How to Build Wealth After 50: Complete 2026 Strategy Guide

The conventional wisdom says wealth building is for the young — start at 25, retire at 65, and hope the math works out. But here is what the conventional wisdom misses: the average American’s peak earning years are their 50s. The decade when children leave home, mortgages shrink, and salaries reach their highest point is also the decade when most people feel most behind on retirement savings.

That disconnect — between the genuine financial opportunity of your 50s and the anxiety most people feel about them — is the gap this post exists to close.

If you are wondering how to build wealth after 50, you are already asking the right question. The 50s combine your highest income, your lowest family expenses, federally expanded catch-up contribution limits, and still 15+ years of investment compounding.

For many Americans, this is the first decade where truly aggressive wealth building becomes financially possible — not despite starting later, but because of where life has brought you.

Yes, starting at 50 is harder than starting at 30. The math is less forgiving. But it is not hopeless — not by a long way. Below are eight specific, impact-ranked strategies that turn this decade into your most powerful wealth-building window yet.

Let’s start with the single most powerful move available to anyone over 50 — and it has nothing to do with picking the right stocks.

First: Reframe the Timeline — Your 50s Are an Opportunity, Not a Crisis

The most powerful obstacle to wealth building after 50 is psychological — the belief that it is too late. Before any strategy makes sense, this belief needs to go. Here is what the data actually says.

The average retirement age in the United States is 62 for women and 64 for men. Most readers of this post have 10–15 earning years ahead of them. Life expectancy for a 50-year-old American is approximately 82 for men and 85 for women — meaning 30–35 years of retirement to fund, and therefore 30–35 years for investments, Roth accounts, and Social Security to compound.

A 50-year-old who contributes the maximum $31,000 per year to a 401(k) for 15 years at 7% average return accumulates approximately $800,000 in contributions and growth — from zero. Add a $8,000/year IRA contribution over the same period and the number climbs past $1 million. The math is not comfortable. But it is real.

On top of that: median weekly earnings for American workers peak in their 50s (Bureau of Labor Statistics data consistently shows this). Children are typically leaving or have already left home — eliminating $15,000–$25,000 per year in expenses for many families. Mortgages are typically 15–20 years in, with reduced balances and lower payoff timelines. The confluence of highest income + lowest family expenses is the greatest wealth-building surplus of most people’s working lives.

And compounding? The Rule of 72 says money invested at 7% doubles every 10 years. $100,000 invested at 50 becomes $200,000 at 60, $400,000 at 70, and $800,000 at 80. Even modest sums generate meaningful wealth over a 20–35 year horizon.

Patricia, 51, feels behind. She has $95,000 in a 401(k), $0 in an IRA, and $12,000 in a savings account. Her financial advisor runs the projections: if Patricia maximizes her 401(k) catch-up contributions ($31,000/year) and opens a backdoor Roth IRA ($8,000/year) for the next 14 years to retirement at 65 — at 7% average return — her portfolio reaches approximately $1,050,000. Combined with Social Security income of approximately $2,200/month, Patricia’s retirement is not just possible. It is genuinely comfortable. The anxiety she felt at 51 was real. But the math, properly understood, told a different story.

Pro Tip Run the actual numbers for your situation before drawing any conclusions about whether you are “too far behind.” Use the free compound interest calculator at investor.gov with your current savings, your maximum annual contribution capacity, and a 7% average return assumption. Many people are significantly more on track than they feel — and those who are genuinely behind find the calculation motivating, because it shows the exact gap and the exact actions needed to close it.

Before you dive into any of the eight strategies below, take the Retirement Readiness Quiz — it will ground you in where you actually stand before you decide which of these strategies to prioritize first.

