Backdoor Roth IRA [Step-by-Step Guide for High Earners]

If your income exceeds $165,000 as a single filer or $246,000 as a married couple in 2026, the IRS says you cannot contribute directly to a Roth IRA. What the IRS does not say is that you cannot get money into a Roth IRA. The backdoor Roth IRA is the legal, IRS-sanctioned method that high earners use to access tax-free retirement growth — and it has been available since 2010.

This is not a loophole. It is not a gray area. The strategy was explicitly acknowledged and approved by the Joint Committee on Taxation in its 2010 technical explanation, and millions of Americans have used it without issue ever since. Congress opened the door. The IRS provided instructions on how to walk through it. Form 8606 is the key.

The stakes are real: high earners who skip the backdoor Roth IRA are permanently forgoing $8,000 per year in tax-free retirement space. At 7% annual growth over 15 years, that is approximately $201,000 in completely tax-free wealth — gone forever, because prior years’ contribution room cannot be made up retroactively.

This guide covers every step, every form, every timing decision, and every potential complication — including the pro-rata rule, the most dangerous and most misunderstood element of the strategy. Done correctly, the backdoor Roth IRA takes 30 minutes per year. Done incorrectly, it creates unexpected four-figure tax bills. You are about to understand exactly how to do it correctly.

Before we walk through the steps, let’s confirm you actually need the backdoor strategy — because if your income is below the thresholds, the direct route is simpler and identical in outcome.

Do You Actually Need the Backdoor Roth? – Income Limits and Who Qualifies

The backdoor Roth IRA exists specifically because the IRS restricts who can contribute directly to a Roth IRA based on income. Before executing the strategy, confirm you are actually in the group that needs it.

The 2026 Roth IRA Income Limits

The ability to contribute directly to a Roth IRA phases out at the following Modified Adjusted Gross Income (MAGI) thresholds in 2026:

| Filing Status | Phase-Out Begins | Phase-Out Complete |

|---|---|---|

| Single / Head of Household | $150,000 | $165,000 |

| Married Filing Jointly | $236,000 | $246,000 |

| Married Filing Separately (lived with spouse) | $0 | $10,000 |

Between the phase-out start and the phase-out end, your maximum Roth IRA contribution is proportionally reduced. For a single filer earning exactly $157,500 — the midpoint of the $150,000–$165,000 window — the contribution is reduced by 50%, meaning the maximum direct contribution is $4,000 (or $4,000 of the $8,000 age-50+ limit). At or above $165,000 as a single filer, the direct Roth IRA contribution is zero.

What Is MAGI – and Why It Matters

Modified Adjusted Gross Income for Roth IRA purposes is your Adjusted Gross Income (AGI) plus specific add-backs: student loan interest deductions, traditional IRA deductions, foreign income exclusions, and a handful of others. For most W-2 employees without complex tax situations, MAGI is essentially equal to AGI from the first page of Form 1040.

One important nuance: pre-tax 401(k) contributions reduce AGI — and therefore MAGI. Contributing the maximum $23,500 to a pre-tax 401(k) in 2026 reduces your MAGI by $23,500. For someone earning $185,000, that single move drops MAGI to $161,500 — still above the single filer limit, but closer than you might expect. For someone earning $175,000, it drops MAGI to $151,500 — squarely in the partial phase-out zone where a reduced direct contribution is still available.

If you’re not certain where your MAGI lands, calculate it carefully before defaulting to the backdoor approach. You may have more direct access than you think — or you may realize the backdoor is not just useful but essential.

Understanding MAGI is one of those foundational concepts where our retirement planning vocabulary guide is genuinely useful — it covers MAGI, AGI, basis, and dozens of other terms that come up repeatedly in this strategy.

Who Needs the Backdoor Roth

- Single filers with MAGI above $165,000

- Married filers (filing jointly) with MAGI above $246,000

- Anyone married filing separately with meaningful income

Who Does NOT Need the Backdoor Roth

- Anyone below the phase-out thresholds — contribute directly to a Roth IRA

- High earners who want to contribute more than the Roth IRA limit — the Roth 401(k) has no income limits and accepts up to $31,000/year for age 50+ in 2026

- Note: the Roth 401(k) and the backdoor Roth IRA are complementary, not substitutes — both can be used in the same year

Introducing Jennifer — our case study throughout this guide:

Jennifer, 52, is a physician assistant earning $195,000 in 2026. Her MAGI is well above the $165,000 single filer limit — she cannot contribute directly to a Roth IRA. However, Jennifer has no existing traditional IRA balances. She is the ideal backdoor Roth IRA candidate. We will follow Jennifer through every step of the strategy.

Pro Tip: Before executing the backdoor Roth, calculate your exact MAGI for the tax year. Some high earners assume they are above the limit when they are actually in the partial phase-out zone — or can reduce their MAGI below the limit through pre-tax 401(k) contributions, HSA contributions, or other deductions. A quick MAGI calculation with a CPA can determine whether the direct Roth contribution route is still partially available — and may be worth $3,000–$4,000 in additional Roth space.

