Retirement planning vocabulary guide [60 Terms Explained]

The first time someone mentioned “RMDs” at a retirement seminar, half the room nodded as if they understood. Most didn’t. Neither did I.

That moment captures something frustrating and almost universal: retirement planning language was built by financial professionals for other financial professionals — not for regular people trying to make smart decisions about their futures. The terminology isn’t just confusing; it’s exclusionary by design.

This retirement planning vocabulary guide is your decoder ring. Bookmark this page and return to it every time a confusing term crosses your path. Understanding these terms isn’t just academic — it directly affects when you claim Social Security, how much you pay in taxes, and how much wealth reaches your heirs.

When you understand what you’re being offered, warned about, or sold, you make genuinely better decisions. The difference between a good retirement and a financially stressful one often comes down to knowing what these words actually mean.

Let’s start with the accounts — because everything in retirement planning flows from where your money lives.

Retirement Account Terms — Where Your Money Lives

Most people have heard these terms. Fewer have crisp definitions. Here is what you actually need to know.

The Core Accounts

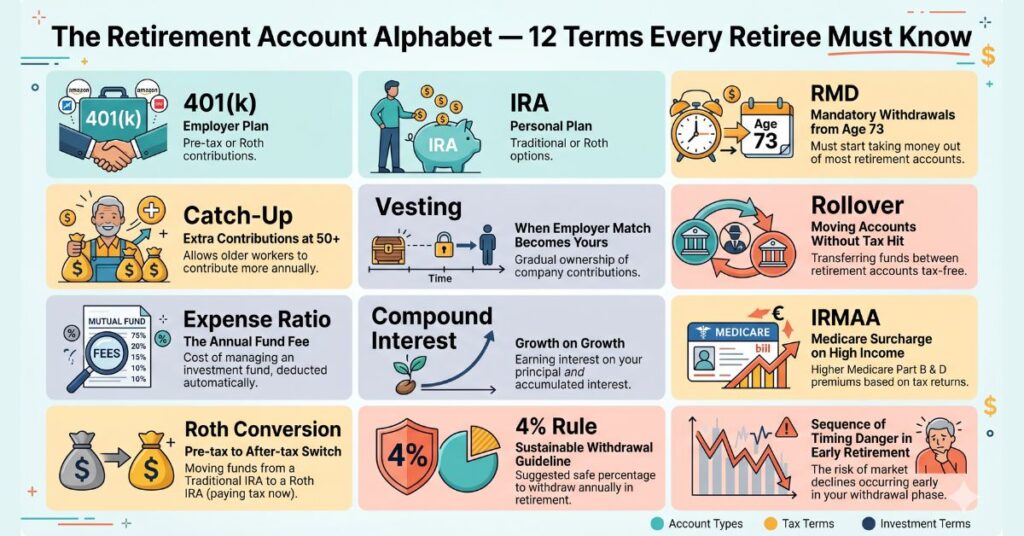

401(k)

A retirement savings account sponsored by your employer. You contribute pre-tax dollars (traditional) or after-tax dollars (Roth), and the money grows tax-advantaged until withdrawal. In 2026, you can contribute up to $23,500 per year, or $31,000 if you are 50 or older. If your employer offers a match, this is the first account you should fund.

403(b)

The 401(k) equivalent for employees of public schools, nonprofits, and certain tax-exempt organizations. Same contribution limits, same basic structure — just a different name tied to a different employer type. If you work in education or the nonprofit sector, this is your version of the 401(k).

457(b)

A deferred compensation plan available to state and local government employees. One significant advantage over 401(k)s: withdrawals before age 59½ are penalty-free if you separate from your employer. That flexibility makes it a powerful tool for government workers planning an early retirement.

Traditional IRA (Individual Retirement Account)

A personal retirement account you open yourself, completely independent of your employer. Contributions may be tax-deductible depending on your income and whether you have a workplace plan. Withdrawals in retirement are taxed as ordinary income. The 2026 contribution limit is $7,000 per year.

