Retirement Savings Guide [Save, Invest & Retire Comfortably]

Retirement may seem years away, but the earlier you begin saving, the easier it becomes to build long-term wealth. Whether you’re in your 20s, 40s, or approaching retirement, having a structured retirement savings plan can help you maintain financial independence and reduce stress later in life.

This guide explains everything you need to know about retirement savings, including how much to save, where to invest, tax advantages, common mistakes, and practical strategies to maximize your retirement income.

What Is Retirement Savings?

Retirement savings refers to the money you set aside during your working years to cover living expenses after you stop working.

These savings typically come from:

- Employer-sponsored retirement plans

- Individual Retirement Accounts (IRAs)

- Personal investment accounts

- Savings accounts

- Pension plans

- Social Security benefits

The goal is to replace your employment income and maintain your desired lifestyle throughout retirement.

Why Retirement Savings Matters

Without sufficient savings, retirees often rely solely on Social Security, which typically replaces only a portion of pre-retirement income.

A solid retirement savings plan helps you:

- Maintain your standard of living

- Cover healthcare expenses

- Protect against inflation

- Handle emergencies

- Leave an inheritance if desired

- Enjoy financial freedom

Starting early gives compound interest decades to grow your investments.

How Much Should You Save for Retirement?

There isn’t a universal number because everyone’s retirement goals differ.

Factors include:

- Current age

- Planned retirement age

- Expected lifestyle

- Healthcare costs

- Life expectancy

- Inflation

- Investment returns

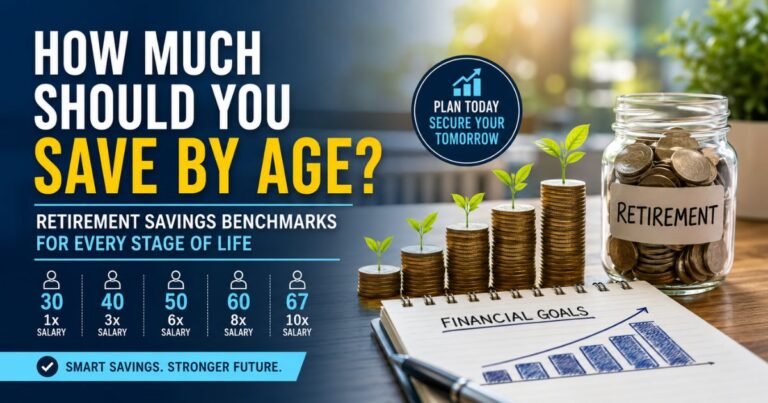

General Retirement Savings Benchmarks

| Age | Suggested Savings |

|---|---|

| 30 | 1× annual salary |

| 35 | 2× annual salary |

| 40 | 3× annual salary |

| 45 | 4× annual salary |

| 50 | 6× annual salary |

| 60 | 8–10× annual salary |

| 67 | 10–12× annual salary |

These are general guidelines rather than strict rules.

How Much Income Will You Need in Retirement?

Many financial planners suggest replacing 70% to 90% of your pre-retirement income.

For example:

Annual income before retirement: $80,000

Estimated retirement income needed:

- 70% = $56,000/year

- 80% = $64,000/year

- 90% = $72,000/year

Your target depends on housing costs, healthcare, travel plans, taxes, and other expenses.

Best Retirement Savings Accounts

1. 401(k)

A 401(k) is an employer-sponsored retirement plan.

Benefits include:

- Automatic payroll deductions

- Employer matching contributions (if offered)

- Tax advantages

- High annual contribution limits

Employer matching is essentially free money and should generally be prioritized.

2. Traditional IRA

A Traditional IRA allows you to contribute pre-tax money (subject to IRS rules).

Advantages:

- Potential tax deduction

- Tax-deferred investment growth

- Wide investment choices

Taxes are paid when funds are withdrawn during retirement.

3. Roth IRA

A Roth IRA is funded with after-tax dollars.

Benefits:

- Qualified withdrawals are tax-free

- No required minimum distributions during the owner’s lifetime

- Ideal for many younger investors expecting higher future tax rates

4. Health Savings Account (HSA)

If eligible, an HSA offers unique tax advantages.

Many experts consider it one of the most tax-efficient retirement tools because it offers:

- Tax-deductible contributions

- Tax-free growth

- Tax-free withdrawals for qualified medical expenses

5. Taxable Brokerage Account

After maximizing tax-advantaged accounts, many investors continue saving through taxable investment accounts.

Benefits include:

- No contribution limits

- Flexible withdrawals

- Broad investment options

How Much Should You Save Each Month?