The Mechanics – How the Backdoor Roth IRA Works in Plain English

Before the step-by-step walkthrough, you need a conceptual map of what is actually happening — the “why it works” before the “how to do it.” Understanding the mechanics prevents the confusion that causes execution errors.

The Fundamental Two-Step Structure

The backdoor Roth IRA is not a special account type. It is a two-step process using standard IRS-recognized accounts:

Step A: Contribute to a traditional IRA using after-tax (non-deductible) dollars.

Step B: Convert that traditional IRA to a Roth IRA — paying tax only on any earnings that accumulated between the contribution and the conversion.

That is the entire strategy. Two steps, two accounts, one clean result.

Why This Works – The Tax Logic

The income limits that restrict direct Roth IRA contributions do not apply to traditional IRA contributions. Anyone with earned income can contribute to a traditional IRA regardless of income level.

The income limits for Roth IRA contributions also do not apply to Roth IRA conversions. Anyone can convert any amount from a traditional IRA to a Roth IRA, regardless of income.

By combining a traditional IRA contribution (no income limit) with a Roth conversion (no income limit), the net result is money in a Roth IRA — the same destination as a direct contribution, achieved through two steps instead of one.

The IRS’s Explicit Acknowledgment

The Joint Committee on Taxation’s 2010 technical explanation of the legislation that eliminated the $100,000 income limit on Roth conversions explicitly acknowledged that this approach would allow high earners to indirectly fund Roth IRAs. Congress did not close it. They permitted it. The IRS has since provided specific guidance on how to execute and report it — primarily through Form 8606.

The Tax Treatment of Each Step

Step A (non-deductible traditional IRA contribution): No current tax deduction, but also no current tax due. After-tax dollars go in, creating a “basis” in the traditional IRA — a record of the money you have already paid tax on.

Step B (conversion to Roth): Taxable only on the amount converted minus the after-tax basis already established in Step A. If the conversion happens immediately after the contribution settles (one to two days), virtually no earnings have accumulated — meaning the taxable amount is effectively zero.

The numbers in Jennifer’s case:

Jennifer contributes $8,000 to a traditional IRA on January 15, 2026. She converts the same $8,000 to a Roth IRA on January 17, 2026 — two days later. In two days, the money earned approximately $2.19 in a money market fund. Jennifer pays income tax on $2.19. That is her entire federal tax bill for the backdoor Roth contribution — approximately $0.48 at her 22% marginal rate. The $8,000 is now in her Roth IRA, growing completely tax-free for life.

What Makes This Complicated – The Pro-Rata Rule

The backdoor Roth works cleanly only when there are no pre-existing pre-tax traditional IRA balances. If you have pre-tax IRA funds sitting in traditional, SEP, or SIMPLE IRAs anywhere, the IRS pro-rata rule applies — and it will tax a proportional share of every conversion regardless of which specific funds you converted.

This is the central complication of the strategy, covered in full in the pro-rata rule section below. For now, the key point is this: before you contribute a single dollar, check your IRA balance situation. Jennifer’s clean slate — no existing pre-tax IRA balances — is what makes her situation simple. Yours may require an extra step first.

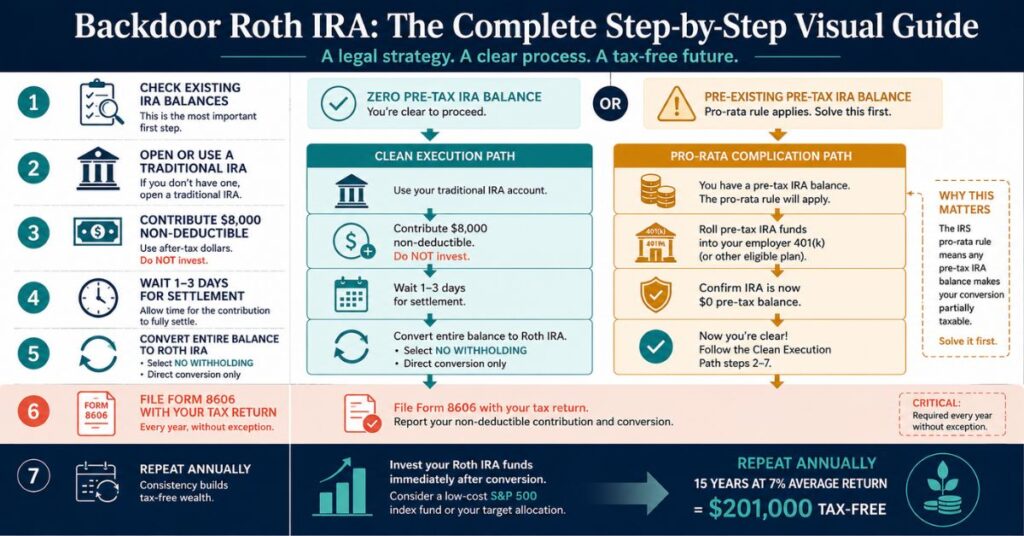

Step-by-Step Execution – The Complete Backdoor Roth IRA Process

This is the operational core of this guide. Every step, every form, every timing decision — spelled out with complete precision. Jennifer’s numbers run through every step consistently.