Roth IRA

Like a traditional IRA, but funded with after-tax dollars. The payoff: qualified withdrawals in retirement are completely tax-free — including all the growth. There are no required minimum distributions during the account owner’s lifetime, making the Roth IRA one of the most flexible and powerful accounts in retirement planning.

SEP IRA (Simplified Employee Pension)

A retirement account designed for self-employed individuals and small business owners. Contribution limits are significantly higher than a standard IRA — up to 25% of compensation or $69,000 in 2026, whichever is less. If you run your own business, a SEP IRA is one of the fastest ways to build tax-advantaged wealth.

Solo 401(k)

A 401(k) plan for self-employed people with no employees other than a spouse. It combines both employee and employer contribution limits, allowing higher annual contributions than a SEP IRA in many income scenarios. A strong choice for self-employed individuals with higher incomes.

SIMPLE IRA

A Savings Incentive Match Plan for Employees — a retirement plan designed for small businesses with 100 or fewer employees. Easier to administer than a full 401(k) and requires employer matching. The 2026 contribution limit is $16,500, with a $3,500 catch-up for those 50 and older.

Pro Tip: You can contribute to both a 401(k) through your employer and a Roth IRA independently — as long as your income falls within Roth IRA eligibility limits ($161,000 for single filers in 2026). Doing both simultaneously is one of the most powerful wealth-building moves available to a working person.

Account Access and Ownership Terms

Beneficiary

The person or entity you designate to receive your retirement account when you die. Critically important: beneficiary designations override your will entirely. If you named an ex-spouse 15 years ago and never updated the form, they may still legally receive your 401(k). Review your beneficiary designations annually, especially after major life changes like marriage, divorce, or the birth of a child.

Custodian

The financial institution that holds and administers your retirement account — a brokerage like Fidelity, Vanguard, or Schwab. The custodian does not manage your investments or make decisions on your behalf; it simply holds the assets.

Rollover

Moving money from one retirement account to another — for example, from an old employer’s 401(k) into an IRA — without triggering taxes or penalties, as long as the transfer is completed correctly within 60 days, or done via direct transfer.

Trustee-to-Trustee Transfer

The cleanest way to move retirement funds: your old custodian sends the money directly to your new custodian. You never touch the funds, eliminating any risk of accidentally triggering taxes or penalties. When changing jobs or consolidating accounts, always request this method first.

Contribution and Limit Terms — How Much You Can Save

These terms have real dollar consequences. People who don’t understand them leave significant money on the table every single year.

Contribution Limit

The maximum amount the IRS allows you to put into a retirement account each year. These limits are adjusted periodically for inflation. In 2026: the 401(k) limit is $23,500 and the IRA limit is $7,000.

Catch-Up Contribution

An additional amount people aged 50 and older can contribute beyond the standard limit. In 2026: an extra $7,500 for 401(k)s (bringing the total to $31,000) and an extra $1,000 for IRAs (bringing the total to $8,000). If you are in your 50s and behind on savings, this is one of the most important numbers in retirement planning.

Super Catch-Up Contribution

Introduced under the SECURE 2.0 Act: employees aged 60 to 63 can contribute an even higher catch-up amount to their 401(k) — $11,250 extra in 2026 instead of the standard $7,500. This applies only to workplace plans like 401(k)s and 403(b)s, not IRAs. If you are in this age window, the opportunity is substantial.

Employer Match

Free money your employer adds to your 401(k) based on your own contributions. A common formula: a 100% match on the first 3% of your salary you contribute. If you earn $60,000 and contribute 3% ($1,800), your employer adds another $1,800. Not contributing enough to capture the full employer match is leaving guaranteed compensation on the table.

Vesting Schedule

The timeline over which you gain full ownership of your employer’s matching contributions. You always own 100% of what you personally contribute — immediately and permanently. But employer contributions may vest over 2 to 6 years. Leaving a job before you are fully vested means forfeiting some or all of that employer money. Always check your vesting status before resigning.