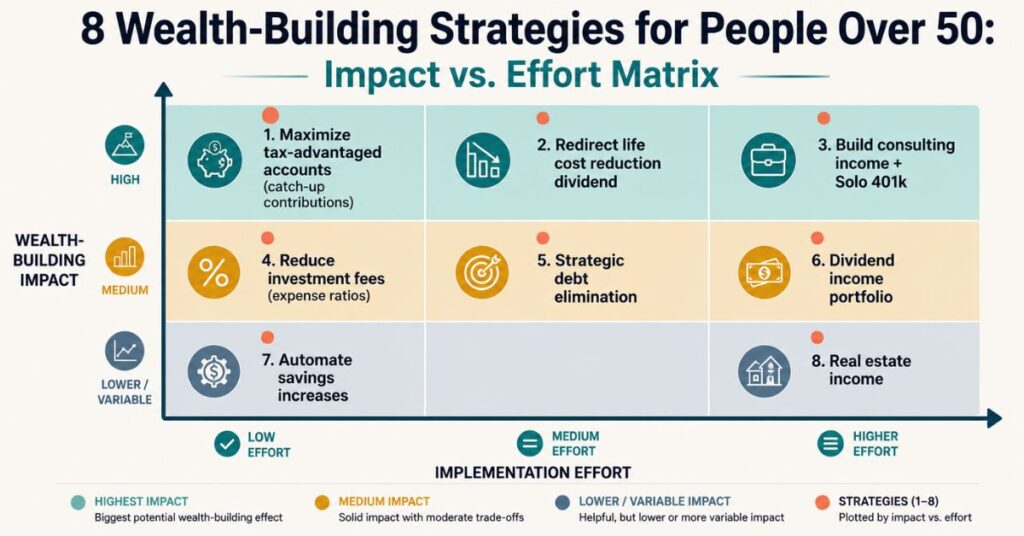

Strategy 1 — Maximize Every Tax-Advantaged Account Available to You

The single highest-ROI wealth-building action available to anyone over 50 is maximizing tax-advantaged accounts — particularly the catch-up provisions designed specifically for this decade.

People aged 50 and older can contribute significantly more to retirement accounts than younger workers. In 2026, the numbers look like this:

| Account Type | Under 50 Limit | Age 50–59 Limit | Age 60–63 Limit | Age 64+ Limit |

|---|---|---|---|---|

| 401(k) / 403(b) | $23,500 | $31,000 | $34,750 | $31,000 |

| Traditional / Roth IRA | $7,000 | $8,000 | $8,000 | $8,000 |

| HSA (individual) | $4,300 | $5,300 | $5,300 | $5,300 |

| HSA (family) | $8,550 | $9,550 | $9,550 | $9,550 |

| Total (401k + IRA, no HSA) | $30,500 | $39,000 | $42,750 | $39,000 |

Source: IRS contribution limits, 2026. HSA eligibility requires enrollment in a qualifying High-Deductible Health Plan. SECURE 2.0 super catch-up applies ages 60–63.

The wealth acceleration math is striking. Maximizing a 401(k) and IRA ($39,000/year) at 7% return for 15 years from age 50 to 65 produces approximately $1,005,000. Contributing only $10,000/year for the same period produces approximately $257,000. The gap between maximizing and under-contributing is $748,000 — from the same 15-year window.

Every dollar in a tax-advantaged account also grows without annual tax drag on dividends and capital gains. A taxable account earning 7% gross may net only 5.5–6% after annual taxes — a drag that compounds dramatically over 15 years.

Common Mistake Treating retirement account maximization as something to “work up to” gradually — planning to increase contributions “next year” or “when things settle down.” The catch-up contribution window is finite. A $20,000 under-contribution at age 52 at 7% growth represents approximately $55,000 in foregone wealth by age 65. Every year below the maximum permanently forfeits that compounding.

If you want a deeper walkthrough of exactly how to calculate the retirement savings target your contributions are working toward, read How to Set Your Retirement Number — it pairs directly with the maximization strategy above.

Strategy 2 — Attack Debt Strategically, Not Emotionally

Debt is the primary obstacle to aggressive wealth building in your 50s — but not all debt is equally urgent. Here is the rational framework for deciding what to eliminate and what to service.

A $25,000 credit card balance at 22% interest costs $5,500 per year in interest — money that could otherwise compound in a retirement account. Paying off that balance is the financial equivalent of earning a guaranteed, risk-free 22% return. No investment reliably beats that.

The priority sequence for wealth builders over 50:

Priority 1 — Credit cards and personal loans above 10%: Eliminate immediately and aggressively. No investment reliably returns 10%+ risk-free. Every dollar paying 22% is destroying wealth.

Priority 2 — Auto loans and consumer debt (6–10%): Pay down systematically while continuing to capture the full employer 401(k) match. At these rates, the mathematical case for investing vs. paying down is ambiguous — personal preference and psychological peace of mind are valid factors.