Step 1 – Open a Traditional IRA (If You Don’t Have One)

What to do: Open a traditional IRA at Fidelity, Vanguard, or Charles Schwab. All three offer no-fee accounts that can be opened entirely online in under 15 minutes. Choose the same brokerage where you have (or will open) your Roth IRA — keeping both at the same institution makes the conversion an internal transfer, eliminating delays, paperwork, and the risk of a 60-day rollover mishap.

The account type is simply “Traditional IRA” — not a rollover IRA, not a SEP IRA, not a SIMPLE IRA.

If you already have a traditional IRA at your chosen brokerage, you can use it — but read the pro-rata rule section first if it contains any pre-tax funds.

Timing: The traditional IRA can be opened and funded any time during the tax year (January 1 through December 31) or by the tax filing deadline the following year — typically April 15. IRA contributions for the 2026 tax year can be made as late as April 15, 2027. That said, January is the best time — more time in the Roth IRA means more tax-free compounding.

Jennifer’s Step 1:

Jennifer opens a traditional IRA at Fidelity on January 15, 2026. She already has a Roth IRA at Fidelity — opened years ago, unfunded, because her income exceeded the direct contribution limit. Both accounts are at the same institution. The conversion will be a simple internal transfer — no checks, no mail, no delays.

Step 2 – Make Your Non-Deductible Traditional IRA Contribution

What to do: Contribute the maximum allowable amount to your traditional IRA:

- $8,000 if you are age 50 or older (2026)

- $7,000 if you are under age 50 (2026)

This contribution is non-deductible — high earners above the IRA deductibility phase-out cannot claim a tax deduction for it. That is not a problem. In fact, it is exactly what you want: making a non-deductible contribution creates an after-tax “basis” in the traditional IRA, which is what makes the subsequent conversion essentially tax-free.

Critical: Do NOT invest the money once it lands in the traditional IRA. Leave it in the default money market or settlement fund. Every dollar invested inside the traditional IRA before conversion creates earnings that will be taxable when you convert. The goal is to convert before any meaningful earnings accumulate — ideally within 48 to 72 hours of settlement.

The per-person rule: Each spouse can independently execute the backdoor Roth. A married couple can together contribute $16,000 per year via backdoor Roth in 2026 ($8,000 each, assuming both are age 50 or older).

The earned income requirement: IRA contributions cannot exceed your earned income for the year. If you earn $8,000 or more in wages or self-employment income — which applies to virtually every high earner — you can contribute the full amount.

Jennifer’s Step 2:

Jennifer logs into her Fidelity account and transfers $8,000 from her bank checking account to her traditional IRA on January 15, 2026. She leaves the money in Fidelity’s default SPAXX money market fund and does not select any other investments. Her traditional IRA now shows a $8,000 balance — all after-tax, non-deductible.

Step 3 – Wait for the Contribution to Settle

What to do: Wait for the contribution to fully settle in the traditional IRA. ACH bank transfers typically take one to three business days.

Do not initiate the conversion before the funds have fully settled. A premature conversion attempt will be rejected or create administrative complications at your brokerage.

Why not wait longer? Every additional day the money sits in the traditional IRA, it earns a small amount of interest — typically $0.50 to $2.00 per day on $8,000 in a money market fund. Those earnings, however small, become taxable upon conversion. Waiting weeks or months before converting is needlessly expensive. Convert as soon as the funds settle.

Jennifer’s Step 3:

Jennifer’s $8,000 settles in her Fidelity traditional IRA by January 17, 2026. Two days of money market earnings: approximately $2.19. Jennifer is ready to convert.

Step 4 – Convert the Traditional IRA to a Roth IRA

What to do: Log into your brokerage and initiate a Roth IRA conversion. Navigation paths by institution:

- Fidelity: Accounts → Account Features → Convert to Roth IRA

- Vanguard: My Accounts → Transact → Convert to Roth IRA

- Schwab: Accounts → IRA Conversion → Convert Traditional to Roth

Convert the entire traditional IRA balance — including the small earnings that have accumulated since your contribution. Leaving any amount behind creates a partial-conversion complexity that you do not need.

Select “no withholding.” This is one of the most consequential decisions in the entire process. Electing withholding means the brokerage sends a portion of your conversion to the IRS on your behalf — but that withheld amount never reaches your Roth IRA. It reduces your Roth balance and may trigger an early withdrawal penalty on the withheld portion if you are under 59½. Pay any minimal conversion taxes (on $2.19 in earnings) from your regular savings at tax time. Never fund tax payments by shrinking your Roth.

Direct conversion vs. 60-day rollover: The direct conversion method — where the brokerage converts the funds internally — is the only method worth using for a backdoor Roth. The 60-day indirect rollover method (take a distribution, re-deposit within 60 days) triggers mandatory 20% withholding, requires you to make up the difference from outside funds, and introduces timing risk. Do not use it.

Jennifer’s Step 4:

On January 17, 2026, Jennifer logs into Fidelity and initiates a Roth IRA conversion of her entire traditional IRA balance: $8,002.19 ($8,000 contribution + $2.19 in money market earnings). She selects “convert entire balance” and “no withholding.” Fidelity confirms the conversion will complete within two business days. On January 19, Jennifer’s Roth IRA shows a balance of $8,002.19 — now growing completely tax-free.