2026 Retirement Contribution Limits at a Glance

| Account Type | Standard Limit | Age 50+ Catch-Up | Age 60–63 Super Catch-Up |

|---|---|---|---|

| 401(k) / 403(b) | $23,500 | +$7,500 → $31,000 | +$11,250 → $34,750 |

| Traditional / Roth IRA | $7,000 | +$1,000 → $8,000 | Not applicable |

| SEP IRA | 25% of comp / $69,000 | Not applicable | Not applicable |

| SIMPLE IRA | $16,500 | +$3,500 → $20,000 | Not applicable |

| HSA (Individual) | $4,300 | +$1,000 → $5,300 (age 55+) | Not applicable |

Source: IRS.gov — 2026 retirement plan contribution limits. Figures subject to annual adjustment.

Investment Terms — How Your Money Grows

Many retirees have retirement accounts but don’t fully understand the investments inside them. These definitions close that gap.

Asset Allocation

The percentage of your portfolio divided among different asset classes — typically stocks, bonds, and cash. A common rule of thumb: subtract your age from 110 to get your target stock percentage. A 60-year-old would hold roughly 50% stocks and 50% bonds — though modern planning often suggests holding more stocks given longer life expectancies.

Diversification

Spreading investments across many different assets so that the poor performance of one doesn’t devastate your entire portfolio. Owning 500 different stocks through a broad index fund is diversified. Owning stock only in your employer’s company is not. Diversification is one of the few free lunches in investing.

Index Fund

A fund that tracks a market index — like the S&P 500 — rather than being actively managed by a fund manager. Because no one is making daily trading decisions, fees are extremely low. Historically, most index funds outperform most actively managed funds over long time horizons. For most retirement investors, low-cost index funds are the default best choice.

ETF (Exchange-Traded Fund)

Similar to an index fund, but traded on a stock exchange like an individual stock — you can buy and sell throughout the trading day. Most ETFs are passively managed and low-cost. For practical purposes inside a retirement account, ETFs and index funds serve similar functions.

Expense Ratio

The annual fee a fund charges, expressed as a percentage of your investment. A 0.03% expense ratio on a $100,000 portfolio costs $30 per year. A 1.0% expense ratio costs $1,000 per year. That $970 annual difference, compounded over 30 years, adds up to tens of thousands of dollars in lost wealth. Always check the expense ratio before investing in any fund.

Target-Date Fund

A “set it and forget it” fund designed for a specific retirement year — for example, a “2030 Fund” for someone retiring around 2030. The fund automatically shifts from aggressive (more stocks) to conservative (more bonds) as the target date approaches. Ideal for investors who don’t want to manage their own asset allocation over time.

Rebalancing

Periodically adjusting your portfolio back to your target allocation. If stocks grow and now represent 75% of your portfolio instead of your intended 60%, rebalancing means selling some stocks and buying more bonds to restore the balance. Most financial advisors recommend rebalancing once or twice per year.

Return and Risk Terms

Compound Interest

Earning returns not just on your original investment, but on the returns themselves. $10,000 invested at 7% annual return grows to $76,123 in 30 years — without adding another dollar. The longer your money compounds, the more dramatic the results. This is why starting early matters so profoundly — every year of delay is a year of compounding you never recover.

Sequence of Returns Risk

The danger that poor investment returns early in retirement can permanently damage your portfolio, even if average returns over the full period are acceptable. A 30% market crash in year one of retirement is far more damaging than the same crash in year 20, because early withdrawals force you to sell assets at depressed prices before they recover. This risk is a key reason why retirement income planning is more complex than simply accumulating savings.

Volatility

The degree to which an investment’s value fluctuates. High volatility (like individual stocks) means bigger swings up and down. Low volatility (like short-term bonds) means steadier, smaller movements. The right level depends entirely on your time horizon and personal tolerance for market swings — neither is inherently good or bad.

Common Mistake: Many people confuse “risk” with “losing money.” In investing, risk also includes the risk of NOT growing enough to outpace inflation. A savings account feels safe but loses purchasing power every year that inflation exceeds its interest rate. Real risk management means balancing both sides of the equation.

Tax Terms — What the Government Takes (and How to Minimize It)

Tax literacy in retirement is underrated. People who understand these terms make dramatically better decisions about when to convert, when to withdraw, and how to sequence income in retirement.

