have large traditional IRA or 401(k) balances, your income at 73 — Social Security plus RMDs — could trigger IRMAA Medicare premium surcharges.

Ages 62–72 with no Social Security income and lower RMDs can be an ideal window for Roth conversions, reducing future taxable income and IRMAA exposure for the rest of your life. This interaction is complex enough to warrant professional review for anyone with significant pre-tax retirement account balances. If you are not yet clear on how RMDs and tax brackets interact, our retirement planning vocabulary guide covers the key terms — PIA, FRA, COLA, IRMAA, and RMDs — in plain language.

Claiming Age Recommendations by Situation

After working through the five factors, here is where most readers will land. Find your situation, use it as your starting point, and adjust based on what you learned above.

| Your Situation | Recommended Age | Primary Reason |

|---|---|---|

| Excellent health, significant savings, married | 70 | Maximize survivor benefit + lifetime income |

| Excellent health, single, significant savings | 70 | Strong longevity odds favor delay |

| Good health, limited savings, need income | 65–67 | Balance immediate need with reasonable benefit |

| Poor health or chronic illness | 62–64 | Break-even likely unreachable; claim early |

| Still working full-time above earnings limit | 67 (FRA) | Avoid earnings test reduction |

| Married, lower earner, higher earner delaying | 62–64 | Bridge income while higher earner’s benefit grows |

| Divorced after 10+ year marriage | 62–70 | Check ex-spousal benefit eligibility first |

| Widowed with survivor benefit available | Varies | Model survivor vs. own benefit — often claim own early, survivor later |

Note: These are general guidelines only. Your specific situation may differ significantly. Consult a fee-only financial advisor for personalized analysis.

The Case for Claiming at 62

Claiming at 62 makes the most sense when you have a serious health condition or family history of short life expectancy, you have been laid off and need income immediately, you are the lower earner in a marriage where your spouse plans to delay to 70, or you have sufficient savings that the reduced benefit will not threaten your long-term security.

Eligibility at 62 is not a recommendation. But for the right person, it is absolutely the right call.

The Case for Claiming at 67

Claiming at Full Retirement Age makes the most sense when you are still working but want to claim without the earnings test complexity, your health is genuinely uncertain — not clearly excellent, not clearly poor — or your portfolio requires some Social Security income but you do not urgently need it at 62. It is the neutral option, and there is nothing wrong with choosing it deliberately.

The Case for Claiming at 70

Claiming at 70 makes the most sense when you are in excellent health with a strong family longevity history, you have sufficient assets to fund living expenses from 62–70 without Social Security, you are the higher earner in a marriage and want to maximize the survivor benefit, or you are specifically concerned about longevity risk — running out of money in your late 80s or 90s.

A higher Social Security benefit at 70 is the closest thing to bulletproof longevity insurance that exists in the American financial system. You cannot outlive it. It adjusts for inflation every year. And it requires no investment management or ongoing decisions on your part.

The Spousal and Survivor Benefit Strategy — The Most Underused Optimization

Most retirement articles either skip this section or reduce it to a footnote. That is a mistake. For married couples, the interaction between spousal benefits and survivor benefits can be worth hundreds of thousands of dollars — and the strategy is straightforward once you understand the mechanics.

Spousal benefit basics:

A spouse who earned less — or did not work — can claim up to 50% of the higher earner’s FRA benefit, regardless of when the higher earner actually claims. Critically, the spousal benefit does not increase if the higher earner delays past FRA. It is always capped at 50% of the FRA benefit. The lower earner must claim their own benefit first; the spousal top-up is the difference between their own benefit and 50% of their spouse’s FRA benefit, if that is higher.

Survivor benefit basics:

When a spouse dies, the survivor receives the deceased spouse’s actual monthly benefit — including any Delayed Retirement Credits earned. If the higher earner delayed to 70 and was receiving $3,500 per month, the surviving spouse receives $3,500 per month (subject to their own age at the time they claim the survivor benefit).

This is the most powerful argument for the higher earner to delay. It provides inflation-adjusted, lifetime income security for the surviving spouse who — statistically — will live significantly longer.