Priority 3 — Mortgage (typically 3–7%): The most complex debt decision for 50-year-olds. If your rate is below 5%, investing in diversified index funds (historical 7–10% average return) is mathematically superior. If your rate is above 6.5%, the math is essentially a coin flip — and the peace of mind from carrying no mortgage into retirement is a legitimate consideration.

Thomas, 53, carries $18,000 in credit card debt ($330/month minimum at 22% interest), a $520/month car payment (4.9% interest, 3 years remaining), and a mortgage at $1,650/month (15 years remaining, 4.5% rate). Thomas’s wealth-building priority: eliminate the credit card first, aggressively, in 12–18 months. Then redirect the freed $330/month to additional 401(k) contributions. Next: let the car loan run its course while redirecting that $520/month to investment upon payoff. The mortgage is strategically serviced — Thomas plans to downsize at 67, so equity will be converted through the home sale.

Priority Rule Always capture the full employer 401(k) match before paying extra on any debt. A 100% immediate match (free money) outcompetes even 22% credit card paydown — mathematically and practically. Sequence: (1) contribute enough for full match, (2) eliminate high-interest debt, (3) maximize all tax-advantaged accounts, (4) address remaining debt based on interest rate comparison.

Strategy 3 — Capture the “Life Cost Reduction Dividend”

One of the most powerful and underappreciated wealth-building forces in your 50s is not earning more — it is capturing the cash flow that becomes available as major life expenses naturally shrink. Call this the life cost reduction dividend.

Unlike a raise (which requires employer action) or an investment return (which is uncertain), the life cost reduction dividend is predictable, certain, and automatic — if you capture it deliberately rather than letting it dissolve into lifestyle upgrades.

The major reductions that typically occur in your 50s:

Children leaving home ($15,000–$30,000/year freed): Food, clothing, transportation, extracurricular activities, and discretionary spending for children adds up dramatically. When the last child leaves home, this cash flow becomes available for wealth building — if captured deliberately.

Reduced college financial support ($5,000–$25,000/year freed): For parents supporting college students, tuition, room, and board often peak in the early-to-mid 50s. When college support ends, the freed cash flow is a significant opportunity.

Mortgage approaching payoff ($800–$2,500/month freed in the late 50s): Redirecting a $1,800/month mortgage payment to investment at age 58, seven years before retirement at 65, generates approximately $204,000 in additional wealth at 7% return.

Sandra, 54, sends her youngest child to college this fall. Her child-related household expenses drop by approximately $18,000 per year. Sandra redirects $1,200/month of the freed cash to her 401(k) — bringing her annual contribution to $31,000 — and $300/month to a Roth IRA ($8,000/year via monthly contributions). The remaining $6,600/year goes toward accelerated mortgage paydown. Sandra’s wealth trajectory changes dramatically — not because she earned more, but because she captured cash flow that was always there.

The biggest threat to this dividend is lifestyle inflation — replacing child-rearing costs with an upgraded car, home renovation, or expanded dining budget. These naturally fill cash flow vacuums if the money is not pre-committed. The solution: automate the retirement contribution increase the same month child expenses decrease, before the money touches your checking account.

If you are unsure whether you are approaching retirement with a strong enough financial foundation to capture this dividend effectively, the Retirement Readiness Quiz is worth running first — it will show you which pillar of retirement readiness needs the most attention right now.

Strategy 4 — Build Multiple Income Streams Beyond Your Primary Career

Single-income dependence is a wealth vulnerability in your 50s. Age discrimination in employment is illegal but real — workers over 50 who lose their primary job face statistically longer unemployment periods and often accept lower salaries in new positions. A second income stream provides both additional wealth-building fuel and meaningful financial resilience.

The five most accessible income streams for 50-somethings:

Consulting and freelancing in your primary expertise: Your 50s represent peak professional knowledge and network depth. Consulting income of $20,000–$40,000 per year from 5–10 hours per week can be deposited into a Solo 401(k) — creating additional tax-advantaged savings beyond your employer’s plan. The combination of a W-2 job (maxing the employer 401(k) at $31,000) and self-employment consulting income (depositing into a Solo 401(k) as the employer contribution) can legally allow total annual retirement contributions well above $50,000.

Dividend-generating investment portfolio: Building a portfolio of dividend-paying index funds (VYM, SCHD) or REITs in a taxable brokerage account creates income that grows independent of employment. Even a $100,000 dividend portfolio at a 3.5% yield generates $3,500 per year — which, reinvested over 10 years, compounds significantly.