Tax-Deferred

Growth that is not taxed until you withdraw the money. Traditional 401(k)s and IRAs are tax-deferred — you pay taxes on withdrawals in retirement, not on contributions or growth along the way. The benefit: your money grows on a larger base because taxes are postponed.

Tax-Free

Growth and withdrawals that are never taxed. Roth accounts, after meeting qualification requirements, are completely tax-free. HSAs used for qualified medical expenses are also tax-free. These accounts are most valuable when you expect to be in a higher tax bracket in retirement than you are today.

Tax-Advantaged

An umbrella term for any account that receives favorable tax treatment — whether tax-deferred, tax-free, or tax-deductible. 401(k)s, IRAs, HSAs, and 529 education accounts are all tax-advantaged. Maximizing contributions to these accounts should be the foundation of any retirement savings strategy.

Ordinary Income

Income taxed at your regular federal income tax rate — the same brackets that apply to your paycheck. Traditional 401(k) and IRA withdrawals are taxed as ordinary income in retirement. Large withdrawals can push you into higher tax brackets, making withdrawal strategy critically important.

Capital Gains

Profit from selling an investment that has grown in value. Long-term capital gains (assets held more than one year) are taxed at 0%, 15%, or 20% — significantly lower than ordinary income rates. Retirees in lower income brackets can often harvest capital gains at the 0% rate, effectively locking in investment profits tax-free.

Roth Conversion

The process of moving money from a traditional pre-tax retirement account into a Roth after-tax account. You pay income taxes on the converted amount now, in exchange for tax-free withdrawals later. Strategic conversions in low-income years — such as early retirement before Social Security or RMDs begin — can significantly reduce your lifetime tax burden.

Tax Bracket

The rate at which portions of your income are taxed. The US uses a marginal progressive system — only the income within each bracket is taxed at that rate, not all of your income. In 2026, federal brackets range from 10% to 37%. Many retirees find themselves in lower brackets than during their peak earning years, creating valuable windows for strategic tax planning.

IRMAA (Income-Related Monthly Adjustment Amount)

A Medicare premium surcharge added when a retiree’s income exceeds certain thresholds. In 2026, single filers with income above $106,000 pay higher Medicare Part B and Part D premiums. Critically, IRMAA is calculated on income from two years prior — meaning a large Roth conversion in 2024 could trigger higher Medicare premiums in 2026. One of the most commonly overlooked retirement tax traps.

Pro Tip: The years between retiring and turning 73 — when Required Minimum Distributions begin — are often the lowest-tax years of your life. Use this window to do Roth conversions, harvest capital gains at the 0% rate, and restructure your income before RMDs force distributions that push you into higher brackets. Waiting until 73 to think about this is an expensive mistake.

Withdrawal and Distribution Terms — Getting Your Money Out

Most people understand how to put money into retirement accounts. Far fewer understand the rules and strategy for getting it out. This section is where costly mistakes are prevented.

Required Minimum Distribution (RMD)

The minimum amount the IRS requires you to withdraw annually from traditional retirement accounts starting at age 73 (as of 2026 under SECURE 2.0). The amount is calculated each year by dividing your account balance by an IRS life expectancy factor. Failing to take your full RMD triggers a 25% penalty on the amount you should have withdrawn — reduced to 10% if you correct the mistake within two years.

Qualified Distribution

A withdrawal from a Roth account that meets IRS requirements and is therefore completely tax-free. To qualify: the account must be at least 5 years old and you must be 59½ or older (with exceptions for disability or a first-time home purchase up to $10,000). Understanding this rule ensures you never accidentally trigger taxes on Roth withdrawals.

Early Withdrawal Penalty

A 10% federal tax penalty on retirement account withdrawals made before age 59½, on top of regular income taxes owed. Several exceptions exist — including permanent disability, substantially equal periodic payments (rule 72(t)), and first-time home purchase from an IRA. The penalty is significant enough that it should rarely be triggered voluntarily.