The 62/70 split strategy for couples:

The lower earner claims at 62, providing immediate household income. The higher earner delays to 70, maximizing both the couple’s total lifetime income and the survivor benefit. This is the most commonly recommended strategy for married couples with a meaningful earnings gap — not because it is the only answer, but because it is the best starting point for the analysis.

Key Takeaway for Married Couples: The higher earner delaying to 70 is not just a bet on their own longevity. It is a financial protection strategy for the surviving spouse — who may collect that higher benefit for 20 or more years after the higher earner passes. This single factor changes the optimal strategy for most married couples, even those who initially assume the higher earner should claim early.

Common Social Security Claiming Mistakes to Avoid

These are not hypothetical errors. They are the mistakes financial planners see repeatedly — and every one of them is entirely avoidable.

Mistake 1 — Claiming automatically at 62 because “that’s when you can”

Eligibility at 62 is not a recommendation. For someone in good health with a 25-year retirement horizon, claiming at 62 can cost hundreds of thousands of dollars in lifetime benefits. The decision deserves the same deliberate analysis you would give any six-figure financial commitment.

Mistake 2 — Not coordinating with your spouse

Treating Social Security as two independent decisions in a marriage almost always leaves money on the table. Spousal and survivor benefit coordination can significantly change the optimal claiming age for both partners — often pushing the higher earner toward delay even when they personally would prefer to claim early.

Mistake 3 — Ignoring the earnings test while working

Claiming before FRA while earning above $22,320 per year creates cash flow disruption and administrative complexity. If you plan to keep working at a meaningful income level, wait until at least FRA to claim.

Mistake 4 — Forgetting the survivor benefit

The higher earner delaying to 70 is not just about their own lifetime income. It is about protecting the surviving spouse with a larger permanent benefit for potentially decades. This factor alone changes the optimal strategy for most married couples.

Mistake 5 — Not checking your SSA earnings record for errors

Your benefit is calculated from your 35 highest-earning years on record at the Social Security Administration. Errors in your earnings record — missing years, incorrect amounts — directly reduce your benefit. Check your account at ssa.gov/myaccount annually and dispute any discrepancies before you claim.

Mistake 6 — Assuming Social Security won’t exist

The Social Security trust fund faces projected shortfalls — but the system will not disappear. Even under the worst-case scenario without legislative changes, Social Security is projected to pay approximately 77% of scheduled benefits from payroll tax revenue alone. Planning as if Social Security will pay zero leads to over-saving at the expense of your quality of life today.

Common Mistake to Avoid: Claiming Social Security the same month you retire without running the numbers first. Retirement and Social Security claiming are two completely separate decisions. You can retire at 63 and claim at 70. Many people do not realize this — and conflating the two decisions costs them significantly.

How to Get Your Personalized Social Security Estimate — Step by Step

Understanding the strategy is step one. Applying it to your actual numbers is step two. Here is exactly how to do that.

Step 1 — Create your my Social Security account

Go to ssa.gov/myaccount. Setup takes approximately 10–15 minutes to verify your identity. Anyone aged 18 and older can create an account — you do not need to be near retirement to access your statement.

Step 2 — Review your earnings record

Your Social Security statement shows every year of earnings on record. Verify that all years are listed and the amounts look correct. Missing or incorrect years directly reduce your projected benefit. Dispute errors by contacting the SSA with supporting documentation — W-2s or tax returns.

Step 3 — Note your benefit estimates at 62, FRA, and 70

The statement provides projected monthly benefits at each major claiming age. These estimates assume you continue earning at your current income level until retirement. If you plan to retire early, your actual benefit will be slightly lower than what the statement shows.

Step 4 — Run the break-even calculation

Use the SSA’s break-even tool or the formula from the earlier section with your actual numbers. Compare 62 vs. FRA vs. 70 scenarios side by side. Once you have real numbers in front of you, the decision often becomes significantly clearer.

Step 5 — Model the spousal scenario (if married)

Have your spouse pull their benefit estimates too. Model the combined household income under different claiming combinations — both at 62, both at 70, the split strategy, and variations in between.

Pro Tip: The free tool at opensocialsecurity.com allows you and your spouse to input your benefit estimates and life expectancy assumptions and see the optimal claiming combination. It takes about five minutes and models hundreds of scenarios simultaneously — one of the most valuable free tools in retirement planning.