Real estate income: A single rental property generating $500–$800 per month net cash flow represents a meaningful supplement. REITs provide real estate income exposure without landlord responsibilities. For 50-somethings, purchasing a modest rental property with a 15-year mortgage aligns well with a retirement timeline — the mortgage pays off approximately at retirement age, and rental income becomes free cash flow.

Monetizing accumulated knowledge: Online courses, paid newsletters, or YouTube channels allow professionals to monetize decades of expertise. Even modest online income of $10,000–$20,000 per year, deposited into a Solo 401(k), adds meaningful tax-advantaged retirement savings.

Part-time work in a complementary field: Teaching, mentoring, or advisory roles at 10–15 hours per week generate income with minimal physical demand and often provide the social connection that makes the transition from full-time work feel less abrupt.

Richard, 56, works full-time as a marketing director earning $130,000 and maximizes his employer’s 401(k) at $31,000/year. He also does brand consulting 8 hours per week — earning approximately $35,000/year in net self-employment income. Richard opens a Solo 401(k) for his consulting business. As the “employer” in his Solo 401(k), Richard contributes 25% of his net self-employment income: 25% × $35,000 = $8,750 in additional employer contributions. Total annual retirement savings: $31,000 (employer 401k) + $8,750 (Solo 401k) + $8,000 (backdoor Roth IRA) = $47,750/year in tax-advantaged savings. His consulting side income nearly doubles his retirement contribution capacity.

Strategy 5 — Invest With the Right Allocation for Your Timeline

Investment allocation is where 50-somethings most commonly make wealth-destroying mistakes — in both directions. Too conservative leaves decades of growth on the table. Too aggressive creates catastrophic sequence-of-returns risk as retirement approaches.

Mistake A — Too conservative: A 52-year-old with a 33-year investment horizon who holds 100% bonds or stable value funds at 3–4% net return may not keep pace with inflation, let alone build real wealth. Healthcare inflation alone runs at 5–6% annually.

Mistake B — Too aggressive: Holding 100% equities at age 62 with a retirement date 2 years away exposes the portfolio to catastrophic sequence-of-returns risk. A 40% market decline at 63 with no cash buffer forces selling assets at their lowest prices to fund retirement expenses — a mathematically devastating scenario.

The evidence-based allocation framework for 50s wealth builders:

Early 50s (50–54) — Growth phase: 70–80% equities / 15–25% bonds / 5% cash. Ten to fifteen years to retirement is long enough for equity compounding to dominate.

Mid 50s (55–59) — Transition phase: 60–70% equities / 25–35% bonds / 5–10% cash. Sequence-of-returns risk begins to become relevant; start building the 1–2 year cash buffer that will protect against selling equities at depressed prices in early retirement.

Late 50s to early 60s (60–64) — Pre-retirement positioning: 50–60% equities / 30–40% bonds and income-generating assets / 5–10% cash covering 1–2 years of planned retirement expenses.

Carol, 58, has her entire $380,000 portfolio in a stable value fund at her 401(k) — earning 3.1% annually after switching out of equities during the 2022 correction and never returning. At 3.1% return with 7 years to retirement and 25 more years in retirement: $380,000 grows to $474,000 by age 65. At 6.5% (a conservative balanced portfolio): $380,000 grows to $590,000 — $116,000 more from the same starting balance. Carol shifts gradually to a 60% equity / 35% bond / 5% cash allocation, accepting short-term volatility in exchange for the substantially better long-term outcome her retirement security requires.

One common myth worth addressing here: that staying out of the stock market is the “safe” choice after 50. It is not. Inflation risk is as real as market risk — it just moves more slowly. If you find the retirement myths around investing confusing, the 10 Retirement Myths Debunked post clears up a number of these misconceptions in a way that directly informs how you should think about allocating in your 50s.

Strategy 6 — Reduce Investment Costs and Tax Drag Ruthlessly

For wealth builders in their 50s, two silent destroyers of accumulated wealth are investment fees and avoidable taxes. Both are fully controllable — and both create massive long-term impacts that most people never calculate.