72(t) Distributions

A method for accessing retirement funds before age 59½ without the 10% penalty, by taking Substantially Equal Periodic Payments (SEPPs) based on your life expectancy. You must continue these payments for at least 5 years or until you reach 59½, whichever is longer. Modifying or stopping payments early triggers back-penalties on all previous distributions — this strategy requires careful, upfront planning.

The 4% Rule

A widely cited guideline suggesting retirees can withdraw 4% of their portfolio in year one of retirement, adjust that amount for inflation each subsequent year, and have a high probability of not outliving their money over a 30-year retirement. Originally based on the 1994 Trinity Study. Modern research suggests adjustment may be needed given lower expected future returns and longer life expectancies — but it remains a useful starting benchmark.

Withdrawal Sequencing

The strategic order in which you draw from different account types to minimize lifetime taxes. The conventional wisdom: spend from taxable accounts first, then tax-deferred accounts, then tax-free Roth accounts last. The optimal sequence depends on your specific tax situation, income sources, and goals — one of the highest-value areas where a financial advisor adds real value.

Social Security and Benefits Terms — Government Income Explained

Social Security is the single most important income source for most retirees — yet its terminology is widely misunderstood. Getting these definitions right can mean the difference between claiming optimally and leaving tens of thousands of dollars permanently on the table.

Full Retirement Age (FRA)

The age at which you qualify for 100% of your Social Security benefit. For anyone born in 1960 or later, FRA is age 67. Claiming before FRA permanently reduces your monthly benefit. Claiming after FRA — up to age 70 — permanently increases it. This decision is one of the most consequential financial choices most retirees will ever make.

Primary Insurance Amount (PIA)

The monthly Social Security benefit you receive if you claim exactly at your Full Retirement Age. Your PIA is calculated from your 35 highest-earning years. Years with zero earnings count as zeros in the calculation — which is why extended gaps in work history reduce your benefit. You can view your estimated PIA at any time at ssa.gov.

Spousal Benefit

A Social Security benefit available to a married person based on their spouse’s earnings record, worth up to 50% of the spouse’s Primary Insurance Amount. Available even to a spouse who never worked, as long as the working spouse has already claimed their own benefit. Essential to understand for married couples making coordinated claiming decisions.

Survivor Benefit

The benefit a widow or widower receives after a spouse dies — worth up to 100% of what the deceased spouse was receiving. Survivor benefits and spousal benefits are separate programs with different claiming rules and different strategies. The age at which you claim survivor benefits can significantly affect lifetime household income.

Delayed Retirement Credits

The bonus you earn by delaying Social Security past your Full Retirement Age. For each year you delay up to age 70, your benefit grows by 8% per year. Waiting from age 67 to age 70 adds 24% to your monthly benefit — permanently. For retirees who can afford to wait, delay is often the most powerful guaranteed investment available.

Earnings Test

If you claim Social Security before your Full Retirement Age and continue working, your benefits are temporarily reduced if your earnings exceed $22,320 in 2026. Benefits withheld are not lost — they are credited back as a higher monthly payment once you reach your Full Retirement Age. After FRA, you can earn any amount without any reduction in benefits.

Combined Income (for Social Security taxation)

The IRS formula used to determine how much of your Social Security benefit is subject to federal income tax: Adjusted Gross Income + Non-taxable interest + 50% of Social Security benefits. If this total exceeds $25,000 for a single filer or $32,000 for a married couple, up to 85% of your benefit may be taxable. Understanding this formula helps retirees plan withdrawals to minimize unnecessary Social Security taxation.

Healthcare and Insurance Terms — Protecting Your Wealth

Healthcare is the largest unplanned expense in retirement for most Americans. These definitions help you navigate a complex system before confusion becomes a costly mistake.

Medicare Part A — Hospital Insurance

Covers inpatient hospital stays, skilled nursing facility care, hospice, and some home health services. Most people pay no premium for Part A if they or their spouse worked and paid Medicare taxes for at least 10 years (40 quarters). Deductibles and coinsurance still apply at point of use — Part A is not entirely free.

Medicare Part B — Medical Insurance

Covers doctor visits, outpatient care, preventive services, and some home health care. The standard monthly premium in 2026 is $185 per month. Part B covers 80% of approved costs after the annual deductible — the remaining 20% is your responsibility unless you have supplemental coverage.

