How Much Should You Save by Age? [Benchmarks 2026]

One of the biggest retirement questions people ask is:

“How much should I have saved by my age?”

The answer depends on your income, lifestyle, retirement goals, and when you started saving. However, retirement benchmarks provide an excellent way to measure your progress and identify whether you’re ahead, behind, or right on track.

This guide explains recommended retirement savings targets by age, why these milestones matter, and what to do if you’re behind.

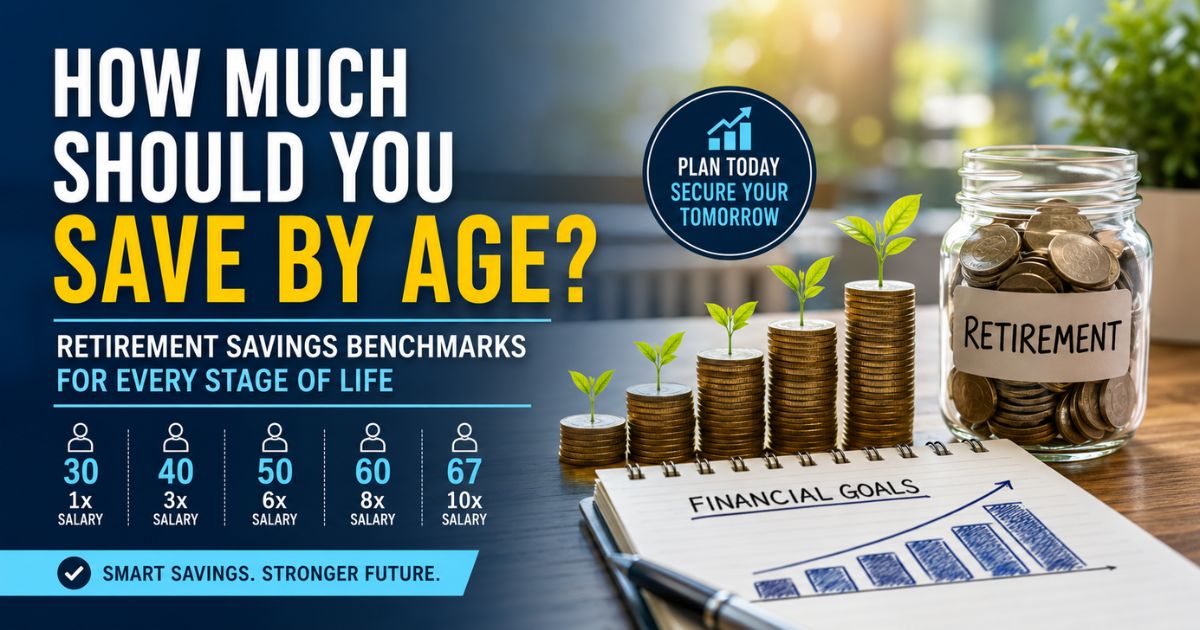

Quick Retirement Savings Benchmarks

| Age | Recommended Retirement Savings |

|---|---|

| 30 | 1× annual salary |

| 35 | 2× annual salary |

| 40 | 3× annual salary |

| 45 | 4× annual salary |

| 50 | 6× annual salary |

| 55 | 7× annual salary |

| 60 | 8× annual salary |

| 67 | 10× annual salary |

Example

If you earn $80,000 per year:

- Age 30 → $80,000

- Age 40 → $240,000

- Age 50 → $480,000

- Age 60 → $640,000

- Retirement (67) → About $800,000

These are general guidelines, not strict rules.

Retirement Savings by Age

By Age 20–29

Goal

Begin building the saving habit.

Even small contributions have decades to grow thanks to compound interest.

Recommended Actions

- Contribute to your employer’s 401(k)

- Capture the full employer match

- Open a Roth IRA if eligible

- Build an emergency fund first

Savings Target

Aim for approximately 1× your annual salary by age 30.

By Age 30

Many people experience income growth during their thirties while balancing mortgages, childcare, and other major expenses.

Recommended Target

1× your annual salary

Example:

Annual salary: $70,000

Retirement savings goal:

$70,000

By Age 35

Your career is usually becoming more established.

Increase retirement contributions whenever you receive raises.

Savings Target

2× annual salary

Example:

Salary: $90,000

Target:

$180,000

By Age 40

By now, retirement should become a major financial priority.

Many financial planners recommend saving 15%–20% of income annually if possible.

Savings Target

3× annual salary

Example:

Salary: $100,000

Target:

$300,000

By Age 45

Compound growth should now become a significant contributor to your portfolio.