Step 5 – Invest the Roth IRA Funds

What to do: Once the conversion completes, the funds land in your Roth IRA in the same money market or settlement fund — uninvested. Invest them immediately in your target allocation. A broad S&P 500 index fund, total market fund, or balanced fund are all appropriate starting points depending on your timeline and risk tolerance.

This step is critical and surprisingly often skipped. Money sitting in a Roth IRA money market fund earns roughly 4–5% per year. A diversified equity portfolio has historically returned 7–10% annually. Over 15 years, that gap compounds into a significant difference in tax-free retirement wealth.

Jennifer’s Step 5:

Jennifer immediately invests her $8,002.19 in Fidelity’s FXAIX (S&P 500 index fund, expense ratio 0.015%). Her Roth IRA is now fully invested and growing tax-free. She sets a calendar reminder for January 2027 to repeat the process for the next tax year.

Step 6 – File IRS Form 8606

What to do: File IRS Form 8606 with your federal income tax return for every year you execute a backdoor Roth IRA — no exceptions.

Part I of Form 8606 reports your non-deductible traditional IRA contribution and tracks your cumulative after-tax basis.

Part II of Form 8606 reports the Roth IRA conversion amount and calculates the taxable portion.

File by April 15, 2027 for the 2026 tax year (or October 15, 2027 if you file an extension — but the contribution itself must be made by April 15).

Why Form 8606 is non-negotiable: Without it, the IRS has no record of the after-tax basis you established in Step 2. In a future audit or upon retirement distribution, the IRS may treat the entire conversion as taxable — double-taxing money you have already paid tax on. The failure to file Form 8606 when required carries a $50 penalty — but the real risk is far larger: losing the documented proof of your after-tax basis.

What Form 8606 shows for Jennifer’s clean backdoor Roth:

| Form 8606 Line | Description | Jennifer’s Amount |

|---|---|---|

| Line 1 | Non-deductible contributions this year | $8,000 |

| Line 2 | Prior year cumulative basis (first year) | $0 |

| Line 3 | Total basis (Line 1 + Line 2) | $8,000 |

| Line 6 | Value of all traditional IRAs at year end | $0 (fully converted) |

| Line 14 | Remaining basis | $0 (all basis used in conversion) |

| Line 16 | Amount converted to Roth | $8,002.19 |

| Line 17 | Taxable amount of conversion | $2.19 |

Source: Illustrative Form 8606 walkthrough for a clean backdoor Roth with no pre-existing IRA balances. Consult current-year Form 8606 instructions.

Jennifer’s total federal tax on the backdoor Roth: $2.19 × 22% = $0.48.

Backdoor Roth IRA Step-by-Step Summary

| Step | Action | Timing | Key Requirement |

|---|---|---|---|

| 1 | Open traditional IRA | Any time before April 15, 2027 | No pre-existing pre-tax IRA balance |

| 2 | Contribute $8,000 non-deductible | Jan 1, 2026 – Apr 15, 2027 | Earned income; do NOT invest yet |

| 3 | Wait for funds to settle | 1–3 business days | Do not convert until settled |

| 4 | Convert entire balance to Roth IRA | Immediately after settlement | Select “no withholding” |

| 5 | Invest the Roth IRA funds | Same day as conversion | Do not leave in money market |

| 6 | File Form 8606 with tax return | By April 15, 2027 | Required every year — no exceptions |

Source: IRS Publication 590-A, IRS Form 8606 instructions, 2026.

The Annual Rhythm – Repeating the Strategy Year After Year

The backdoor Roth IRA is not a one-time event. It is an annual discipline — and it gets simpler every year after the first.

How the Second Year Differs From the First

In year one, you opened two accounts and navigated the process for the first time. In year two and beyond:

- The traditional IRA already exists

- The Roth IRA already exists

- The process is four actions: contribute → settle → convert → invest

- File Form 8606 with your annual tax return

Total annual time commitment after year one: approximately 30 minutes.

The Recommended Annual Sequence

January (recommended): Fund the traditional IRA for the new tax year as early as possible.

January (2–3 days later): Convert to Roth IRA immediately after funds settle.

January (same day as conversion): Invest the Roth IRA funds.

April (following year): File Form 8606 with your annual tax return.

The Lifetime Wealth Impact

Backdoor Roth IRA Wealth Accumulation Over Time ($8,000/year contribution, 7% annual return):

| Years of Execution | Total Contributions | Roth IRA Balance (7% return) | Tax-Free Growth |

|---|---|---|---|

| 5 years | $40,000 | $46,004 | $6,004 |

| 10 years | $80,000 | $110,491 | $30,491 |

| 15 years | $120,000 | $201,384 | $81,384 |

| 20 years | $160,000 | $328,988 | $168,988 |

| 25 years | $200,000 | $506,765 | $306,765 |

Source: Compound growth calculations at 7% annual return on $8,000/year contributions. For illustrative purposes only.