For a $400,000 portfolio with 15 years to retirement at 7% gross return:

| Annual Expense Ratio | Net Return | Portfolio at Year 15 | Lost to Fees vs. Index |

|---|---|---|---|

| 0.05% (index fund) | 6.95% | $1,094,000 | — |

| 0.25% | 6.75% | $1,065,000 | $29,000 |

| 0.75% | 6.25% | $990,000 | $104,000 |

| 1.25% | 5.75% | $921,000 | $173,000 |

| 1.75% | 5.25% | $854,000 | $240,000 |

Source: Compound growth calculations, illustrative only. For educational purposes. Same portfolio, same gross return — different fees.

The audit is simple: log into every retirement account, find the expense ratio for every fund held, flag any above 0.20%, and research the low-cost index fund equivalent. Switching inside a 401(k) or IRA has no tax consequence.

Beyond fees, three tax strategies deserve attention:

Asset location optimization: Hold tax-inefficient assets (high-dividend stocks, REITs, bond funds) in tax-advantaged accounts. Hold tax-efficient assets (index funds with low dividend yields) in taxable brokerage accounts. This reduces annual taxable income from investments — functionally equivalent to a small ongoing return improvement.

Tax-loss harvesting: Selling investments at a loss generates capital losses that offset gains elsewhere in the portfolio. Losses carry forward indefinitely — losses generated in your 50s can offset gains taken in retirement.

The 0% capital gains rate: In 2026, long-term capital gains are taxed at 0% for single filers with taxable income below approximately $47,025 and married filers below approximately $94,050. Strategic planning can position some retirees to recognize capital gains at 0% in early retirement — before Required Minimum Distributions begin and push income higher.

Strategy 7 — Use Home Equity as a Wealth-Building Tool, Not a Piggy Bank

Home equity is the largest single asset for most Americans over 50 — and the most misused. The productive use of home equity is converting it into investable capital through a calculated, planned downsizing. The destructive use is extracting equity to fund current lifestyle.

A 58-year-old who owns a $650,000 home with a $180,000 remaining mortgage has approximately $470,000 in equity. Selling and purchasing a $350,000 home frees approximately $120,000 in net equity after transaction costs and the new purchase. That $120,000 invested at 7% for 7 years to retirement at 65 grows to approximately $193,000. Additionally: lower property taxes, lower maintenance costs, and potentially a reduced or eliminated mortgage payment frees ongoing monthly cash flow to redirect to retirement accounts.

One critical tax advantage deserves attention: homeowners who have lived in their primary residence for at least 2 of the past 5 years can exclude from capital gains taxes $250,000 of profit (single filers) or $500,000 of profit (married filing jointly). Many 50-somethings who purchased their home decades ago have appreciation that falls within this exclusion — meaning downsizing capital can be deployed into investments completely tax-free.

James, 59, owns a 4-bedroom home worth $720,000 with $160,000 remaining on the mortgage. His children are grown and the extra bedrooms unused. James and his wife sell, purchase a $420,000 townhome, and net approximately $130,000 after the new purchase, closing costs, and real estate fees. The profit on the original home is $280,000 — entirely within the $500,000 married filing jointly exclusion. Zero capital gains tax. James invests the $130,000 in a taxable brokerage account and eliminates his mortgage entirely on the new home. He redirects $1,450 per month previously going to the old mortgage entirely to his 401(k) catch-up contributions. James’s wealth trajectory improves dramatically from one real estate transaction.

Two pitfalls to avoid: cash-out refinancing for consumption (replacing tax-free equity with interest-bearing debt at 6.5%+), and treating home equity as guaranteed retirement funding. Real estate values fluctuate, home equity is illiquid, and retirement planning should not depend on a specific future sale price. Build retirement security from investment accounts first; treat home equity as a potential accelerator.

Strategy 8 — Build the Financial Habits That Make Everything Else Sustainable

All seven previous strategies require consistent execution over years. That requires habits — not just decisions made once and forgotten. Here is the behavioral infrastructure that makes wealth building after 50 automatic rather than heroic.

Habit 1 — The annual financial review (non-negotiable): Set a specific date each year — January 1st, your birthday, or the first Monday of November — as your permanent annual review date. Review total net worth, retirement account balances, investment allocation, expense ratios, beneficiary designations, Social Security estimated benefit, and progress toward your retirement number. The annual review creates accountability before small problems become expensive ones.