If your retirement number calculation shows you are heavily reliant on Social Security to meet your income target, this step is not optional. Get the actual numbers before making any decision.

FAQs About the Best Age to Claim Social Security

Is it ever smart to claim Social Security at 62?

Yes — claiming at 62 is the right decision in specific circumstances. If you have serious health issues that reduce your life expectancy, if you have been laid off and have minimal savings, or if you are the lower earner in a marriage where your spouse plans to delay, claiming early can be mathematically sound. The key is making the decision deliberately based on your situation — not simply because 62 is when you become eligible.

What happens if I claim early and then keep working?

If you claim before your Full Retirement Age and earn more than $22,320 in 2026, the SSA will withhold $1 in benefits for every $2 you earn above that threshold. These withheld benefits are not permanently lost — they are recredited to your account when you reach FRA, permanently increasing your monthly benefit. In the year you reach FRA, the threshold increases significantly and the reduction formula changes.

Can I change my mind after claiming Social Security?

Yes, but only within the first 12 months. If you claimed Social Security and want to undo that decision, you can file Form SSA-521 to withdraw your application — but you must repay every dollar of benefits you and any dependents received. After 12 months, the decision is permanent. There is one partial exception: at your Full Retirement Age, you can voluntarily suspend your benefits without repaying them to earn Delayed Retirement Credits until age 70.

Does delaying Social Security affect my Medicare enrollment?

No. Medicare eligibility begins at 65 regardless of when you claim Social Security. However, if you are not yet receiving Social Security when you turn 65, you must proactively enroll in Medicare during your 7-month initial enrollment window. Failing to enroll on time results in permanent premium penalties.

How does inflation affect the claiming age decision?

Social Security benefits receive annual Cost of Living Adjustments (COLAs) regardless of when you claim — but a higher starting benefit means the COLA applies to a larger base. A person receiving $2,480 per month at age 70 receives significantly more from any given COLA increase than a person receiving $1,400 per month from age 62. This gap widens further every year inflation runs, making the lifetime income difference even larger than the simple 20-year table above suggests.

Is it true Social Security is going broke?

No — this is one of the most persistent myths in retirement planning, and we debunk it in detail in 10 Retirement Myths Debunked. The trust fund faces a projected shortfall — not a shutdown. Even without any legislative changes, payroll tax revenue is sufficient to pay approximately 77% of scheduled benefits indefinitely. Congressional action, which has addressed every prior shortfall in the program’s history, would likely push that figure back toward 100%.

The Bottom Line

You came into this post knowing the difference could be significant. You are leaving with the exact formula for calculating your own version of that number — and a five-factor framework for knowing which answer actually applies to you.

Three things worth carrying with you:

- There is no universally correct claiming age. The right answer depends on your health, finances, marital status, and tax situation. Anyone who tells you to always wait or always claim early is skipping the analysis that actually matters.

- The survivor benefit is the most underweighted factor in most couples’ claiming decisions. The higher earner delaying to 70 protects both spouses — not just the one who delays. This factor alone changes the optimal strategy for most married households.

- The single best action you can take today is creating your my Social Security account at ssa.gov and pulling your actual benefit numbers. Everything else in this guide becomes concrete once you have your real numbers in front of you.

If you have not yet taken the retirement readiness quiz, that is a useful next step — it scores your Social Security preparedness alongside your savings, healthcare planning, and income strategy, and gives you a clear picture of which areas need the most attention before you retire.

The best age to claim Social Security isn’t 62 or 67 or 70 — it’s the age you arrive at after doing the math, honestly, with your own numbers.

Disclaimer: The content on RetireWealthPath.com is for informational and educational purposes only and does not constitute financial, tax, or legal advice. We are not licensed financial advisors. Social Security rules, benefit amounts, earnings test thresholds, and tax treatment referenced in this article reflect 2026 guidelines and are subject to change by legislation or SSA policy. Break-even calculations and benefit examples are for illustrative purposes only and do not represent guaranteed outcomes. Individual Social Security benefits vary based on your personal earnings history. Always consult a qualified financial professional or Social Security specialist before making claiming decisions. Retirement planning involves risk and individual results will vary.