The Married Couple Multiplier

Both spouses can independently execute backdoor Roth IRAs, doubling the annual contribution to $16,000/year. At 7% return over 15 years, a married couple accumulates approximately $402,000 in combined Roth IRA wealth — with zero taxes owed on distributions in retirement. Neither spouse’s income affects the other’s backdoor Roth eligibility, provided each has independent earned income.

The Roth 401(k) Combination

The backdoor Roth IRA pairs powerfully with a Roth 401(k). In 2026, married high earners can simultaneously contribute:

- Roth 401(k): up to $31,000 each (age 50+) — no income limits

- Backdoor Roth IRA: $8,000 each — no income limits via the backdoor method

- Combined annual Roth savings per couple: up to $78,000/year in tax-free growth accounts

This combination is the most powerful tax-free retirement savings strategy available to high earners today. If you are not yet clear on how your retirement number fits into a picture like this, our guide on how to set your retirement number walks through exactly how to map your savings to a specific goal.

Pro Tip: Set a recurring annual calendar reminder for January 2nd of every year: “Fund backdoor Roth IRA.” A contribution on January 2nd versus April 14th earns an additional 3.5 months of tax-free Roth growth — approximately $163 per year in additional compounding at 7%. Small gap per year, significant gap over a decade.

The Pro-Rata Rule – The Most Dangerous Element of the Backdoor Roth

The pro-rata rule is the single most important concept in backdoor Roth IRA planning — and the most commonly misunderstood. This section requires your complete attention. Many backdoor Roth guides mention it in a paragraph. What follows is the full mathematical treatment, because this is where real financial mistakes happen.

What Is the Pro-Rata Rule?

When calculating the taxable portion of a Roth IRA conversion, the IRS treats all of a taxpayer’s traditional IRA accounts as one combined pool — regardless of which specific account or which specific dollars were converted.

The taxable percentage of any conversion is determined by this formula:

Taxable Percentage = Pre-tax IRA Balance ÷ (Total IRA Balance Including After-Tax Contributions)

Taxable Amount = Converted Amount × Taxable Percentage

The Impact in Hard Numbers

Here is what this means in practice. Suppose Jennifer had a pre-existing rollover IRA containing $192,000 in pre-tax funds from a former employer’s 401(k). She contributes $8,000 in non-deductible after-tax funds to a new traditional IRA and immediately converts the $8,000 to Roth.

Without understanding the pro-rata rule, Jennifer expects to pay tax only on $2.19 in earnings. In reality:

- Total IRA balance: $192,000 (pre-tax rollover) + $8,000 (after-tax contribution) = $200,000

- After-tax ratio: $8,000 ÷ $200,000 = 4%

- Pre-tax ratio: 96%

- Of Jennifer’s $8,000 conversion: 96% is taxable = $7,680 treated as taxable ordinary income

- At Jennifer’s 24% bracket: $7,680 × 24% = $1,843 in unexpected federal income tax

Instead of paying $0.48 in tax — as in the clean scenario — Jennifer pays $1,843. A difference of $1,842.52 caused entirely by a misunderstood rule and a forgotten rollover IRA.

Why the Pro-Rata Rule Applies to ALL IRA Accounts

The IRS aggregates all traditional, SEP, and SIMPLE IRA accounts for pro-rata purposes. They are treated as a single IRA regardless of how many institutions hold them, how many separate accounts you have, or which specific account you converted from.

What is NOT included in the aggregation:

- Roth IRA accounts

- 401(k), 403(b), and 457(b) accounts

That last point — employer plan accounts are excluded — is the key to the most important solution.

The Four Solutions to the Pro-Rata Problem

Solution 1 — Have no pre-tax IRA balances (ideal)

If you have never made deductible IRA contributions and have no rollover IRA balances, the pro-rata rule has zero impact on your backdoor Roth. Jennifer’s clean situation is exactly this: her $8,000 conversion generates essentially zero taxable income.

Solution 2 — Roll pre-tax IRA balances into your 401(k)

Most 401(k) and 403(b) plans accept incoming rollovers from traditional IRAs. Rolling your pre-tax IRA balance into your employer’s 401(k) removes those funds from the pro-rata calculation — because 401(k) assets are not included in the IRS aggregation rule.

After the rollover, your traditional IRA balance is zero (or reduced to only your new non-deductible contribution). The pro-rata rule no longer affects your backdoor Roth.

Jennifer’s Solution 2 example:

If Jennifer had a $192,000 rollover IRA, she would first confirm that her employer’s 401(k) accepts incoming rollovers. It does. Jennifer rolls the $192,000 into her employer’s 401(k) plan. Her traditional IRA balance is now zero. She then executes the backdoor Roth with a clean $8,000 non-deductible contribution — paying tax only on $2.19 in earnings, exactly as in the simple scenario.

Solution 3 — Convert the entire traditional IRA in a low-income year

If rolling to a 401(k) is not an option, converting the entire traditional IRA balance (including all pre-tax funds) resolves the pro-rata problem — but creates a large taxable event. For most high earners in the 24–37% bracket, a forced large conversion is not tax-efficient. This approach works best in a year of unusually low income, such as a career transition or early retirement year.