Medicare Part C — Medicare Advantage

Private insurance plans that bundle Parts A, B, and usually Part D into one plan. Often includes dental, vision, and hearing benefits that traditional Medicare does not cover. Plans vary significantly by region and carrier — always compare carefully before enrolling.

Medicare Part D — Prescription Drug Coverage

Available as a standalone plan paired with original Medicare, or bundled into a Medicare Advantage plan. Each plan has a formulary — a list of covered drugs — that varies by plan. Choosing the right Part D plan based on your specific medications can save hundreds of dollars annually.

Medigap (Medicare Supplement Insurance)

Private insurance that covers the “gaps” left by original Medicare — primarily the 20% co-insurance under Part B and the Part A inpatient deductible. Requires a separate monthly premium but dramatically reduces unpredictable out-of-pocket exposure. Pairs with original Medicare Parts A and B — not with Medicare Advantage.

HSA (Health Savings Account)

A triple-tax-advantaged account available to people enrolled in a qualifying High-Deductible Health Plan (HDHP). Contributions are pre-tax, growth is tax-free, and withdrawals for qualified medical expenses are tax-free. After age 65, HSA funds can be used for any purpose — taxed as ordinary income for non-medical use — making it a powerful stealth retirement account for those who can afford to let balances grow.

Long-Term Care

Assistance with activities of daily living — bathing, dressing, eating, mobility — due to aging, illness, or disability. Long-term care is not covered by Medicare except briefly for skilled nursing following a qualifying hospital stay. Facility care can cost $5,000 to $9,000 per month or more depending on location. Planning for this risk is one of the most underaddressed areas of retirement planning.

Common Mistake: Many people assume Medicare enrollment is automatic at 65. It is not. You must actively enroll during a 7-month window around your 65th birthday. Missing this window without qualifying coverage elsewhere can result in permanent late-enrollment premium penalties that follow you for life.

Estate Planning Terms — Protecting What You’ve Built

Estate planning vocabulary tends to make people avoid the topic entirely. Plain definitions make it approachable — and approachable means people actually act on it.

Will (Last Will and Testament)

A legal document specifying how you want your assets distributed after death and, if you have minor children, who should serve as their guardian. A will must go through probate — the public court process of validating the document and distributing assets. Without a will, your state’s intestacy laws determine who gets what.

Revocable Living Trust

A legal arrangement where you transfer assets into a trust you control during your lifetime. At death, assets transfer to your beneficiaries without going through probate — faster, private, and often simpler for heirs. “Revocable” means you can change or cancel it anytime while you are alive. Recommended for people with significant assets, real estate in multiple states, or a strong preference for privacy.

Power of Attorney (POA)

A legal document authorizing someone — your designated “agent” — to make financial and legal decisions on your behalf if you become incapacitated. A durable Power of Attorney remains valid even if you become mentally incapacitated, which is a critical distinction from a standard POA that terminates upon incapacity. Every adult should have one.

Healthcare Directive (Living Will)

A legal document stating your wishes for medical treatment if you cannot communicate them — including preferences about life-sustaining treatment, resuscitation, and organ donation. Prevents family members from having to make agonizing decisions without guidance and ensures your wishes are legally honored.

Probate

The court-supervised process of validating a will and distributing a deceased person’s assets. Probate is a matter of public record, can take months or years, and often involves legal fees that reduce the estate. Assets with named beneficiaries — including IRAs, 401(k)s, and life insurance — and assets held in a trust bypass probate entirely.

Step-Up in Basis

A tax rule that resets the cost basis of inherited assets to their fair market value at the time of death. If a parent purchased stock for $10,000 that grew to $100,000 by the time of their death, an heir who sells that stock immediately owes capital gains tax on zero gain — not on the $90,000 of growth that occurred during the original owner’s lifetime. One of the most significant tax benefits available in estate planning.