Habit 2 — Automatic contribution escalation: Set your 401(k) contributions to increase automatically by 1–2% of salary each year. Most major 401(k) platforms offer this feature. Set it once, let it compound. Even a 1% annual escalation on a $100,000 salary adds $1,000 per year in new contributions — and over 10–15 years, that compounds into significant additional retirement wealth.

Habit 3 — The 48-hour rule for major financial decisions: Any financial decision above a personal threshold (a useful default: $5,000) waits 48 hours before execution. This pause prevents emotionally-driven mistakes: panic selling during market corrections, impulse purchases, and hasty investment decisions. The most dangerous wealth-destroying behavior for people over 50 is panic selling during corrections. The average bear market lasts approximately 9–14 months before recovery begins — investors who sell during the decline and wait for “stability” lock in losses permanently.

Habit 4 — Net worth tracking: Track total net worth quarterly — total assets minus total liabilities. Net worth is the single most informative financial metric, capturing the progress of every strategy simultaneously. Free tools like Empower (formerly Personal Capital) make this straightforward.

Habit 5 — Pay yourself first, automatically: Every contribution — 401(k), IRA, taxable brokerage, emergency fund — should be automated before discretionary spending occurs. Wealth built from “what’s left after spending” rarely materializes consistently. Wealth built from automated first contributions — with spending adjusted to what remains — compounds reliably.

Eleanor, 53, creates her wealth-building habit infrastructure in February. She sets her 401(k) to auto-escalate 1% each January. She opens a Roth IRA at Fidelity with a $666/month automatic transfer ($8,000/year). She schedules her annual financial review for January 15th permanently in her calendar. She establishes a rule: any discretionary purchase above $3,000 waits 72 hours. Eleanor tracks net worth quarterly in a Google Sheet. None of these habits requires daily attention. Together, they ensure the seven strategies above execute automatically — whether she feels motivated in any given month or not.

Your 30-Day Wealth-Building Action Plan

Week 1 — Foundation (4 actions, about 2 hours)

- Calculate your current 401(k) contribution rate — are you at the maximum ($31,000 for age 50+)? If not, log into your 401(k) portal and increase it today.

- Pull your complete list of debts with interest rates — identify any above 7% to prioritize for paydown.

- List all monthly expenses reduced or eliminated in the past 3 years — calculate the monthly cash flow now available for wealth building.

- Create a free account at ssa.gov/myaccount and note your projected Social Security benefit at 62, Full Retirement Age, and 70.

Week 2 — Investment Audit (3 actions, about 1.5 hours)

- Log into every retirement account and list every fund with its expense ratio — flag any above 0.20% for replacement with a low-cost index alternative.

- Review your current investment allocation — compare to the age-appropriate ranges in Strategy 5 and identify any rebalancing needed.

- Research whether your employer’s 401(k) plan allows after-tax contributions (Mega Backdoor Roth potential) — read the Summary Plan Description or call HR.

Week 3 — Income and Accounts (3 actions, about 2 hours)

- Open a Roth IRA or backdoor Roth IRA at Fidelity, Vanguard, or Schwab if you do not have one — set up automatic monthly contributions of $666 ($8,000/year).

- Evaluate your consulting or freelance income potential — what expertise could generate $10,000–$30,000/year in 5–10 hours/week?

- Research Solo 401(k) options if you have or plan to develop self-employment income — contribution room can be dramatically expanded with even modest consulting income.

Week 4 — Systems and Habits (3 actions, about 1 hour)

- Schedule your annual financial review date permanently in your calendar — every year, going forward.

- Set your 401(k) to auto-escalate 1% annually starting January 2027.

- Establish net worth tracking: create a quarterly spreadsheet with total assets (retirement accounts, taxable accounts, home equity) and total liabilities (mortgage, loans).

Frequently Asked Questions

I’m 55 with only $120,000 saved. Is there a realistic path to a secure retirement?

Yes — though it requires deliberate, aggressive action in the next 10 years. At $120,000 with 10 years of maximum catch-up contributions ($31,000/year) at 7% average return, your portfolio reaches approximately $582,000. Add a projected $2,000/month Social Security benefit ($24,000/year) and you have a retirement income foundation of approximately $47,000 per year using the 4% rule. A modest but genuinely sustainable retirement. The path requires maximizing contributions immediately and consistently — every year below the maximum widens the gap.

Should I pay off my mortgage or invest in my 50s?