Solution 4 — Systematic partial conversions to drain the pre-tax balance over time

Convert a controlled portion of pre-tax IRA funds each year — targeting amounts that stay within your current tax bracket — while simultaneously making new non-deductible contributions. Over five to ten years, the pre-tax balance is systematically eliminated, eventually enabling clean backdoor Roth contributions.

Common Mistake Warning: Failing to check all IRA balances before executing a backdoor Roth is the single most expensive error in this process. Many people have rollover IRAs from former employers they have forgotten about — or IRAs containing deductible contributions from earlier, lower-income years. Before your first backdoor Roth contribution, pull your complete IRA balance across every financial institution and run the pro-rata calculation. A surprise $150,000 rollover IRA can transform a zero-tax backdoor Roth into a $36,000 tax bill.

Form 8606 Deep Dive – Filing It Correctly Every Year

Form 8606 is not a detail. It is the foundation of the entire backdoor Roth strategy. Without it filed correctly, the tax advantages of the strategy can unravel — potentially years or decades after the contributions were made.

What Form 8606 Does

Form 8606 performs three functions:

- Establishes and tracks your cumulative after-tax (non-deductible) IRA basis with the IRS

- Reports the taxable portion of any Roth IRA conversions

- Creates the official record that proves your converted funds were already taxed — preventing double taxation when you take distributions in retirement

The Cumulative Basis Concept

Each year you make a non-deductible traditional IRA contribution, your basis increases. The basis persists year to year — it does not reset annually. Form 8606 carries the running total forward from year to year, creating a documented record across your entire contributing lifetime.

If Jennifer executes the backdoor Roth for five consecutive years at $8,000 per year, her cumulative Form 8606 basis reaches $40,000. This record is what the IRS uses to determine — years or decades from now — that those distributions are not taxable again.

What Happens If You Miss a Year

Failing to file Form 8606 in a year when you made a non-deductible contribution does not eliminate your basis — but it requires you to file an amended return (Form 1040-X) to establish that year’s contribution. The IRS charges a $50 penalty for failure to file Form 8606 when required.

More critically: without the filed Form 8606, future distribution tax calculations have no documented basis to reference. The IRS default is to treat undocumented IRA distributions as fully taxable. You may end up proving a basis you cannot prove.

If you have missed prior years, file amended Form 1040-X returns for each year — including the relevant Form 8606 with each. The IRS generally allows amended returns up to three years past the original filing deadline. Older situations may require professional guidance.

The Critical End-of-Year IRA Balance (Line 6)

The IRS calculates the pro-rata ratio using your December 31st traditional IRA balance — not the balance at the time of conversion.

This timing detail matters: if you convert the entire traditional IRA to Roth before December 31st, your year-end IRA balance is zero, and the pro-rata ratio is 0%. The full basis is available for the clean, tax-free conversion. If you contribute in late December but do not convert until January of the following year, your December 31st traditional IRA balance includes the new contribution — complicating the Form 8606 calculation. Contribute and convert within the same calendar year whenever possible.

Form 8606 Line-by-Line (Clean Backdoor Roth, No Pre-existing Balances)

| Form 8606 Line | Description | Jennifer’s Amount |

|---|---|---|

| Line 1 | Non-deductible contributions this year | $8,000 |

| Line 2 | Prior year cumulative basis (first year: $0) | $0 |

| Line 3 | Total basis (Line 1 + Line 2) | $8,000 |

| Line 6 | Value of all traditional IRAs at year end | $0 (fully converted) |

| Line 14 | Remaining basis | $0 (all basis used in conversion) |

| Line 16 | Amount converted to Roth | $8,002.19 |

| Line 17 | Taxable amount of conversion | $2.19 |

Source: Illustrative walkthrough for a clean backdoor Roth with no pre-existing IRA balances. Consult current-year Form 8606 instructions.

Pro Tip: Keep a dedicated folder — physical or digital — for every Form 8606 you ever file. Your cumulative after-tax IRA basis is a number you will need potentially decades from now, when taking retirement distributions or when heirs handle inherited IRA accounts. A complete historical record of every Form 8606 filed since your first non-deductible contribution protects you from double taxation at a time when recreating the record may be impossible.

Common Backdoor Roth Mistakes – The Eight Errors That Trigger Tax Bills

Preventable execution errors are the primary risk in backdoor Roth IRA planning. Every one of these mistakes has a specific, quantifiable cost. Avoid all eight.

Mistake 1 — Forgetting to check existing IRA balances before contributing

The pro-rata rule applies to ALL traditional, SEP, and SIMPLE IRA balances. A forgotten rollover IRA from a prior employer can transform a planned zero-tax conversion into a significant taxable event. Always run the pro-rata calculation before Step 2.

Mistake 2 — Investing the traditional IRA before converting

Investing in the traditional IRA creates earnings that become taxable upon conversion. One month in an S&P 500 index fund at 7% annual return on $8,000 generates approximately $47 in taxable income. For a high earner in the 35% bracket, that is an unnecessary $16 tax bill. Keep the traditional IRA in the money market settlement fund and convert immediately after settlement.