A common recommendation is to save:

- 10% of income (minimum)

- 15% of income (ideal for many workers)

- 20% or more if starting later

Example:

| Annual Salary | Monthly Retirement Savings (15%) |

|---|---|

| $50,000 | $625 |

| $75,000 | $938 |

| $100,000 | $1,250 |

| $150,000 | $1,875 |

Consistency is generally more important than trying to time the market.

The Power of Compound Growth

Compound interest allows your investment earnings to generate additional earnings over time.

Example

Invest:

- $500 per month

- 30 years

- 8% average annual return

Estimated value:

Over $740,000

Starting even five or ten years earlier can significantly increase your retirement balance.

Retirement Savings by Age

In Your 20s

Focus on:

- Starting early

- Building saving habits

- Taking advantage of employer matching

- Investing aggressively for long-term growth

In Your 30s

Priorities include:

- Increasing contributions

- Paying down high-interest debt

- Diversifying investments

- Growing emergency savings

In Your 40s

This is often a high-earning period.

Consider:

- Maximizing retirement contributions

- Reviewing investment allocations

- Planning for college expenses without sacrificing retirement

- Estimating retirement income needs

In Your 50s

Focus on:

- Catch-up contributions (if eligible)

- Reducing unnecessary debt

- Preparing for healthcare costs

- Reviewing retirement timelines

In Your 60s

Important steps include:

- Creating a withdrawal strategy

- Delaying Social Security if beneficial

- Managing taxes

- Adjusting investment risk appropriately

Where Should Retirement Savings Be Invested?

Common investment options include:

- Stock index funds

- Bond funds

- Target-date retirement funds

- ETFs

- Dividend-paying stocks

- International funds

- REITs (in appropriate allocations)

Asset allocation should generally become more conservative as retirement approaches, though the right mix depends on individual circumstances.

Common Retirement Savings Mistakes

Avoid these frequent errors:

- Starting too late

- Not contributing enough

- Ignoring employer matching

- Cashing out retirement accounts early

- Paying high investment fees

- Keeping too much cash for decades

- Not reviewing investments regularly

- Underestimating inflation

- Forgetting healthcare costs

Tips to Increase Retirement Savings

Consider these practical strategies:

- Increase contributions after every raise.

- Automate monthly investments.

- Maximize employer matching.

- Reduce unnecessary spending.

- Eliminate high-interest debt.

- Invest consistently regardless of market fluctuations.

- Rebalance your portfolio periodically.

- Increase savings gradually each year.

Small improvements made consistently can produce significant long-term results.

Retirement Savings and Inflation

Inflation reduces purchasing power over time.

For example:

- $50,000 today may require significantly more in 30 years to maintain the same lifestyle.

Investments with long-term growth potential can help offset inflation more effectively than keeping all retirement savings in cash.

Retirement Withdrawal Strategy

Once retired, you’ll need a sustainable withdrawal plan.

Common considerations include:

- Withdrawal rate

- Required Minimum Distributions (RMDs)

- Tax-efficient withdrawals

- Social Security timing

- Healthcare costs

- Investment allocation

A balanced strategy can help extend the life of your retirement portfolio.

FAQs About Retirement Savings Guide

When should I start saving for retirement?

As early as possible. Starting in your 20s provides more time for compound growth, but it’s never too late to begin.

Is 15% of my salary enough?

For many people, saving around 15% of income throughout their career is a solid target. Individual needs may vary based on retirement goals, pensions, and other income sources.

Should I pay off debt or save for retirement?

High-interest debt should generally be prioritized, but if your employer offers a 401(k) match, contributing enough to receive the full match is often worthwhile.

Can I retire with only Social Security?

For most people, Social Security alone may not provide enough income to maintain their desired lifestyle, making personal retirement savings an important complement.

How often should I review my retirement plan?

Review your retirement strategy at least once a year or after major life events such as marriage, job changes, or nearing retirement.

Final Thoughts

Retirement planning isn’t about predicting the future perfectly, it’s about consistently making smart financial decisions over time. By saving regularly, investing wisely, taking advantage of tax-advantaged accounts, and reviewing your progress annually, you can build a retirement fund that supports your long-term goals.

The best retirement plan is one you start today. Even modest, consistent contributions can grow into substantial savings through the power of compounding, helping you enjoy greater financial security and flexibility throughout retirement.

Disclaimer: The information provided in this article is for educational and informational purposes only and should not be considered financial, investment, tax, legal, or retirement planning advice. Every individual’s financial situation and retirement goals are unique.

While we strive to keep our content accurate and up to date, we make no guarantees regarding the completeness, accuracy, or reliability of the information presented. Before making any financial or retirement-related decisions, consult a qualified financial advisor, tax professional, or other licensed professional who can provide advice tailored to your specific circumstances.