QCD (Qualified Charitable Distribution)

A direct transfer of up to $105,000 per year (2026 limit) from an IRA to a qualified charity, available to account holders age 70½ or older. QCDs count toward satisfying your RMD requirement for the year and are excluded from your taxable income entirely — making them one of the most tax-efficient ways for retirees to give. If you plan to donate anyway, always consider a QCD before writing a personal check.

Pro Tip: Beneficiary designations on retirement accounts and life insurance policies override your will entirely. A 10-minute review of every account’s beneficiary designation is one of the highest-value estate planning actions you can take today — at absolutely zero cost. Do it now, not later.

FAQs About Retirement Planning Vocabulary

What is the most important retirement planning term for a beginner to understand first?

Start with compound interest. Everything else in retirement planning — contribution limits, account types, investment strategy — is ultimately in service of maximizing how long and how effectively compound interest works for you. Once you understand that growth builds on itself over time, the urgency of starting early becomes immediately and permanently clear.

What’s the difference between a 401(k) and an IRA?

A 401(k) is offered through your employer, often comes with an employer match, and has higher contribution limits ($23,500 in 2026). An IRA is opened independently at a brokerage of your choice, has lower contribution limits ($7,000 in 2026), but typically offers a wider range of investment choices and more flexibility. Ideally, contribute to both — capturing the full employer match in your 401(k) first, then funding a Roth IRA up to the annual limit.

What does “vesting” mean and why does it matter?

Vesting refers to your ownership of employer-contributed funds in your 401(k). You always own 100% of your own contributions immediately and permanently. But your employer’s matching contributions may only belong to you fully after staying at the company for 2 to 6 years, depending on the plan. Leaving before you are fully vested means forfeiting some or all of that employer money. Always check your vesting status before resigning.

What is an RMD and what happens if I miss it?

A Required Minimum Distribution is the amount the IRS requires you to withdraw annually from traditional retirement accounts starting at age 73. The penalty for missing an RMD is 25% of the amount you should have withdrawn — reduced to 10% if corrected within two years. The IRS calculates your RMD amount each year based on your account balance and a published life expectancy table.

What’s the difference between Medicare and Medicaid?

Medicare is federal health insurance for people 65 and older — available regardless of income level. Medicaid is a joint federal-state program for people with low income and limited assets. Medicaid covers long-term care expenses that Medicare does not, but qualification requires meeting strict income and asset limits that vary significantly by state. They sound similar but serve very different populations and purposes.

What is a Roth conversion and should I do one?

A Roth conversion moves money from a traditional pre-tax account into a Roth after-tax account. You pay income taxes on the converted amount now, in exchange for tax-free withdrawals later. Whether you should do one depends on your current tax bracket, your expected tax bracket in retirement, and your timeline. The best window is typically the years between retiring and age 73, when your income is often at its lowest. A fee-only financial advisor can run the numbers for your specific situation.

The Bottom Line

You came into this post with a list of terms that might have seemed intimidating. You are leaving with clear, working definitions for over 60 of the most important concepts in retirement planning — from the accounts where your money lives, to the tax rules that govern how it grows, to the estate documents that protect what you have built.

Here are the three terms worth carrying with you above all others:

- Compound interest — why starting now matters more than starting perfectly

- Roth IRA — often the single best first account for long-term, tax-free wealth building

- RMD — the tax reality that makes planning ahead so important, starting decades before age 73

Save this page — you will want to come back to it every time a new financial term crosses your path. Every term you understand is one less way someone can confuse, mislead, or overcharge you.

Ready to put these terms into action? Start with Why Retire Wealth Planning Starts Now, or explore our guide on how to set your retirement number to see how these concepts work in real-world planning.

Financial jargon was never designed to help you — but understanding it puts you firmly in the driver’s seat of your own retirement.

Disclaimer: The content on RetireWealthPath.com is for informational and educational purposes only and does not constitute financial, tax, or legal advice. We are not licensed financial advisors. The information provided may not apply to your specific situation. Contribution limits, tax rules, and benefit amounts referenced reflect 2026 figures and are subject to change. Always consult a qualified financial professional, tax advisor, or attorney before making any financial decisions. Retirement planning involves risk and individual results will vary.