Mistake 3 — Electing tax withholding on the conversion

Selecting withholding during the Roth conversion reduces the amount that actually lands in the Roth IRA — and that withheld portion is treated as a distribution, potentially subject to early withdrawal penalties if you are under 59½. Always select “no withholding” and pay any minimal conversion taxes from external funds at tax time.

Mistake 4 — Using the 60-day indirect rollover method

Taking a distribution from the traditional IRA and depositing it into the Roth IRA within 60 days triggers mandatory 20% withholding — meaning you receive only $6,400 of your $8,000. To complete the conversion cleanly, you must deposit the full $8,000 into the Roth within 60 days, covering the withheld $1,600 from outside funds. The direct conversion method eliminates this risk entirely.

Mistake 5 — Contributing more than the earned income limit

IRA contributions cannot exceed your earned income for the year. If you earn only $6,000 through part-time consulting, you cannot contribute more than $6,000 — even though the limit is $8,000. Excess IRA contributions carry a 6% annual excise tax for every year the excess remains in the account.

Mistake 6 — Failing to file Form 8606

Without Form 8606, the IRS has no record of your non-deductible contribution. When you eventually take distributions from any IRA account in retirement, the IRS may treat those distributions as fully taxable — double-taxing money you have already paid income tax on. File Form 8606 every year without exception.

Mistake 7 — Contributing and converting in different tax years without understanding the timing implications

Contributing in December 2026 (for the 2026 tax year) and converting in January 2027 creates a December 31st IRA balance that complicates the pro-rata calculation — the traditional IRA shows the contribution on December 31st, but the conversion does not happen until the following year. Either contribute and convert within the same calendar year, or understand the specific Form 8606 implications of a year-straddling approach with a CPA before proceeding.

Mistake 8 — Assuming the strategy is fully automatic after setup

No brokerage automatically contributes and converts on your behalf each year. Forgetting to execute in a given year means missing $8,000 in Roth IRA space permanently — prior years’ contribution room cannot be made up retroactively. Set an annual calendar reminder and treat it like a bill.

Many of the broader financial planning errors that trip up high earners — including several that create the IRA balance situations described above — are covered in our 10 retirement myths debunked piece. Myth #3 and Myth #6 in particular apply directly to backdoor Roth planning.

The Mega Backdoor Roth – Supercharging the Strategy for High Savers

The backdoor Roth IRA moves $8,000 per year into tax-free growth. For high earners who want to move dramatically more, the Mega Backdoor Roth uses a different vehicle — the 401(k) — to achieve the same goal at a much larger scale.

What Is the Mega Backdoor Roth?

The Mega Backdoor Roth is a strategy that uses after-tax contributions to a 401(k) plan — contributions beyond the standard pre-tax or Roth employee limit — to fund a much larger Roth account.

The total 401(k) plan limit in 2026 is $70,000 (or $77,500 for age 50+), which includes employee contributions, employer match, and after-tax contributions. If an employer allows after-tax 401(k) contributions and in-plan Roth conversions (or in-service withdrawals to a Roth IRA), the Mega Backdoor Roth can funnel an additional $30,000 to $40,000+ per year into tax-free growth.

The Math

Jennifer maxes her pre-tax 401(k) at $23,500 (standard employee limit). Her employer contributes an $8,000 match. That leaves $70,000 − $23,500 − $8,000 = $38,500 in potential after-tax 401(k) contribution space. Her plan allows after-tax contributions and in-plan Roth conversions. Jennifer contributes an additional $38,500 in after-tax funds, then immediately converts them to a Roth 401(k) account within the plan.

Combined with her regular backdoor Roth IRA ($8,000), Jennifer’s total annual Roth savings: $38,500 + $8,000 = $46,500 in tax-free growth accounts — in addition to her $23,500 pre-tax 401(k) contribution.

Plan Availability Is the Limiting Factor

Not all 401(k) plans allow after-tax contributions. Not all plans that allow after-tax contributions also allow in-plan Roth conversions or in-service withdrawals. Check your employer’s Summary Plan Description to determine whether your plan supports this feature. The Mega Backdoor Roth is most commonly available in tech company plans and large corporate benefit programs.

Combined Annual Roth Savings Potential for High Earners (2026)

| Strategy | Annual Roth Contribution | Available To |

|---|---|---|

| Direct Roth IRA | $8,000 (age 50+) | Income below $165K single / $246K married |

| Backdoor Roth IRA | $8,000 (age 50+) | All earners via non-deductible IRA + conversion |

| Roth 401(k) | $31,000 (age 50+ incl. catch-up) | All earners — no income limits |

| Mega Backdoor Roth | Up to $38,500+ (plan-dependent) | All earners if plan allows after-tax contributions |

| Maximum combined (age 50+) | Up to $77,500/year | High earners with access to all strategies |

Source: IRS 401(k) plan limits, 2026. After-tax contribution space depends on employer match and plan provisions.

Frequently Asked Questions

Q: Is the backdoor Roth IRA legal? Will it get me audited?