Savings Target

4× annual salary

Focus on:

- Increasing investments

- Avoiding high-interest debt

- Maximizing employer retirement plans

By Age 50

You’re entering your highest earning years.

This is also when the IRS allows catch-up contributions to many retirement accounts.

Savings Target

6× annual salary

Example:

Salary: $120,000

Goal:

$720,000

By Age 55

Retirement is approaching.

Begin estimating future retirement expenses.

Savings Target

7× annual salary

Also consider:

- Healthcare costs

- Long-term care planning

- Social Security timing

- Tax-efficient withdrawals

By Age 60

Most people are within a decade of retirement.

Savings Target

8× annual salary

Review:

- Investment allocation

- Retirement income strategy

- Required expenses

- Withdrawal plans

Retirement Age (Around 67)

Many retirement experts suggest aiming for approximately:

10× your annual salary

This level of savings often supports a comfortable retirement when combined with:

- Social Security

- Pension income (if available)

- Personal investments

- Other retirement assets

Why These Benchmarks Matter

Age-based savings goals help you:

- Measure your retirement progress

- Identify savings gaps early

- Increase contributions before it’s too late

- Stay motivated with realistic milestones

- Avoid unpleasant surprises near retirement

Remember, they’re meant to be guideposts—not guarantees.

Factors That Affect How Much You Need

Your ideal retirement savings may differ depending on:

Retirement Age

Retiring at 55 requires much more savings than retiring at 67.

Lifestyle

Luxury travel costs more than a modest retirement lifestyle.

Expected Social Security Benefits

Higher benefits reduce the amount you may need from personal savings.

Healthcare Costs

Medical expenses often increase during retirement.

Investment Returns

Higher long-term returns may reduce the amount you need to contribute, while lower returns may require higher savings.

Inflation

Future living expenses are likely to be much higher than today’s costs.

What If You’re Behind?

Many people discover they’re below recommended savings targets.

The good news is that it’s never too late to improve your retirement outlook.

Consider:

- Increase retirement contributions each year

- Contribute enough to receive your employer’s full match

- Maximize IRA contributions

- Delay retirement if needed

- Reduce unnecessary expenses

- Avoid withdrawing retirement funds early

- Invest consistently instead of trying to time the market

Even modest increases can make a meaningful difference over time.

How Much Should You Save Each Month?

A common recommendation is to save:

- At least 15% of gross income for retirement.

- 20% or more if you start saving later or plan to retire early.

Example:

| Annual Income | Monthly Retirement Savings (15%) |

|---|---|

| $50,000 | $625 |

| $75,000 | $938 |

| $100,000 | $1,250 |

| $150,000 | $1,875 |

Your exact savings rate depends on your age, retirement timeline, and existing savings.

Retirement Savings Tips

Start Early

Time is one of the most valuable factors in retirement planning.

Increase Contributions Automatically

Raise your savings rate whenever you receive a raise.

Diversify Investments

A balanced portfolio helps manage long-term risk.

Review Progress Annually

Compare your current savings against age-based benchmarks every year.

Avoid High Fees

Lower investment costs can significantly improve long-term returns.

FAQs About How Much Should You Save by Age

Is it bad if I don’t have one year’s salary saved by age 30?

Not necessarily. Many people start later. The important step is to begin saving consistently and gradually increase contributions.

Should I include my home equity?

Generally, retirement savings benchmarks refer to retirement accounts and investments, not your primary home’s equity.

What if my salary changes significantly?

Update your savings targets whenever your income changes. Benchmarks should reflect your current earnings.

Are these benchmarks guaranteed?

No. They’re general planning guidelines based on common retirement assumptions. Individual needs vary based on lifestyle, health, taxes, investment performance, and retirement goals.

Final Thoughts

Age-based retirement savings benchmarks provide a practical way to measure your financial progress and adjust your strategy before retirement arrives.

Whether you’re just starting in your 20s or catching up in your 50s, consistent saving, disciplined investing, and regular reviews can significantly improve your long-term financial security.

Remember that these milestones are guidelines, not rigid rules. Focus on steady progress, increasing contributions when possible, and creating a retirement plan that fits your personal goals.

Disclaimer: The information provided in this article is for educational purposes only and should not be considered financial, investment, tax, or legal advice. Retirement savings benchmarks are general guidelines and may not reflect your individual financial situation or goals. Investment returns are not guaranteed, and all investments involve risk, including the possible loss of principal. Before making financial decisions, consider consulting a qualified financial advisor, tax professional, or retirement planning specialist.