The mathematical answer depends on your mortgage interest rate relative to your expected investment return. If your rate is below 5%, investing in diversified equity index funds (historical 7–10% average return) is mathematically superior. If your rate is above 6.5–7%, the comparison is close enough that personal preference — peace of mind from being debt-free in retirement — becomes a valid factor. What should never be compromised regardless of the mortgage rate: capturing the full employer 401(k) match and maximizing catch-up IRA contributions. These generate guaranteed immediate returns that exceed any mortgage interest cost.

I inherited $200,000 at age 52. What is the single best use of it?

Resist the temptation to make any decision in the first 30 days. Emotion and major financial decisions do not mix well. Then: eliminate any high-interest debt first. If your 401(k) and IRA are not maxed for the current year, max them immediately. For the remaining balance, a diversified low-cost index fund portfolio in a taxable brokerage account — S&P 500 index fund, international index fund, bond index fund in age-appropriate proportions — is hard to beat. Consult a fee-only financial advisor for a one-time review before deploying more than $100,000 in a single move.

The stock market terrifies me. Can I build meaningful wealth after 50 without equity exposure?

Technically yes — but the path is significantly harder and the likely outcome is significantly less secure. Without equity exposure, your wealth-building tools are: aggressive cash savings (4–5% APY in 2026), Treasury bonds and CDs (4–5%), real estate income, and Social Security optimization. These can generate retirement security — but require higher savings rates and more active management than a diversified index fund approach. If market volatility is genuinely distressing, consider working with a fee-only financial advisor to build an allocation that provides meaningful equity exposure (perhaps 30–40% equities) without the psychological cost of a fully equity-weighted portfolio. The behavioral risk of panic selling during corrections often matters more than the theoretical optimal allocation.

How does Social Security factor into my wealth-building plan after 50?

Social Security is one of the most powerful retirement income tools available — and it interacts directly with how much you need to save. Every $1,000 per month in guaranteed Social Security income reduces your required portfolio by approximately $300,000 using the 4% rule. Delaying your Social Security claim past your Full Retirement Age (67 for most people) adds 8% to your monthly benefit permanently — and waiting from 67 to 70 adds 24%. Understanding exactly how your benefit is calculated and when to claim it can be worth more than years of additional contributions. The full guide to how Social Security is calculated walks through the formula in detail, and the best age to claim Social Security post covers the claiming decision from every angle.

The Bottom Line

50 is not the finish line for wealth building. For many Americans, it is the most financially powerful decade of their lives — if they use it deliberately.

Three things worth carrying with you from this post:

1. The catch-up contribution provisions for people over 50 are the government’s most generous wealth-building gift. $31,000–$34,750 per year in a 401(k) alone, used fully for 15 years, generates over $1,000,000 at historical return rates. This window is open right now.

2. The life cost reduction dividend — freed cash flow from children leaving home, debts paying off, and mortgages shrinking — is a predictable, certain wealth-building accelerator. Most 50-somethings will see it. The question is whether they capture it deliberately or absorb it into lifestyle spending before it reaches a retirement account.

3. Investment costs and behavioral mistakes are the two greatest threats to wealth building after 50. More destructive, for most people with established portfolios, than insufficient contributions. Low-cost index funds and the 48-hour rule protect against both.

Now that you have the full strategic playbook, your next step is understanding exactly where you stand and where you are trying to go. Start by reading How to Set Your Retirement Number to calculate the exact target these eight strategies are aimed at. Then revisit Why Retire Wealth Planning Starts Now for the mindset and structural foundation that keeps the plan moving when motivation fluctuates.

The people who build real wealth after 50 are not the ones who started earlier — they are the ones who started deliberately. You just did.

Disclaimer: The content on RetireWealthPath.com is for informational and educational purposes only and does not constitute financial, tax, or legal advice. We are not licensed financial advisors. Investment return projections, contribution limit figures, tax thresholds, and all other numerical references in this article reflect 2026 guidelines and are subject to change. All named examples — including Patricia, Thomas, Sandra, Richard, Carol, James, and Eleanor — are fictional and for illustrative purposes only. Historical investment returns are not indicative of future performance. All investment involves risk, including the potential loss of principal. Real estate investments involve additional risks including illiquidity, market fluctuations, and property management challenges. Always consult a qualified financial professional, CPA, or investment advisor before making wealth-building, investment, or tax decisions. Individual results will vary significantly based on income, savings rate, investment choices, market performance, and other factors.