Yes, the backdoor Roth IRA is entirely legal. The strategy was explicitly acknowledged by the Joint Committee on Taxation in 2010 when Congress removed the income limit on Roth conversions. The IRS has issued specific guidance on how to execute and report it correctly via Form 8606. When properly reported, it is a standard tax filing item — not an audit trigger. What attracts scrutiny is improper reporting: failing to file Form 8606, or misreporting the taxable amount of the conversion. Executed correctly and reported accurately, the backdoor Roth is as mainstream as any other retirement contribution.

Q: What happens if I contribute to a traditional IRA for the backdoor Roth but my income drops below the Roth limit that same year?

If your income drops below the direct Roth IRA contribution limit before you execute the conversion, you have two options. You can recharacterize the traditional IRA contribution as a direct Roth IRA contribution by the tax filing deadline (October 15th with extensions). Or you can proceed with the backdoor conversion as planned — the process and outcome are identical regardless of whether you technically qualified for a direct contribution.

Q: Can I do a backdoor Roth IRA if I’m self-employed and have a SEP IRA?

Yes — but the SEP IRA balance is included in the pro-rata calculation, which is the central complication for self-employed individuals. If you have a large SEP IRA balance, the pro-rata rule will make most of your conversion taxable. The solution is to establish a Solo 401(k) and roll the SEP IRA balance into it. Most Solo 401(k) plans accept SEP IRA rollovers, which removes the SEP IRA funds from the pro-rata calculation entirely. With a zero SEP IRA balance, the backdoor Roth proceeds cleanly. This is a well-established strategy for high-earning self-employed individuals — but requires careful sequencing.

Q: My spouse has no earned income. Can we still do a backdoor Roth IRA for them?

Yes, through the spousal IRA provision. A non-working (or low-earning) spouse can contribute to an IRA based on the working spouse’s earned income, as long as you file a joint tax return. The contribution limit is $8,000 per year (age 50+) — the same as for the working spouse. A married couple can therefore execute two backdoor Roth IRAs — $16,000 per year total — even if only one spouse has earned income. The spousal backdoor Roth requires the same steps: non-deductible traditional IRA contribution in the non-working spouse’s name, conversion to the non-working spouse’s Roth IRA, and Form 8606 in the non-working spouse’s name.

Q: I already have a large pre-tax rollover IRA. Is the backdoor Roth still worth doing?

It depends on whether you can roll the pre-tax IRA into your employer’s 401(k) first. With a large pre-tax IRA balance and no rollover option, the pro-rata rule makes most of each conversion taxable — potentially making the strategy inefficient. But if your current employer’s 401(k) accepts incoming IRA rollovers (most do), rolling the pre-tax IRA into the 401(k) before executing the backdoor Roth can transform a complicated, heavily taxable conversion into a clean, essentially zero-tax contribution. Check your Summary Plan Description first.

The Bottom Line

The income limits that block direct Roth IRA contributions do not block the backdoor Roth. High earners who skip this strategy are permanently leaving $8,000 per year in tax-free retirement growth on the table — space that cannot be recovered retroactively.

Three things to take from this guide:

1. Execution precision matters more than in almost any other retirement strategy. Six specific steps, Form 8606 filed every year without exception. Done correctly: $0.48 in taxes on Jennifer’s $8,000 contribution. Done incorrectly: a $1,000+ unexpected tax bill.

2. The pro-rata rule is the landmine. Check your IRA balances across every financial institution before contributing. If pre-tax balances exist, roll them into your 401(k) first — then execute the backdoor Roth from a clean slate.

3. Consistency is everything. $8,000 per year executed precisely for 15 years becomes $201,000 in tax-free retirement wealth. One missed year cannot be made up. One improperly executed year can trigger a significant and entirely preventable tax bill.

The IRS created the income limits. Congress opened the door around them. Form 8606 is the key. Use it — every year, without fail.

Ready to build the complete tax-free retirement picture? Check our retirement readiness quiz to see how your tax readiness stacks up across every category — the backdoor Roth is one piece of a larger strategy. And if you are thinking about what to do with IRA or 401(k) balances from a former employer — which directly affects the pro-rata rule — why retirement wealth planning starts now covers the cost of waiting and how to begin with clarity.

Disclaimer: The content on RetireWealthPath.com is for informational and educational purposes only and does not constitute financial, tax, or legal advice. We are not licensed financial advisors or CPAs. The backdoor Roth IRA strategy, pro-rata rule calculations, Form 8606 requirements, contribution limits, income phase-out thresholds, Mega Backdoor Roth provisions, and all other figures and rules referenced in this article reflect 2026 IRS guidelines and are subject to change by legislation or IRS policy. All calculations, named examples, Form 8606 walkthroughs, and strategic recommendations — including Jennifer and all other examples — are for illustrative and educational purposes only and do not represent guaranteed outcomes or tax advice. The backdoor Roth IRA involves complex tax interactions that depend on your specific financial situation, existing IRA balances, employer plan provisions, and filing status. Errors in execution or reporting can result in unexpected tax bills and penalties. Always consult a qualified CPA, tax advisor, or financial professional before executing a backdoor Roth IRA strategy.